Catherine

-

Posts

7,473 -

Joined

-

Last visited

-

Days Won

463

3 Followers

Recent Profile Visitors

20,721 profile views

-

I like to say, "I have easier ways to hurt myself!" and Eric has (or had?) a GIF for us on that exact topic.

-

I have one couple who share an email, and I send to them twice - once for him, and once for her. I suppose in theory one could sign in both spots, but for that you'd have to know the clients, I guess. I had emails in the workspace sent by each of them (signed by name; different 'voices'), and so knew both were on board and spoke with each other about the returns regularly. If it was a couple where I had contact, mostly, with only one of them, I might be chary of using a single email address.

-

I did get a renewal notice from Drake, with different options. I'll be looking at them soon. Still recovering from bronchitis.

-

As long as they are in a Workspace thread with both people, you set up the two signers. It goes to #1, automatically to #2, then back to you once signed.

-

Old college professor of mine said "You only start to understand thermodynamics about the third or fourth time you teach it."

-

I ended up sending a letter for my case. we're now past the "response date" of the letter and I started mine out stating that I've been trying to get through from about a week before the response date. If the IRS never answers the phone, they cannot then say the t/p is SOL because they did not respond in time.

-

Part Year Resident of 2 States - Sale of Real Estate

Catherine replied to gfizer's topic in General Chat

Might not matter where they still had their residence at the time. States vary, but over time more are taxing full-year income regardless of where earned. Then they adjust based on % earned in what state, or $ earned in each state, or they apportion by date. Home state will give credit for tax paid to another jurisdiction, usually up to the amount they tax on that same income. You'll need to research what KY and WI want for part-year resident reporting. -

An office support place like Staples or Kinkos, or a local stationer, can make those for you in whatever format you want. Talk to a local shop to see what format they want you to provide, and about options. Hubby needed some specific type of scorebooks that were commercially available 30+ years ago but not for a long time. He took an old one to a local place, asked "can you make me more of these?" and they could not only make them, they gave him the choice of glue-bound or spiral-bound, paper color, page count per book, quantity, etc - all for what he considered to be a VERY reasonable price.

-

Thank you, @Eric, for everything you do for us. Do you need any donations at this time to fund the new server? If so, please let us know!

-

Wow! I've tried to call several times for a trust issue; letter response call number X and use ID number Y. No one has picked up, in an hour and a half, any time I've tried. Yesterday I got disconnected after 47 minutes; my shortest call yet. Very, very frustrating.

-

Fed refund shorted;CO returned spouses 2023 estimated tax payments

Catherine replied to artp's topic in General Chat

Not always! I've had a few over the years where no letter ever followed to explain discrepancies. The states tend to be worse about that than the IRS, but the IRS does it too. I'd call. Next week. -

The forms may also insidiously end up being issued years afterwards, when the taxpayer is no longer insolvent. Then it can become taxable income.

-

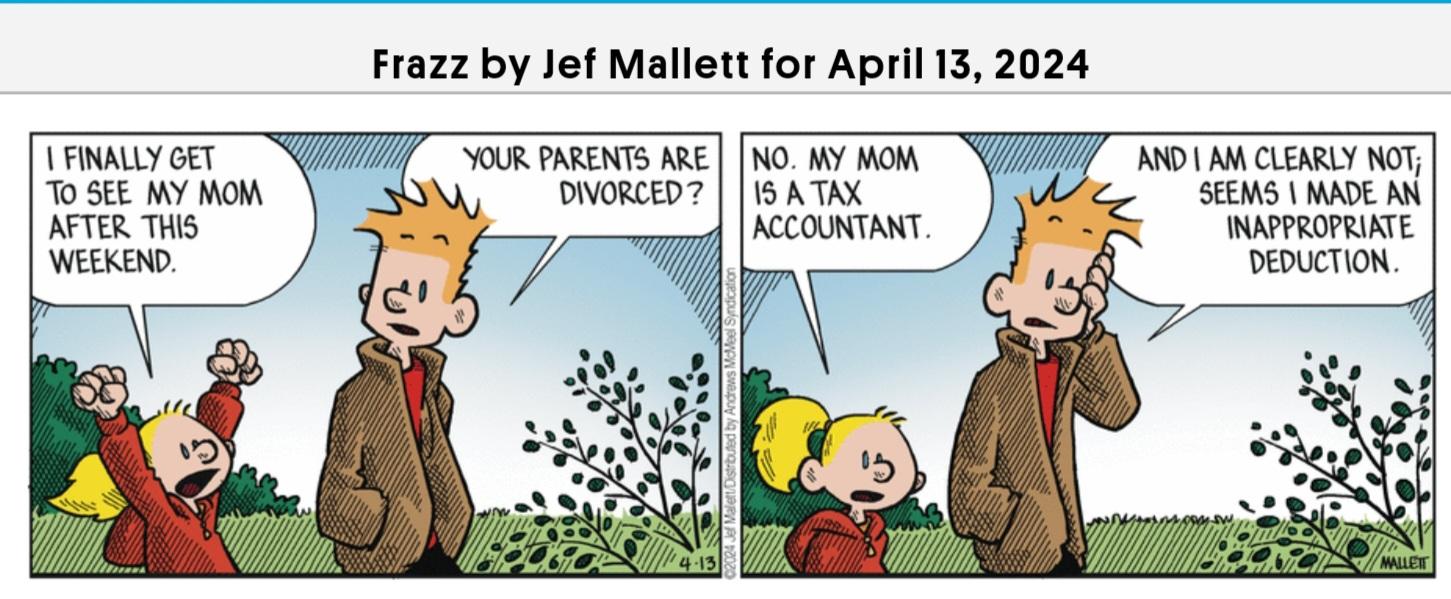

Here you go, Gail. https://www.gocomics.com/frazz/2024/04/13

-

Maybe institute a per-call fee, so you try hard yourself before calling. Even a small fee of $1 to $5 per call would make a lot of folks look things up themselves first.