jklcpa

-

Posts

7,165 -

Joined

-

Days Won

406

Posts posted by jklcpa

-

-

Some suggestions:

1. Run Admin Console

2. Make sure your ATX server is running.

3. Make sure your AV isn't blocking some file or process with those years. You may want to check for any files to excluded from the AV. Maybe start with whatever files or processes you have excluded in your AV, if any, and see if similar is excluded for 2020 and 2021.

-

3

3

-

-

Hmm, with Drake I can name a pdf attachment anything I like and enter that name in a space provided within the input. As long as the input matches the file I've attached it goes though.

-

3

-

-

Tom this page should help. Also, did you write down or copy the recovery code at the bottom of the page during setup of the authenticator when you first paired your phone? CCH help says that is used to fix things when your phone is lost or stolen. You may have to go through the steps of unpairing, re-pairing.

-

3

-

-

Maybe the emails are being sent in batches. Here it is for anyone that hasn't seen it yet.

-

3

-

1

1

-

-

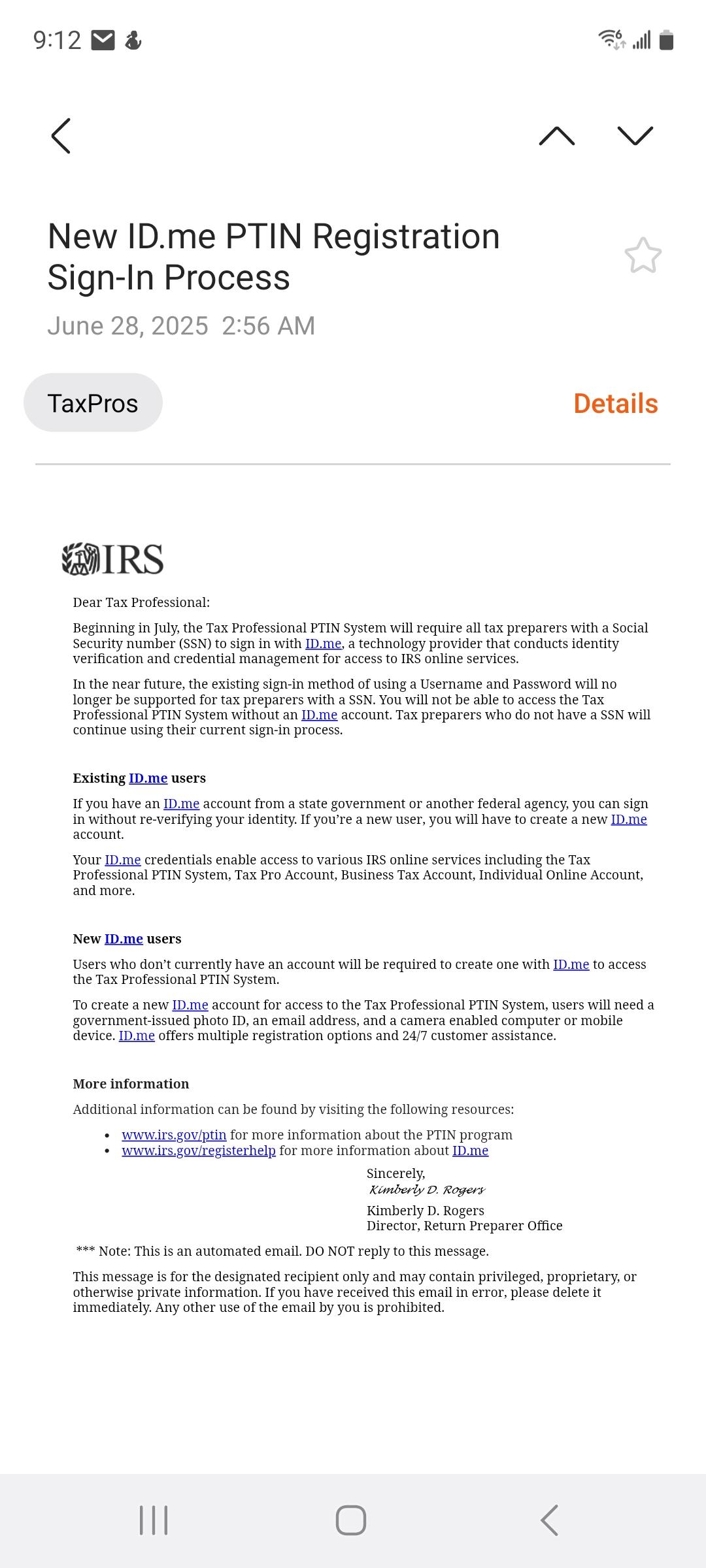

Posting in case anyone here hasn't read the email saying that ID.me will be required to log in to the PTIN and other IRS services.

