Unread Content 30 Days

Showing all content posted in for the last 30 days.

- Past hour

-

Tax items in reconciliation bill

Lynn EA USTCP in Louisiana replied to kathyc2's topic in General Chat

a local CPA contacted me late last week for my comments on the proposed raise in the SALT cap to $30,000. I advised her that in all my 36 years of practice I've never commented on a proposed bill. -

Standard response to client inquiries: there is no sense in discussing anything until a bill has been passed and signed. Until then, all bets are off.

-

I also charge $25 - $50 for dependent returns, with the option I keep for myself to give them a courtesy discount down to $5 or $10 or even $0 (say if the kid had one W-2 and $27 in withheld tax). But I want to see it before I price-quote, and anything that involves credits, kiddie tax, and multi-state issues is not done for a measley $50.

-

It looks like the "Windy" format.

- Today

-

The DOR refers to OAR 150-314-0435 with respect to Market Based Sourcing

-

The 2023 IT-201-X can be e-filed and any NY schedules that are normally included with the IT-201 would be included.

-

I go back quite aways myself as I like many moved from the Maine produced software (Saber?) to ATX. I miss hearing from Rita and a number of others I no longer see post. I got ready to renew my software this AM and got a threatening email from WK that I appeared to be attempting to access my account from different locations! I had to replace my older computer about a month ago and suspect that is the problem. I have had no small difficulty in connecting with anyone at ATX. Unable to get my rep. What a hassle ! Finally got a call back from tech support which hopefully will resolve the problem. She advised that they had sent out a number of these emails so I am evidently not the only one. This after over twenty years as a client.

-

What is CA's rule for preparing CA resident tax returns by out of state preparers?

-

I agree that in your example your fee could be considered an out of state source of income. However, I do not see any authority which would exclude it from your Oregon taxable income under ORS 316.048. Since the starting point is federal AGI, I am not aware of any provision to subtract it out for determining Oregon taxable income. Also, I don't see any reason why income from non-income tax states would be treated differently from states with income tax for Oregon taxable income, since Oregon taxes all sources of income, but allows a credit for tax paid to another state.

-

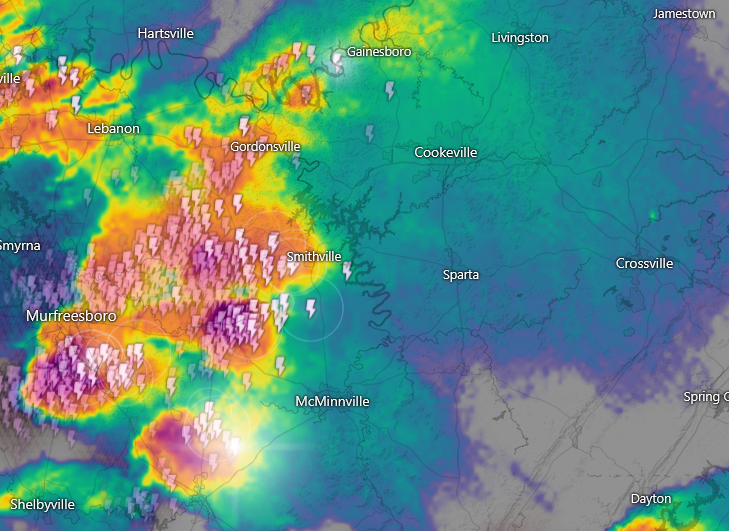

Tornado warnings all afternoon for Tennessee. Damage reports just now coming in. We're OK in Manchester - about an hour plus away from Rita.

-

Oftentimes the child is a student somewhere who has income in three states! Our fee for dependent returns is $50, like Patrick trying to avoid them claiming themselves and leaving us with a mess to clean up. More if the child has investments, plays with cryptocurrency, or has income in another state.

