jklcpa

-

Posts

7,165 -

Joined

-

Days Won

406

2 Followers

Recent Profile Visitors

49,660 profile views

-

To be clear, the "ATX server" is a piece of software installed on your machines that needs to be running for the program to start. It has nothing to do with the term "server" used where hardware is designated as the server in networked installation (vs standalone). This is also different than the server at the processing center that the ATX program connects to via the internet.

-

Some suggestions: 1. Run Admin Console 2. Make sure your ATX server is running. 3. Make sure your AV isn't blocking some file or process with those years. You may want to check for any files to excluded from the AV. Maybe start with whatever files or processes you have excluded in your AV, if any, and see if similar is excluded for 2020 and 2021.

-

Descendent Return with Court Appointed Personal Rep Attachement

jklcpa replied to b#tax's topic in General Chat

Hmm, with Drake I can name a pdf attachment anything I like and enter that name in a space provided within the input. As long as the input matches the file I've attached it goes though. -

Tom this page should help. Also, did you write down or copy the recovery code at the bottom of the page during setup of the authenticator when you first paired your phone? CCH help says that is used to fix things when your phone is lost or stolen. You may have to go through the steps of unpairing, re-pairing. https://files.cchsfs.com/doc/atx/2024/Help/Content/Both-SSource/Login and Passwords/Manage Admin Authentication.htm