-

4

-

-

https://www.thetaxadviser.com/newsletters/2020/mar/married-taxpayers-jointly-owned-business/

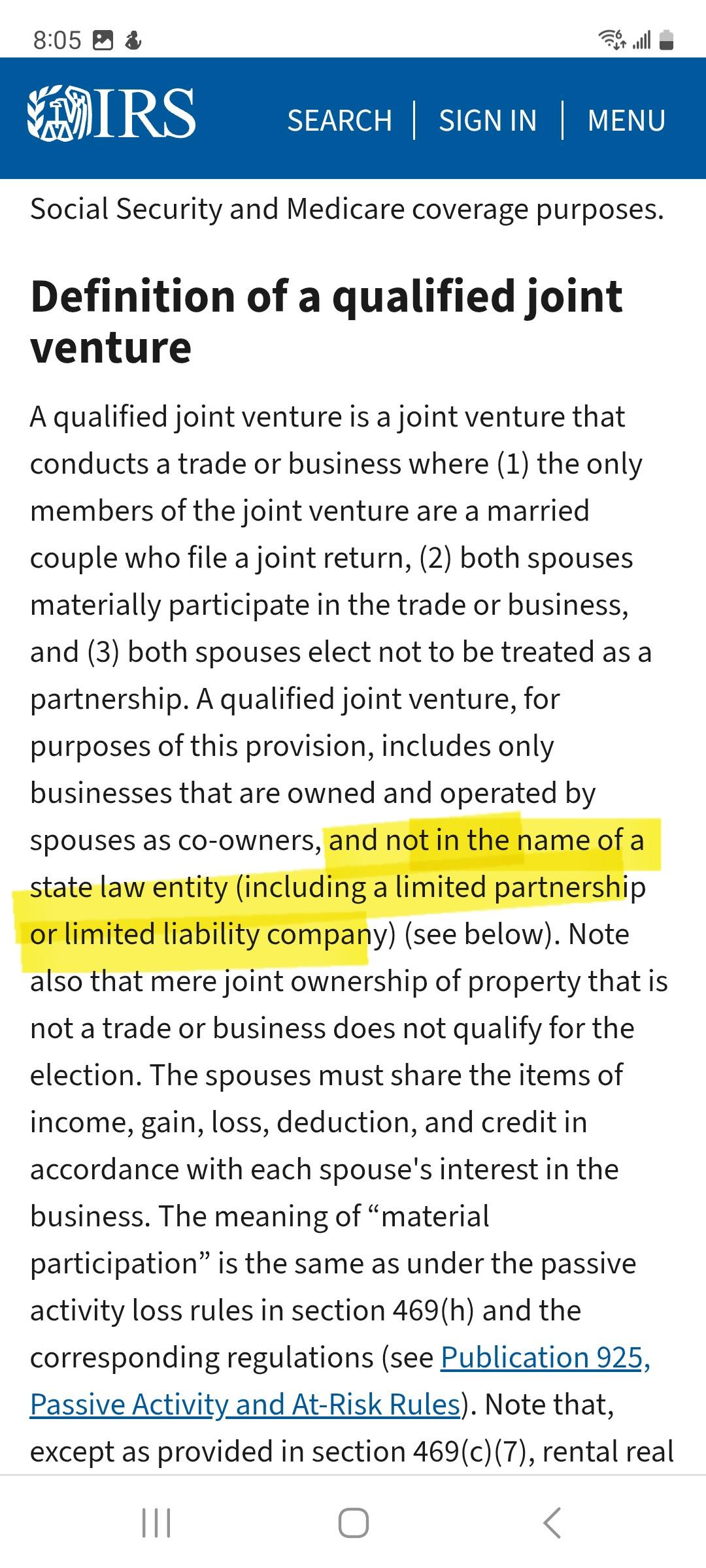

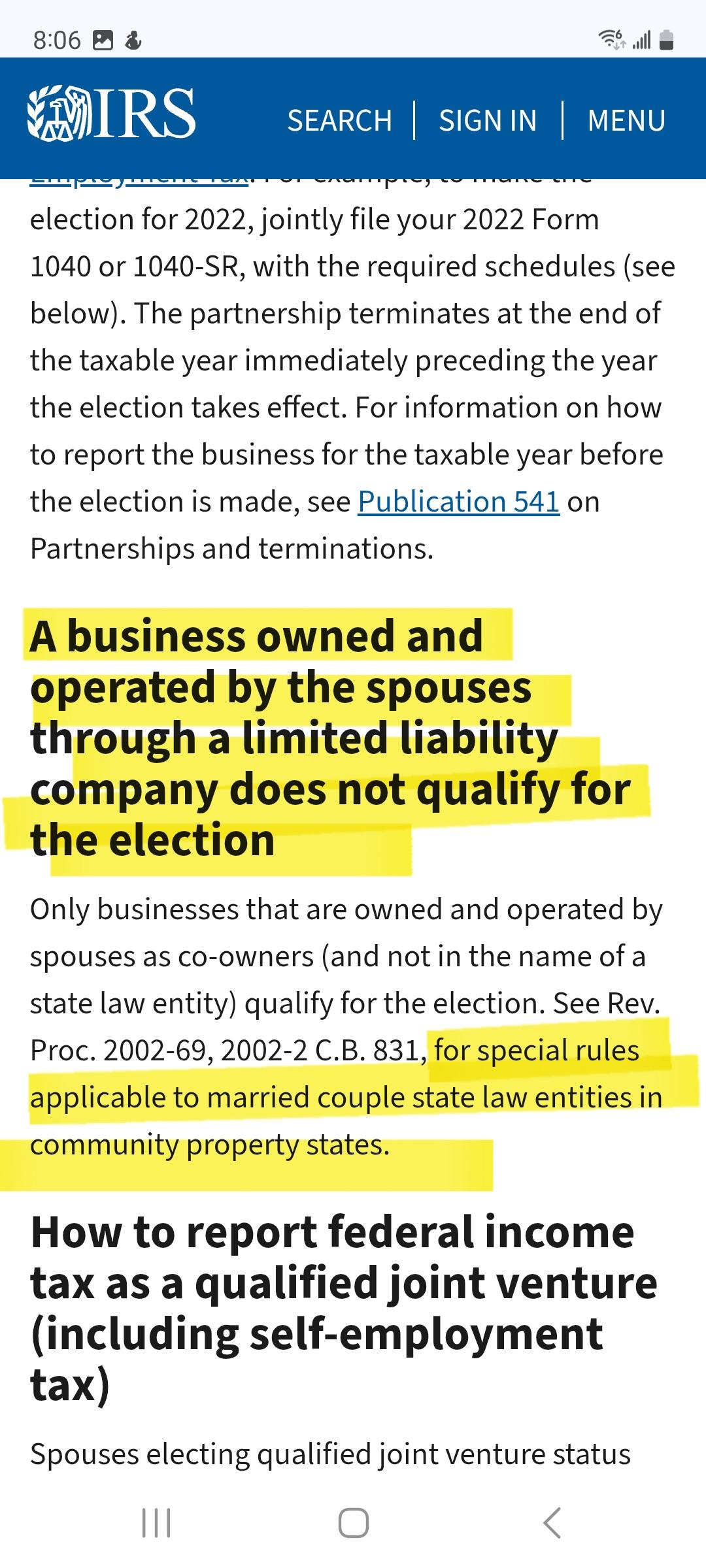

QuoteUnfortunately, limited liability companies (LLCs) do not qualify for the Sec. 761(f) election. Businesses operated in the name of a state law entity, e.g., LLCs, limited liability partnerships (LLPs), and limited partnerships (LPs), are ineligible for the Sec. 761(f) election, regardless of their existing tax status as a partnership or otherwise qualifying as a qualified joint venture. These entities must follow the tax filing status they previously elected upon formation or elect a new status they qualify for. As a multi-owner entity, this will mean filing as a partnership if corporate tax status, S or C, is not elected. These rules are summarized under Regs. Secs. 301.7701-2 and 301.7701-3.

@DANRVANThis is a second article from The Tax Advisor that disagrees with your interpretation by saying that MMLLCs are state entities that do not qualify to make the 761(f) election, and that goes on to make the separate point of an exception to those in community property states. I would still tell the OP to file a 1065.

