Leaderboard

Popular Content

Showing content with the highest reputation on 12/17/2021 in Posts

-

I think this is it.....Hope it helps.

4 points

4 points -

You are in a potential "conflict of interest" situation, which might require letters signed by both of your clients.3 points

-

Just make sure that both A and B both feel like they have been given fair and objective advice which results in both clients satisfied, which needs to documented in writing and signed by both clients.2 points

-

Agreed! It shouldn't be such a mystery to find. I find those little checkboxes and blips of information ATX throws in above the forms is where they stealthily put a lot of incredibly important data entry clues.2 points

-

If shareholder A is 75% and wishes to "own" 100% of the property as sole shareholder he will have to pay a price one way or another. So his choices are basically to buy out the shares of B or pay tax on his share of the gain if proceeds from the sale are not fully invested in replacement property. Gain is recognized at that point and allocated to the shareholders since less than 100% of the proceeds were reinvested. Then the cash from the sale is used to redeem the stock of B and A becomes 100% shareholder. That would involve a corporate reorganization coordinated with the 1031 where each shareholder ends up with a separate company; which in turn hold their separate replacement properties. Does not sound like the direction your client wants to go.2 points

-

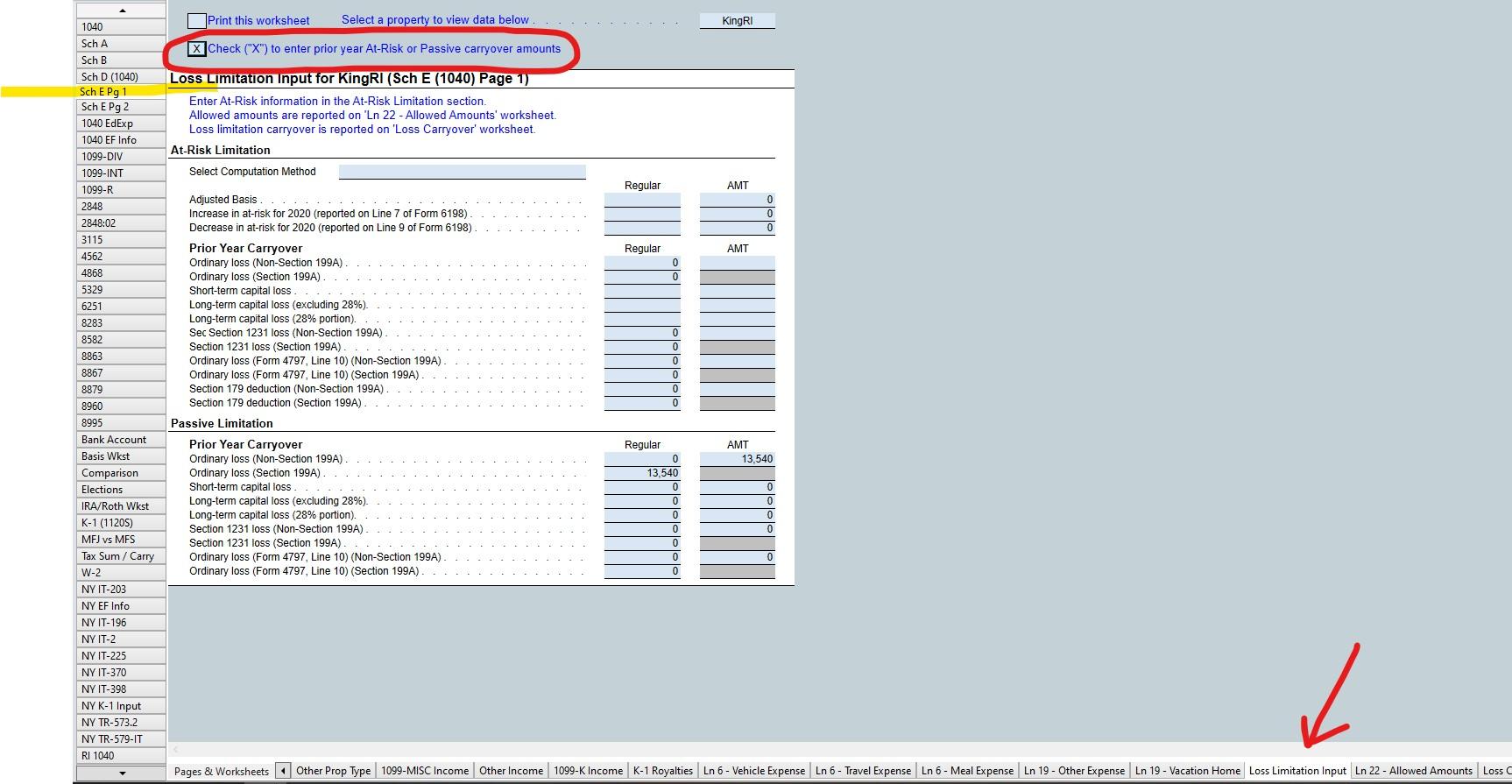

ATX must have changed this and it's been years since I've had to do one, but I cannot find where to enter this. I've been all over the Sch E and the 8582, to no avail. Thanks! Edit: I found the answer in the Knowledgebase. You have to check a box on the Sch E Loss Limitation Input tab.1 point

-

You might be surprised on how that would work out. Say for example the only asset of the corp was bare land in a prime location, basis of 100,000 and fmv of 200,000, clear title. So B's stock value of 25% = 50,000. First option is for A to buy B's stock for 50,000 out right if he has the cash, either before or after 1031 transaction with zero boot received. If he does not have the cash, the property can be sold through a partial 1031 and 50,000 of cash received, which is used to redeem B's stock. Then a gain of $50,00 is recognized. A's 75% share of the gain is 37,500. Assume the gain is taxed at 15% federal and 10% state for a total of $9,375. So now instead of spending 50,000 to become 100% owner of corp worth $200,000, he has paid $9,375 in taxes to to become 100% owner of a corp worth $150,000. A third option is to complete the 1031 in whole, then borrow 50,000 against the replacement property at the corporate level. The $50,00 is then used to redeem the 25% stock owned by B. In that scenario A has not spent any money personally to become 100% owner in a corp worth $150,000, including a note payable of $50,000. Also, "A" does not incur a tax bill under that option. Hope I am not overlooking anything here, but if you run the numbers for your client he or she will have some solid footing to make a decision.1 point

-

Thanks! Yes, that's the correct tab and you don't need to check the box if you're only entering PAL carryovers. Now, ATX needs to update the jump from the 8582 to take you to that tab and not the one where you can't enter anything. And, they should add a jump from the tab you can't enter anything on Sch E to the tab where you can.1 point

-

From what I read this morning, I was wrong. MS is doing away with the "default browser" selection and it will always be Edge going forward unless people freak out enough / the government warns them of anti-trust violations.1 point

-

Just checked a pdf with a link - opened in my default browser. Now I have an insatiable desire to do all my internet searches via my start menu.1 point

-

Subsequent articles say that EdgeDeflector has been revised to get around the Microsoft block, which MS will probably block, since Microsoft has stated that apps like EdgeDeflector are in violation of MS policies. Also Microsoft is now blocking Firefox users from accessing microsoft.com and other associated domains because Firefox has been in of violation of some Microsoft technical specifications since 2016.0 points