-

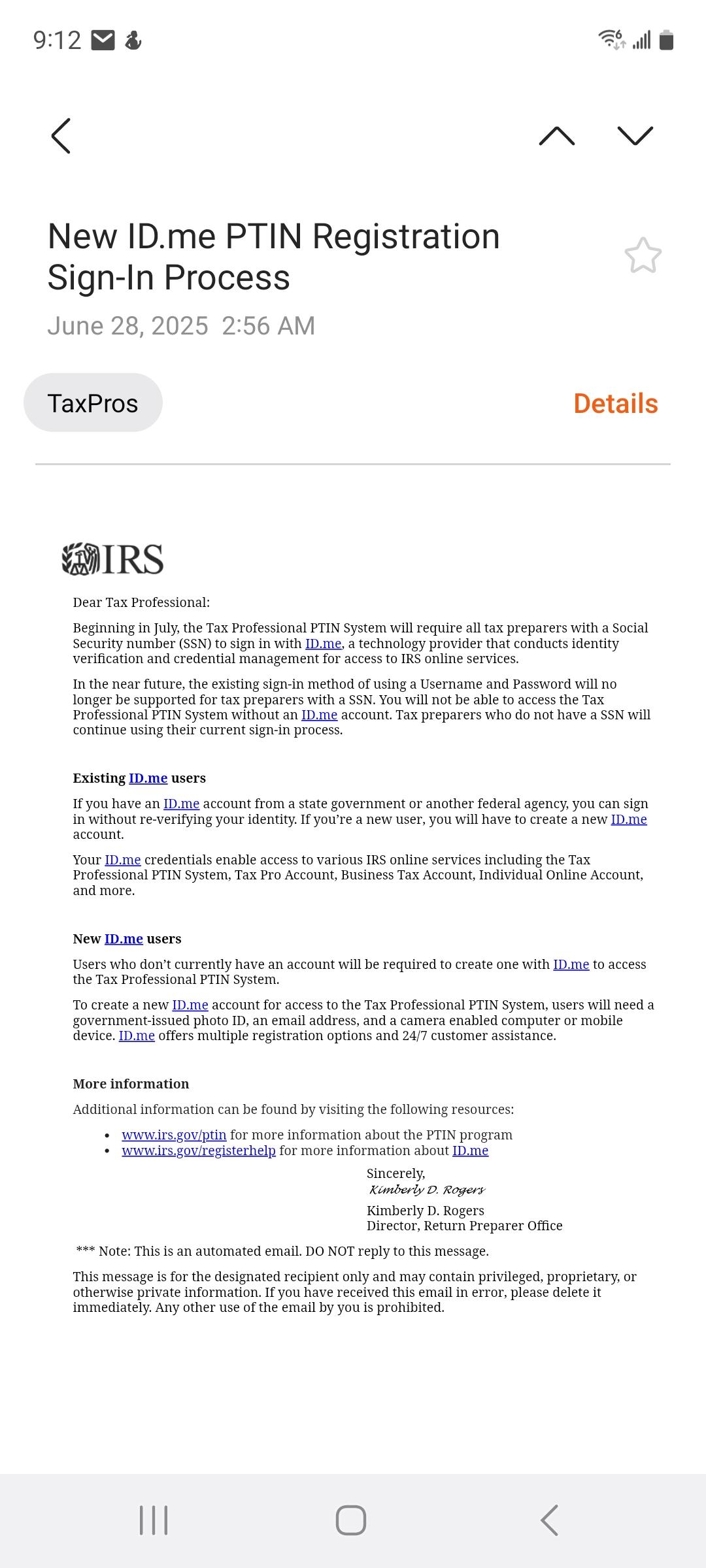

Maybe the emails are being sent in batches. Here it is for anyone that hasn't seen it yet.

-

Posting in case anyone here hasn't read the email saying that ID.me will be required to log in to the PTIN and other IRS services.