9 hours ago, DANRVAN said:In Argosy .... The taxpayers lost.

- The determining factors in that case were the previous filing of 1065 by the plaintiffs and the failure to make an election under 761(f) as a QJV.

- The facts that the plaintiffs resided in a non-community property state; and were an LLC were not mentioned in the opinion of the court.

- Therefore it appears to me the court looked to the code for authority and was not bound by the RP stipulations.

In Argosy, the court didn't need to consider that it was an LLC or not because there were previous filings as a partnership.

-----------------

As to your H-W rentals in your state and the audit you mentioned, not all auditors are that good. Are these in LLCs? Even if not, did you make a 761(f) election for them? Do you check for material participation of EACH party each year without attribution of the participation of each to the other? Also from the same Tax Advisor article:

QuoteRental real estate activities owned by spouses can also meet the definition of a qualified joint venture. When these activities qualify for the election under Sec. 761(f), the IRS allows joint filers to file as a single Schedule E activity. With no self-employment income or tax to be assigned to either taxpayer, there is no reason to separate ownership. Unfortunately, rental real estate activities rarely meet the criteria of a qualified joint venture because of the material participation requirement.

-

1

-

1

-

35 minutes ago, Christian said:

Herein lies my confusion.

However, when you die, any capital loss carryover is lost. It cannot be utilized by your estate or surviving spouse except in the final tax return filed for the year that you die. Therefore, it’s important to use as much of the remaining deduction as possible in the final year (or in the years prior to death). There are planning techniques available to help accomplish this goal.

That's correct. What this means is that the final 1040 can show up to a $3,000 loss (just like usual) and any remaining loss carryover is lost.

The planning opportunity mentioned is where a surviving spouse can sell capital assets having a gain in that year of death so that the otherwise unused losses would offset those gains. Example: your client is allowed $3K of losses allowed in the current year and $25K losses unused that are going to be lost. The taxpayer (prior to death) or surviving spouse any time during that year, if filing MFJ, could have sold other capital assets having GAINS up to that $25K with no additional tax effect. If single, that client could have done that in prior years or in the final year prior to death to use up the losses so that they aren't lost. For a single taxpayer where someone has a POA and is aware of the situation, that person could so initiate such a sale of capital asset prior to the taxpayer's death.

-

5

-

-

@DANRVAN Dan, IRS information page on QJVs says it can't be held in a state-recognized entity such as an LLC. Are these IRS pages incorrect? This rental the OP asked about is in an LLC owned by the rev trust. According to the original post, this is in a NONcommunity property state. Do you still think it goes on Sch E and not on 1065?

-

1

-

-

No, the losses in year of death are handled like any other year. Any capital losses that are unused (those that would carryfwd if the person lived) are lost. They die with the decedent.

-

9

-

-

1 hour ago, G2R said:

I learn something new everyday. Thanks!

I worded that very poorly. I revocable trust can have biz prop that is QJV, but it can't be in an LLC, rather it must be operated in an unincorporated entity. So in your case, QJV would be off the table on 2 scores: because the rental is in an LLC and because the client is in a non-community property state.

Sorry for the confusion.

-

1

-

1

-

-

Revocable trust is a grantor trust and is generally ignored for tax return reporting unless it has an EIN and requires a separate 1041 for income to pass through. As you said, QJV is off the table because you are dealing with a non-community property state. Trusts are precluded from holding business property that elects to be QJV anyway.

With all of that in mind and being a revocable trust, then the LLC reporting falls to state law. If this had been a SMLLC, then it would certainly be reported on 1040 Sch E.

Because it is a MMLLC, then you would look to state law which probably says that the multi-member LLC (even H-W) would default to a partnership unless the LLC had the ability and elected to be taxed as a corporation. In your client's case, it sounds like this should be on a 1065 using form 8825 with the husband and wife each receiving a K-1 from the partnership.

-

1

-

1

-

-

19 minutes ago, Lee B said:

Frankly, there are so many so-called emergency announcements it's hard to know what's an emergency or what's clickbait

Ok, well this one came to me in an email that I get directly from Malwarebytes.

Whatever version, users should check to make sure the software is UTD.

-

3

-

-

Google released an emergency update for Chrome to fix a severe vulnerability. If you don't have Chrome set to update automatically, or if you close it infrequently, you should check to make sure you are up to date with the latest version.