-

The rule in CA is "where the benefit of the service is received, that is where the tax lies". In practice, it means that any client who is a resident of CA at the time I prepare the tax return received the benefit of that service in CA. Therefore, the income I received from that client is taxable to CA. Even if they come to my office in Texas, CA considers the benefit received in the state. I have a few clients that are non-residents of CA but who still have CA sourced income. Because they do not reside in CA, the preparation of the 540NR is not sourced to CA and I don't pay tax on it. The benefit of the service was received in their home state. I think OR is pretty much spelling out the same schema for their income tax sourcing rules. Tom Longview, TX

- Yesterday

-

There are so many online and remote services now that the question arises where is the income nexus. Market Based Sourcing says if I whose business is located in Oregon prepare a tax return for a resident of Seattle WA, that the income nexus is where the services were received instead where my business is physically located. Another example: My accounting software is online which is also used by my larger business clients. This accounting service provider is headquartered on Long Island NY, but the actual software is hosted by Amazon Web Services in some server farm at an unknown location. Market Based Sourcing says that where the service is received is the key nexus location. Frankly, it's a new idea to me.

-

@Abby Normal what website did you get that radar image from. I have not seen one like that before. @RitaB take care of yourself. This spring the weather is not fooling around. Tom Longview, TX

-

Rita's got a storm headed her way.

-

I think I follow what you are saying now. For example you prepare a tax return for a Washington resident. You are saying your fee is not subject to Oregon Income tax? Your not talking about whether the client has Oregon sourced income but whether you do for your services?

-

Here is a Tax Advisor article about "Market Based Sourcing" which explains what the DOR presenter was discussing: https://www.thetaxadviser.com/issues/2012/nov/schadewald-nov2012/

-

I am still not following you on this Still subject to Oregon tax, but not subject to the Oregon Preparer rules as I see it.

-

I just took a CPE class where the presenters were ODR employees called "DOR Tax Professional Liaison." This was under a topic called Market Based Sourcing. My post was paraphrase was what the presenter said. Please see pages 2, 3, & 4. https://www.oregon.gov/dor/programs/taxpro/SiteAssets/Pages/meetings/Handout B%26W.pdf

-

There is no other reason!

-

Per the proposed rule notice: NEED FOR THE RULE(S) The proposed new and amended rules were made necessary, among other things, by changes in the technology that may be used by tax preparation businesses for the preparation of personal income taxes. Oregon Tax Preparation Businesses, who take in more work than their trained preparers can handle have, more than occasionally, been found to be reaching out not to other Oregon Licensed tax practitioners for assistance but to tax preparation businesses located outside of the State of Oregon – businesses whose employees have no training or expertise in the preparation of Oregon personal income taxes and as such pose a significant consumer protection risk to unwitting Oregon taxpayers who thought they were turning their tax information over to an Oregon Licensed Tax practitioners for the preparation of their Oregon Personal Income Taxes.

-

I am not following you on this. If they have Oregon source income what has changed? They can have their returns prepared out of state, but still subject to Oregon tax as I see it.

-

The proposed rule 800-002-0000 states "(1) An out-of-state unregistered tax preparation business whose employees or contractors are not exempt from licensure under ORS 673.610 may not contract to, and may not solicit or advertise to, prepare Oregon Personal Income Tax Returns for Oregon residents, or maintain a physical or electronic Oregon drop box location for delivery and pick up of materials pertaining to preparation of Oregon Personal Income Tax Returns for Oregon residents, unless the out-of-state tax preparation business registers with the Board and maintains an Oregon Licensed Resident Tax Consultant(s) on its payroll who is assigned to supervise the preparation of all Oregon personal income tax returns. ¶ So it in that situation is sounds to me that since the taxpayer is no longer an Oregon resident the rule would not apply; even if he/she had been a full time resident for the tax year, but moved out of state and were nonresidents at the time of filing.

-

You are in a different world. $50,000 for new will not buy much of a tractor for an average operation in my area, and will not hold it's original value for the amount of use it will receive. In any case, the original cost is a moot point in determining fmv at DOD, it needs to be done by an independent third party.

-

I have had a couple of situations wherein I have changed S-Corps to LLCs or QJFs just to simplify things for small business clients. This may not make sense to some of you, but I always think of what is best for the client before what is best for me.