-

Married Couple Revocable Trust Owns LLC in Non-Community Property State

jklcpa replied to G2R's topic in General Chat

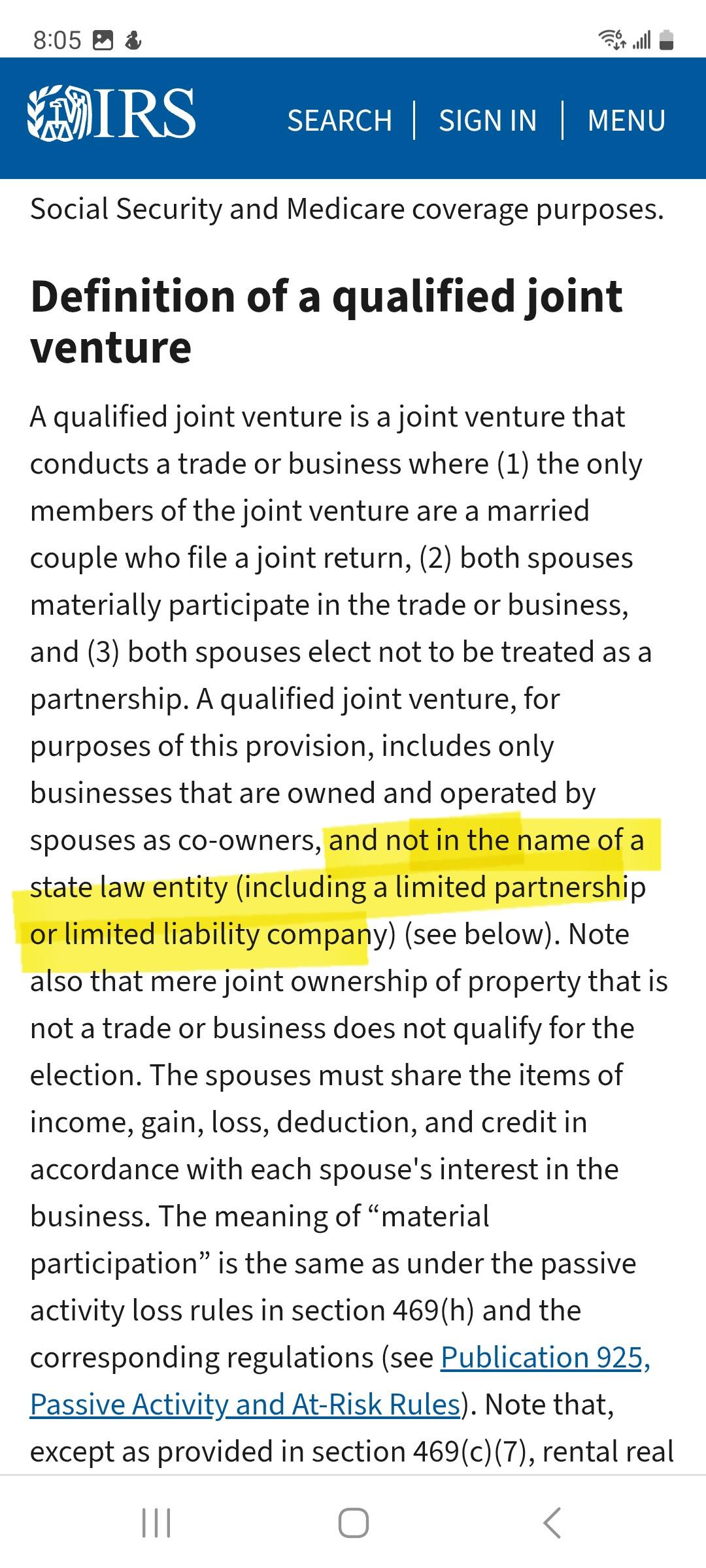

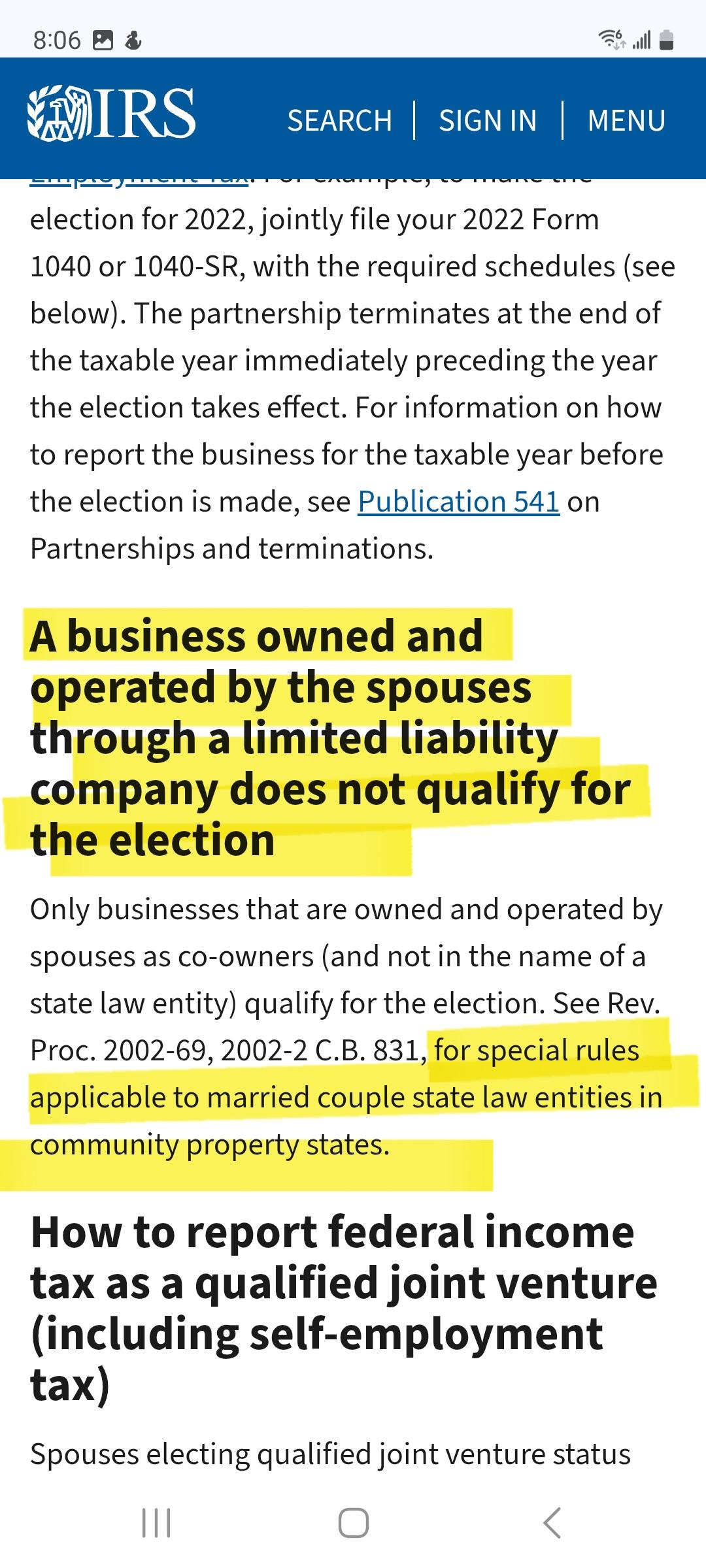

https://www.thetaxadviser.com/newsletters/2020/mar/married-taxpayers-jointly-owned-business/ @DANRVANThis is a second article from The Tax Advisor that disagrees with your interpretation by saying that MMLLCs are state entities that do not qualify to make the 761(f) election, and that goes on to make the separate point of an exception to those in community property states. I would still tell the OP to file a 1065. In Argosy, the court didn't need to consider that it was an LLC or not because there were previous filings as a partnership. ----------------- As to your H-W rentals in your state and the audit you mentioned, not all auditors are that good. Are these in LLCs? Even if not, did you make a 761(f) election for them? Do you check for material participation of EACH party each year without attribution of the participation of each to the other? Also from the same Tax Advisor article: -

That's correct. What this means is that the final 1040 can show up to a $3,000 loss (just like usual) and any remaining loss carryover is lost. The planning opportunity mentioned is where a surviving spouse can sell capital assets having a gain in that year of death so that the otherwise unused losses would offset those gains. Example: your client is allowed $3K of losses allowed in the current year and $25K losses unused that are going to be lost. The taxpayer (prior to death) or surviving spouse any time during that year, if filing MFJ, could have sold other capital assets having GAINS up to that $25K with no additional tax effect. If single, that client could have done that in prior years or in the final year prior to death to use up the losses so that they aren't lost. For a single taxpayer where someone has a POA and is aware of the situation, that person could so initiate such a sale of capital asset prior to the taxpayer's death.

-

Married Couple Revocable Trust Owns LLC in Non-Community Property State

jklcpa replied to G2R's topic in General Chat

@DANRVAN Dan, IRS information page on QJVs says it can't be held in a state-recognized entity such as an LLC. Are these IRS pages incorrect? This rental the OP asked about is in an LLC owned by the rev trust. According to the original post, this is in a NONcommunity property state. Do you still think it goes on Sch E and not on 1065?

