jklcpa

-

Posts

6,640 -

Joined

-

Days Won

328

Posts posted by jklcpa

-

-

12 minutes ago, Lion EA said:

Well, it has to be IRS-approved CE. EAs must look for the square IRS logo that IRS-approved CE providers use and the IRS-provided course number. Only federal tax law qualifies, including ethics and updates. No state tax topics and no tax-adjacent topics, such as SS, Medicare, office management, technology, (although, IRS has now approved security-related topics).

Lion, I do know that about the credits and logo. It's great to maximize credits for the money expended, but maybe some other readers here may want or need to expand knowledge in areas that may or may not involve earning the credits in order to better serve clients or for their own benefit.

Schirallicpa had asked for courses, and as a CPA she would be able to earn credits with either Surgent or Checkpoint. Both companies have courses on the subject.

-

1 minute ago, kathyc2 said:

So CE is what it's called for enrolled agents? If something qualifies for CPE is doesn't automatically count for EA's?

Surgent's detailed course descriptions include a breakdown of the potential credits for CPAs and EAs who will recognize those (NASBA, IRS...)

Fwiw, I've taken the SS course by Bob Lickwar and found it helpful and informative but certainly not enough for me to want to create various complex scenarios for my clients.

-

1

1

-

-

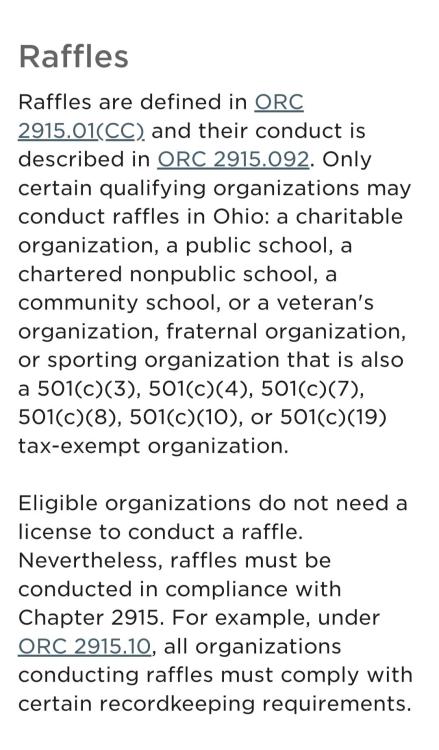

Is this more of a substance over form though? Individual owning the vacation points receives nothing in the transaction. Church has no guarantee of payment but indirectly benefits by the possibility of increase in pledges.

It seems to me that this transaction merely sidesteps the individual's donation to the church of the item being raffled.

ETA - OH gaming is regulated by state's AG. Here's the portion about raffles.

-

1

-

-

4 hours ago, Sara EA said:

Anyone remember how the IRS functioned during the last shutdown? We have several audit submissions awaiting IRS reply. Will these deadlines be extended? The return extension deadline is approaching. Will Oct 15 returns be processed?

Final question: Is it time to donate to this site again?

The e-file system still operates, so file as much electronically as possible. Postmarks for returns mailed should be honored as usual although possibly no one will be at IRS to process paper returns. Statutory deadlines still must be met, so plan for your clients to make all payments by normal due dates.

IRS hasn't finalized the contingency plan yet, but I'd assume that there will be no one to issue refunds unless automated, and definitely assume no one will be there in customer service areas to answer the phones or answer questions. In prior shutdowns, somewhere around 88% of IRS employees were furloughed, and there was a catch up period when it reopened. In one year, the start of tax season was delayed because of the extended shutdown that occurred.

If you have audits with deadlines after the possible shutdown date, contact the auditor to be sure that the deadline for materials submission will be extended or meetings rescheduled.

Although this page was updated this year, this IRS page has details related to the shutdown and reopening from the 2019 shutdown:

https://www.irs.gov/newsroom/irs-activities-following-the-shutdown

Donations to this site are appreciated any time of the year.

-

5

-

-

I'd call support. The only requirement should be met is by IRS, that the original was efiled. The program used to create the amendment shouldn't matter. I've done amended returns in my program for new clients, not ATX though.

-

3

-

-

cbslee is correct. 1099-misc, box 3, issued to the estate or beneficiary.

-

1

-

-

I use it infrequently and mine said it was UTD with v 16.0.5845.188 this morning, and when I clicked "help" and "about" it started the updater and is now at v 117.0.5938.89.

I wonder if this is one of those times when multiple updates will be issued as additional weaknesses are identified, or if the corrections caused problems for enough users to be immediately addressed.

-

-

A quick google search took me to GA Dept of Revenue's page here: https://dor.georgia.gov/2020-hb-1302-tax-refund-faqs where the information you seek is covered in the FAQ. The state was supposed to issue it as a refund if applicable. No line exists on the return.

