Leaderboard

Popular Content

Showing content with the highest reputation on 06/22/2025 in all areas

-

No, the losses in year of death are handled like any other year. Any capital losses that are unused (those that would carryfwd if the person lived) are lost. They die with the decedent.7 points

-

That's correct. What this means is that the final 1040 can show up to a $3,000 loss (just like usual) and any remaining loss carryover is lost. The planning opportunity mentioned is where a surviving spouse can sell capital assets having a gain in that year of death so that the otherwise unused losses would offset those gains. Example: your client is allowed $3K of losses allowed in the current year and $25K losses unused that are going to be lost. The taxpayer (prior to death) or surviving spouse any time during that year, if filing MFJ, could have sold other capital assets having GAINS up to that $25K with no additional tax effect. If single, that client could have done that in prior years or in the final year prior to death to use up the losses so that they aren't lost. For a single taxpayer where someone has a POA and is aware of the situation, that person could so initiate such a sale of capital asset prior to the taxpayer's death.2 points

-

Also see this article in The Tax Advisor: https://www.thetaxadviser.com/issues/2019/apr/llc-spouses-partnership-joint-venture/1 point

-

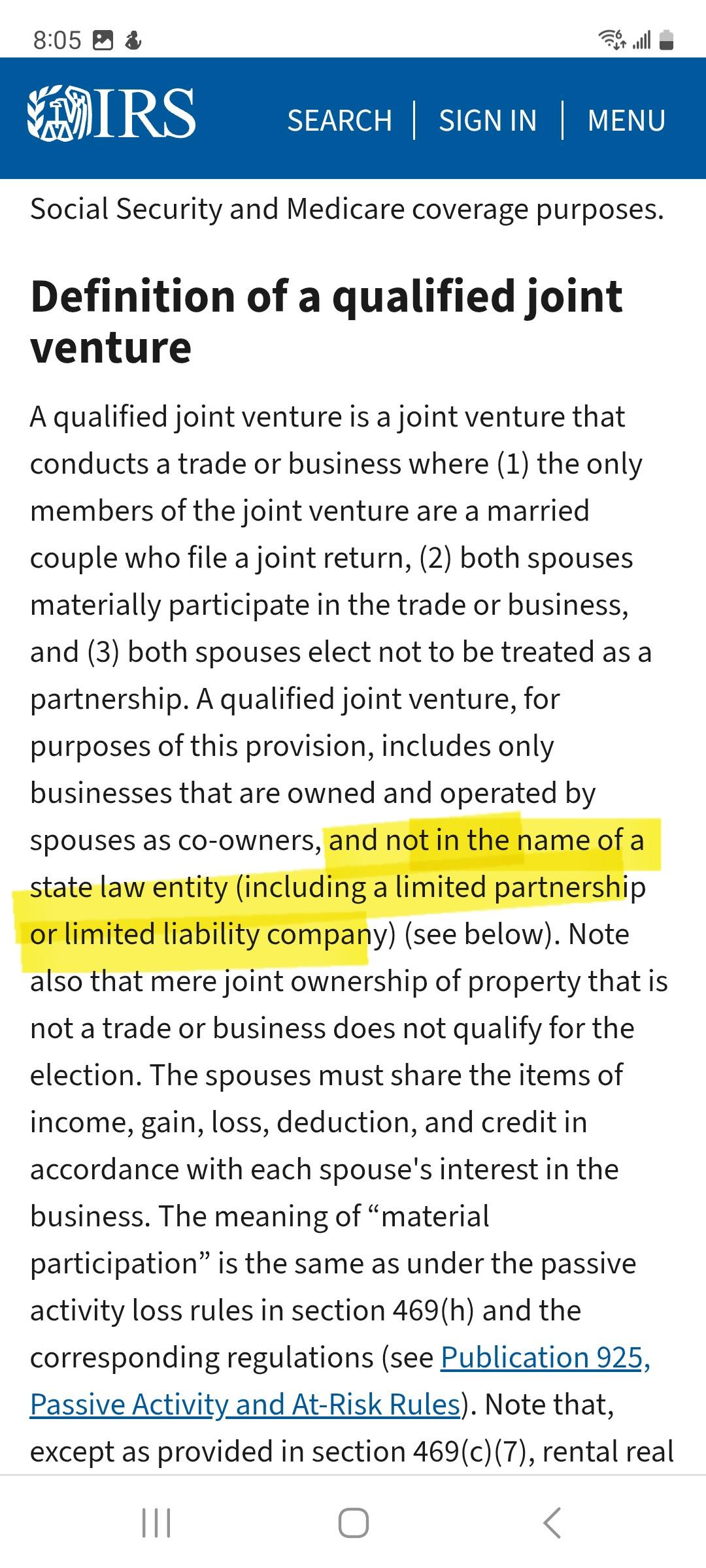

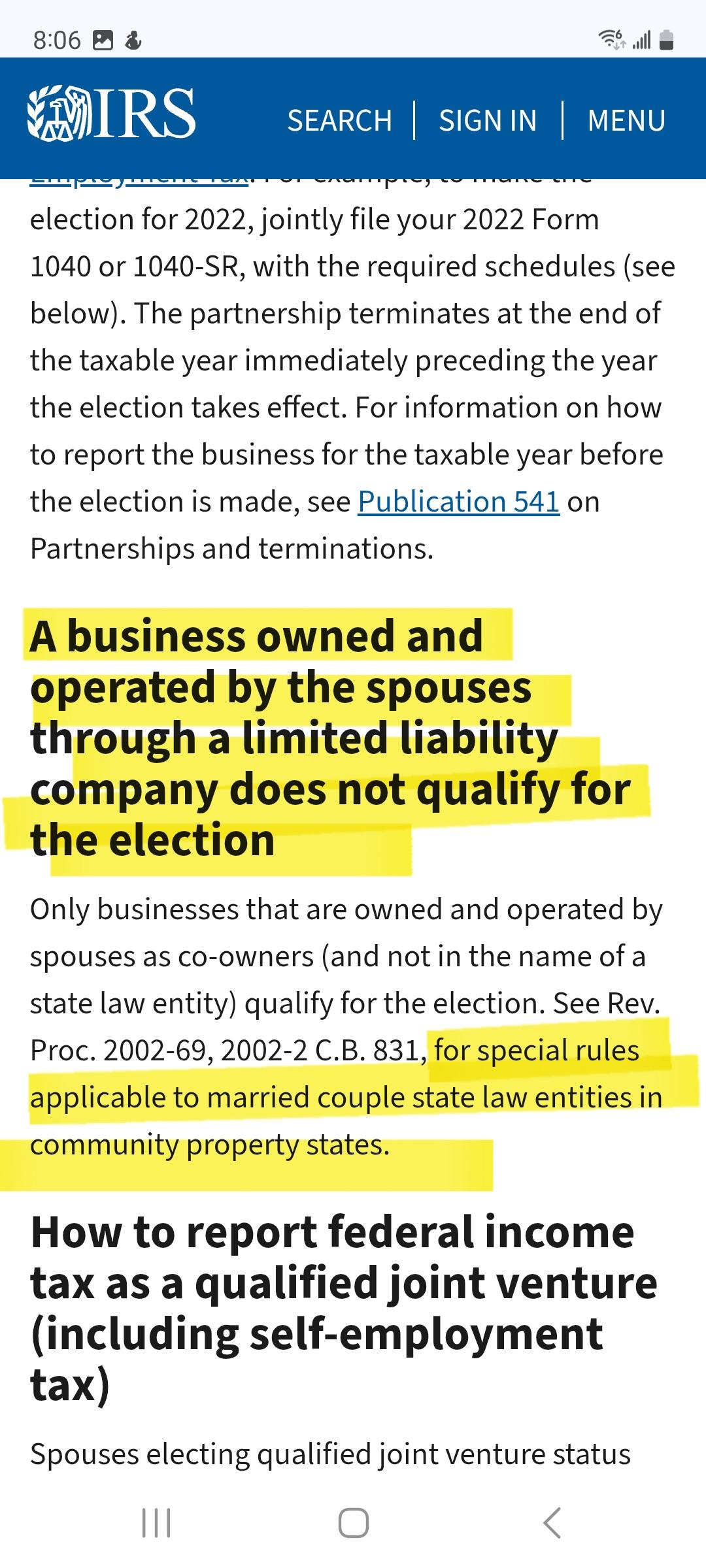

@DANRVAN Dan, IRS information page on QJVs says it can't be held in a state-recognized entity such as an LLC. Are these IRS pages incorrect? This rental the OP asked about is in an LLC owned by the rev trust. According to the original post, this is in a NONcommunity property state. Do you still think it goes on Sch E and not on 1065?

1 point

1 point