"The update brings the Stable channel to versions 136.0.7103.113/.114 for Windows and Mac and 136.0.7103.113 for Linux."

-

3

-

1

-

-

-

1 hour ago, Pacun said:

2.- If I suggest my clients to contribute to an IRA, am I giving financial advice?

I agree with Abby Normal on the crypto investing.

As for your second question, if you are simply suggesting that the client considers an IRA and are explaining the effects it would have on their tax return, then you are not giving investment advice.

-

4

-

-

I use e-services so infrequently that there is always some new requirement to get in. I hadn't bothered with it until yesterday and went through the ID.me process. I had opted for the login.gov to access EFTPS instead.

Just watch, now it will probably change again in the near future!

-

3

-

2

2

-

-

1 hour ago, BTS said:

Am I missing the "No tax on Soc Sec" ? I see it no where in the bill.

You didn't miss it, but the proposed legislation going to the Senate is supposed to have an additional $4,000 of standard deduction for seniors.

Those over 65 were already getting a higher standard deduction, so I suspect that this won't be a full $4,000 increase from what a senior was getting already. -

24 minutes ago, Randall said:

I thought I saw a headline this morning that the bill has passed the whole House. But doesn't it still have to go through the Senate? I usually wait for it to become law. Then we'll get some info and summaries and the IRS can start working on the forms and processing of it all.

Yes, it did. Now it goes to the Senate.

-

1

-

-

I, too, have only the login.gov.

-

2

-

-

Did you see this page under "Maintainingyour EFIN"? Like I said, it's been years, but when I changed my address and then when I added additional services, I'm pretty sure that I opened my application and made the changes and had to resubmit it. I don't remember it saying that it was a new application, but it did seem like I was reapplying because of having to "submit" the application. https://www.irs.gov/tax-professionals/how-to-maintain-monitor-and-protect-your-efin

-

1

-

-

2 hours ago, Margaret CPA in OH said:

The thought of new letterhead, cards, whatever is frightening. I wonder if my clients would mind old letterhead on the engagement letter. How much can I do without? This would also be the death knell of my fax line. Many changes ahead for us, Taxit!

I decided not to purchase stationery when I moved and got only new business cards. I do have shipping labels printed with my name & address that I can also use on tax folders, colors do match the folders so it looks nice. I don't use these regularly on folders for all returns, only oddball returns that I haven't printed out labels for at the beginning of the season.

For letterhead, I created that as a template in MS-Word. I usually print on plain paper, but if you want it to be nicer without engraved stationery, you could buy heavier weight bond if you think the recipient notices or cares. No preprinted envelopes either. They are either run through my printer, again a template, or I use clear Avery address labels using the same font as the letterhead. I use these on a variety of envelopes including small return envelopes that go with invoices or balance due reminders.

I guess it depends on how much your image depends on these, and how much your clients would notice or care. Mine don't care, and the template works better for anyone that gets the correspondence by pdf attachment rather than snail mail.

Sorry for the derail from the Efin addy change, and if this portion gets lots of responses,I may move to its own topic.

-

3

-

-

1 hour ago, taxit said:

I am in the process of downsizing/retiring. I put my office on the market and moved everything to my home. I need to update the change of address and phone number for My EFIN. It says to long into e-services. When I do that I do not see anywhere to update these items. Has anyone completed this task and can offer a tip?

When I changed mine, it was in the application area. Sorry to say it's been enough years ago that I don’t remember the specifics, but it was as if resubmitted the appication, or that part of the appication.

-

1

-

-

11 hours ago, kathyc2 said:

Whatever... Just go ahead and delete it then.

Sorry, I didn't mean the forum shouldn't discuss it. I meant that "I" personally don't because it will change.

I heard that the main objections were to the amount it would increase the deficit and debt, the SALT limitation, and by implication, probably the overall limitation on itemized deductions.

Like I said, it didn't make it to the House floor, and Republican senators were already voicing strong objections, so that we know that the Senate would not pass it it's current form there either.

-

3

-

-

This didn't even make it out of committee in the House and why I've always had a policy of not discussing any legislation until it passes.

-

5

-

I can't get 2020 or 2021 to work

in General Chat

Posted

To be clear, the "ATX server" is a piece of software installed on your machines that needs to be running for the program to start. It has nothing to do with the term "server" used where hardware is designated as the server in networked installation (vs standalone). This is also different than the server at the processing center that the ATX program connects to via the internet.