QuoteHouse Bill 1302 was signed into law by Governor Kemp on March 23, 2022, so some taxpayers may have already filed their 2021 returns. The Department of Revenue will attempt to include the H.B. 1302 refund along with other refund amounts due. For taxpayers whose 2021 returns have already been processed, the Department of Revenue will issue a separate refund beginning in May 2022.

Note: The Department anticipates issuing substantially all the refunds by early August for returns filed by April 18, 2022. Due to the volume of refunds, it may take some time for all refunds to be processed, and your H.B. 1302 refund will not be issued until your 2021 tax return has been processed, which may delay your H.B. 1302 refund. If your address has changed since you filed your 2021 return, you may update your address through the Georgia Tax Center (https://gtc.dor.ga.gov/) or by calling the Department at 1-877-423-6711.

How will I receive my H.B. 1302 refund?

Generally, you will receive the refund in the form of a paper check mailed to the address you used on your 2021 return. If, however, you paid your 2021 tax liability by ACH credit, or you provided your banking information for a 2021 refund, you will receive your H.B. 1302 refund as a direct deposit. All H.B. 1302 refunds will be sent directly to the taxpayers and not to tax preparers.

-

1

1

-

-

On 9/5/2023 at 5:25 PM, ILLMAS said:

X writes a letter to IL, submits copies of the a rental lease, utility bills etc.. showing proof of residency

Residency and domicile are two different things. Your client is domiciled in the other state, but IL still considers him a resident. There are many factors that can be used to determine residency, and only one is where the TP lives or spends time. Basically, where has the TP planted his flag so to speak: driver's license, car registration and inspection, voter registration, church, doctors, banking, where the rest of his immediate family lives, where the kids attend school, mailing address, still maintains a home in that state, social club memberships, etc.

-

4

-

1

-

-

Dec 6 is the date. New Castle County, no location mentioned yet. Sign up link and brochure is not available yet.

https://revenue.delaware.gov/calendar/

I found this by internet search for the name of the annual seminar: "Delaware Tax Institute"

At the very bottom of the page is a link to update an existing email and a phone number to be added to the list to receive information by email.

-

Years ago I set up all phone numbers under my name, husband's, and mom's with nomorobo and wasn't sure it did anything to stop the calls.

-

1

-

-

I usually don't answer if it's not someone I know, but when I do, I never say "hello" or answer "yes" to anything. I'll answer with "accounting office, Judy speaking" because answering "hello" will tell the computer dialer to route the call to an available person or trigger the computer to start responding. Even if answering "hello" sometimes there are no agents available on the other end to speak to us and so in those cases the computer will automatically disconnect from us. Also, I never say "yes" to any questions because that can be recorded and manipulated as acceptance of something we didn't intend or in answer to a question we were never asked.

I have noticed a decrease in calls that, for my office, typically are related to credit card processing, health insurance, Medicare Advantage or Medigap, and sometimes life insurance.

I don't get them on my cell phone that is personal. I have AT&T's security with it set up to route any callers not on my contact list directly to VM without it even ringing. The call log lists those as flagged from potential scammer or telemarketers. If it's a real call, that person does have the ability to leave me a message. It works well.

On my old phone I used to get calls in Chinese that were out of NY and turned out to be a scare scam directed at Chinese immigrants to get them to pay a fee so that they were not in danger of deportment. The scammers knew that only Chinese speaking people would understand and possibly fall for it with the rest of us simply ignoring it by hanging up. Those calls have finally stopped for me.

-

5

-

-

20 hours ago, JackieCPA said:

Now that he is selling it without it being rented at all, does he still qualify to take the passive loss that was carried with the sale or is that void since he decided not to rent it at all?

He will definitely have basis of:

- original cost,

- settlement charges at purchase or paid outside of closing that are required to be capitalized, and

- any subsequent improvements

Then ...

The way the original post was worded, it seems that this property was never "put in service" as a rental, but it must have been entered on Sch E if PALs were reported. I agree with cbslee that we need to know if it was available and advertised for rent.

If never put in service, he should have made an election to capitalize "otherwise deductible" expenses of the real estate taxes, mortgage interest, and other carrying charges that could have added to basis instead of incorrectly creating a PAL. For projects under development or unproductive real estate such as this one, the election must be made annually by attaching the election statement to the tax return by its due date including extensions.

In other words, IF it was never put in service as a rental and IF no 266 election was made for those years, I don't believe that there should be valid PALs available to help offset the gain, and I don't believe he would now be able to now add those expenses to basis for which no 266 elections were made.

-

5

-

I'm reviving this to say that I'm relieved not to have this responsibility or risk except for my own corporation. I'll still have to deal with the government portal, but only for myself and that's it.

I spoke with an attorney from the firm that handles my remaining corps and LLCs that will be handling this reporting. He said it's all up in the air and sure to be a nightmare when people question the need, fail to respond, or notify them with changes. They're not sure what the charge will be but sure it will not be inexpensive.