-

No, the losses in year of death are handled like any other year. Any capital losses that are unused (those that would carryfwd if the person lived) are lost. They die with the decedent.

-

Married Couple Revocable Trust Owns LLC in Non-Community Property State

jklcpa replied to G2R's topic in General Chat

I worded that very poorly. I revocable trust can have biz prop that is QJV, but it can't be in an LLC, rather it must be operated in an unincorporated entity. So in your case, QJV would be off the table on 2 scores: because the rental is in an LLC and because the client is in a non-community property state. Sorry for the confusion. -

Married Couple Revocable Trust Owns LLC in Non-Community Property State

jklcpa replied to G2R's topic in General Chat

Revocable trust is a grantor trust and is generally ignored for tax return reporting unless it has an EIN and requires a separate 1041 for income to pass through. As you said, QJV is off the table because you are dealing with a non-community property state. Trusts are precluded from holding business property that elects to be QJV anyway. With all of that in mind and being a revocable trust, then the LLC reporting falls to state law. If this had been a SMLLC, then it would certainly be reported on 1040 Sch E. Because it is a MMLLC, then you would look to state law which probably says that the multi-member LLC (even H-W) would default to a partnership unless the LLC had the ability and elected to be taxed as a corporation. In your client's case, it sounds like this should be on a 1065 using form 8825 with the husband and wife each receiving a K-1 from the partnership. -

Ok, well this one came to me in an email that I get directly from Malwarebytes. Whatever version, users should check to make sure the software is UTD.

-

Google released an emergency update for Chrome to fix a severe vulnerability. If you don't have Chrome set to update automatically, or if you close it infrequently, you should check to make sure you are up to date with the latest version. "The update brings the Stable channel to versions 136.0.7103.113/.114 for Windows and Mac and 136.0.7103.113 for Linux." https://www.malwarebytes.com/blog/news/2025/05/update-your-chrome-to-fix-serious-actively-exploited-vulnerability?utm_source=iterable&utm_medium=email&utm_campaign=b2c_pro_oth_20250526_mayweeklynewsletter_paid_v4_1_174792831761&utm_content=Update_your_Chrome

-

Wow!