-

5

-

-

I read the original post as the home that taxpayer owned and later rented was owned solely by the taxpayer. She has children and may or may not have had a step-up in the past from a deceased spouse, or she could never have married, or married and divorced. I think that is the property now being sold that the kids were living in until 2020 that was then turned into the rental.

The original post makes no mention of that or a previous spouse related to the home/rental being sold. Taxpayer moved out of property being sold in 2014 and then married the now-deceased husband and moved into his home. To me, it sounds like she may still be living in the home of the now-deceased husband.

On 8/21/2023 at 6:34 PM, Tracy Lee said:TP sold a home that was a primary home from 2003 to 2014, then married and moved in with (now deceased) husband into his home

-

3

-

-

I wouldn't do anything yet without more information because I've followed some creative predecessors and clients that give incorrect answers.

A typical audit scenario in textbooks is when the auditor discovers assets or expenses on the books or returns that can't be traced back to the only cash account and may indicate other hidden cash accounts and activity. I'm not saying this is your client though.

Something else comes to mind that I've actually seen is when a client uses a personal vehicle for business and trades it for a new one with that new vehicle titled in the business name, thinking of all the deductions it could create. Have you seen the title, registration document, or insurance bill listing the vehicle? Perhaps the prior accountant was creative and booked the vehicle and "loan from shareholder" was the balancing entry of the trade-in value of the personal vehicle and/or new vehicle's loan payments being paid personally.

-

2

-

1

-

-

I, too, agree with everything Margaret said and Lee too. I'm sorry for all you are dealing with and hope that lightening the work load sooner than later will make life more manageable.

Many of us put others' needs ahead of our own wellbeing, as do I much of the time, but we have to be at our best to best care for those we love.

-

5

-

-

Run! If you offer advice on this at all it could constitute beyond tax advice into legal advice, and you definitely don't want that kind of risk exposure. I doubt your E&O or malpractice insurance would cover you.

No matter the attractiveness of fees or having off-season additional work, imho this client is NOT worth the risk.

-

5

-

-

2 hours ago, Sara EA said:

The 3115 will handle all the missed depreciation. Since the adjustment will increase current income, I believe there is an automatic election to spread the income over four years.

No, a correction for cumulative missed depreciation expense will be an additional reduction to Sch E and create an overall passive activity loss from the 2 properties.

Reread the original post where Tom estimates the total of missed deductions to be in the 170K range and current income is only about 20K.

-

5

-

-

Thinking that through, that does make sense because any loss that could have been used wasn't used for any tax benefit and would still be c/f, so yes, in a vacuum in the current year of correction.

-

1

-

1

-

-

Tom, obviously one goal is that, at the end of all calculations and current year's depreciation, that the accumulated depreciation and NBV of the assets are correct, and . . .

the second is that any PAL carryforward reflects the actual amount as if everything had been reported properly in the first place. Hope someone will chime in if my reasoning is incorrect on this part, but I believe that it may be necessary to make some adjustment to the PAL for any years where the taxpayer may have been allowed the special $25K allowance if the MAGI was under $150K on a joint return, or half those amounts on MFS returns. Were there any years where that may have been the case?

Another 2 thoughts - AMT calculations, and I hope you are getting a healthy retainer for this work.

-

2

-

-

4 hours ago, BulldogTom said:

How about putting the 481(a) adjustment on each respective Sch. E which will create the suspended passive losses you are trying to get to? Actually, this was my first thought, but I believe the IRS is looking for the 481(a) adjustment on the Schedule 2 - Adjustments to Income. If I put it on the Sch. E, I get the expense where the expense was meant to be. I like the symmetry of this approach, but I think the IRS prescribes otherwise and I can't nail it down for certain in my research.

On the other hand, if I put it on 1040 Schedule 2, I can generate an NOL and still use it to offset gains if she sells the rentals. Something just seems icky about doing it this way....

Tom

Longview, TXSince the accounting change for the error from impermissible to permissble method has gone on for more than the second year, amending would also be incorrect. The proper method is to file form 3115, code 7 if the assets have not yet been disposed of, and the 481 adjustment that will be negative should be shown on Sch E. Doing so will put the prior years' adjustment into the category of a passive activity loss (as if) the depreciation and PALs had been calculated correctly all along, and then take the current year's depreciation on the proper line of Sch E.

If the assets have already been disposed of, use code 107 on the form 3115 that basically eliminates the allowed or allowable "penalty" of never having taken the deduction but having to use the reduced basis at sale.

-

4

-

2

-

-

Congratulations to you and your family, Catherine!

-

2

-

Is anyone in our group a Social Security expert, or taken any courses?

in General Chat

Posted

I never suggested that you don't.

What I said was: