jklcpa

-

Posts

7,153 -

Joined

-

Days Won

403

Everything posted by jklcpa

-

8582 must be produced to determine the correct amount of net loss to use at the bottom for the limitation, if that actually applies. What boxes are checked on the input for the activity? What is the modified AGI being used? Have you checked to make sure that MAGI is below $150K, and that you aren't basing your statements on AGI? I doubt Drake is wrong and is probably doing what you are telling it to do based on your input.

-

Tom, I have not done one myself but took a look at the instructions. I think it goes in section B for losses from business and income producing properties. Then, take a look at instructions for line 19 where it says to include all of the details you have for it if claiming a loss from fraudulent investment schemes that are not Ponzi-type and are not filling out section C. See what you think of that after looking at those instructions. That's the best I could make of it.

-

You will need to file the WV return and report the sale of thr property and show the amount of tax withheld as a payment. I haven't looked at WV instructions but it is customary to include a copy of the form showing the tax withheld. Then, MD will also tax the sale of property because your client is a MD resident. MD allows credit for taxes paid to WV on everything except wages, just as Lion said. Use form 502CR.

-

NT: are we this weird, or this amazing? or both!

jklcpa replied to Catherine's topic in General Chat

Yes to both weird and amazing. -

He would have to sign if that local return is on a joint basis. I don't know which jurisdiction, but those are usually for earned income. If that is the case and he has no PA earned income, they could file the local EIT returns separately, each signing their own. She would file her own and sign it. If he has no earned income and has permanently moved out of PA, he should file his marked "final". The generic local return has a place to give a reason for not having to file that in future, such as "retirement" or moved out of jurisdiction. If you have the preprinted form from the local tax authority, the one printed in red drop-out ink, there should be account #s above each column that belongs to each of them individually.

-

I agree with you. In the cases where not required, the returns are filed without those schedules, but I do prepare and print the Schs L, M-1, and M-2 for my file. That time is minimal, and excluding from the efile is a matter of unchecked a box.

-

None of the examples in the original post would need to include Schs L, M-1, or M-2. Your friend is correct. Both components must be over $250K to require the schedules. The test is NOT with them added together.

-

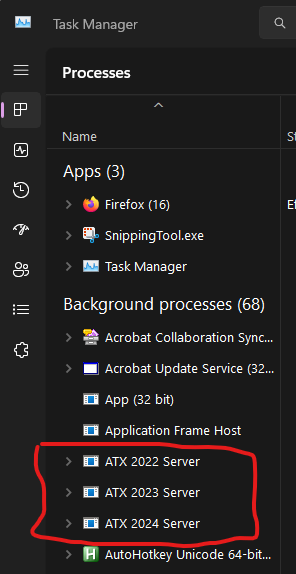

These are posts from Abby Normal as posted in another topic. First post: "Not having a full and complete backup of all of your files is foolish. In addition to backing up the entire Wolters Kluwer folder, you should at least backup your documents and many other things in your Users folder, plus anywhere else you keep important files. It's important that you end the ATX servers, all of them that are running, before backup up the Wolters Kluwer folder. Occasionally, I turn off all the ATX servers and copy the entire Wolters Kluwer folder to My Documents and then it gets backed up with all my other documents. I name the folder Wolters Kluwer yy-mm-dd and keep the latest 3." Second post - to turn off ATX Servers: Bring up Windows Task Manager and end the ATX Servers tasks. You end them by right clicking on them and choosing End task, or by selecting them and pressing the Delete key (DEL). Knowing how to end or restart tasks is an essential ATX skill. To start Task Manager, you can use the menu and type 'task' or right click the taskbar and choose Task Manger or my preferred method, Ctrl+Shift+Esc.

-

- 4

-

-

For future use for everyone using ATX, I'm going to copy Abby Normal's instructions to a new post of how to backup ATX data outside of the program and pin it at the top of general chat.

-

I didn't know this. IRS IP PIN replaces two old ones

jklcpa replied to Pacun's topic in General Chat

You mean the IP PIN, and yes, the most current one issued is the one to use for the current year being filed and the 2 prior years. -

I had my sister in law's birthday off by one day and by one year too! For almost 50 years I thought she and my brother were born the same year but is actually a year younger. Their return has never rejected since e-filing began.

-

I really didn't have to enter much data. On the main screen where 1095A input goes, I entered the spouse's name and information because she was the only one covered by a marketplace plan and I entered all of the figures for the entire year. Then I went to another input area and entered as below. Note that system asked for taxpayer's data and months only if enrolled in a marketplace plan, so I didn't enter anything there. Drake automatically calculates anything with an "=" sign and any entries in those boxes would be considered overrides, so that is why lines 11-23 are blank.

-

What program are you using? Are you overriding entries to try to force the figures to what you expect? I try to not override unless absolutely necessary. I entered in a practice return in Drake, so the names and SSNs are fake. Here's what it produced based on your information using the alternative calc for year of marriage. Pdf is 5 pages : 8962 & worksheets.pdf

-

Yes, you are correct that it should be "2". I read again about the separate family size for each that then gets added together for the 8962 line 1 entry.

-

Is the high ded plan for individual or family coverage? Which box is checked on the 8889?

-

I take back what I said earlier about MFJ should have a "2" on line 1 of the 8962. Line 1 of the 8962 should have a "1" in it for the spouse-only's tax family size that is being used for the alternative calculation. I think this may be causing your e-file error. Note - I have not reviewed any dollar amount entried that you may be discussing with others here. Here is a snip from pub 974 about tax family size when using the alternative calculation: Alternative Family Size Alternative family size is used to determine an alternative monthly contribution amount (see Monthly contribution amount under Terms You May Need To Know, earlier) on worksheets I and III, which may reduce the amount of excess APTC for the pre-marriage months that you must repay. When determining your alternative family size, include yourself and any individual in the tax family who qualifies as your dependent for the year under the rules explained in the Instructions for Form 1040 or the Instructions for Form 1040-NR. Do not include any individual who does not qualify as your dependent under those rules or who is included in your spouse’s alternative family size. When determining your spouse’s alternative family size, include your spouse and any individual in the tax family who qualifies as your spouse’s dependent for the year under the rules explained in the Instructions for Form 1040 or the Instructions for Form 1040-NR. Do not include any individual who does not qualify as your spouse’s dependent under those rules or who is included in your alternative family size. Note. You may include an individual who qualifies as the dependent of both you and your spouse in either alternative family size.

-

No, not the heir, but if you are preparing the final tax return for George & Elizabeth, they may be able to finally use some of the suspended losses. The property is considered disposed of on their final personal income tax return. Below is the paragraph that explains how it would work, and that is taken from this article by The Tax Advisor: https://www.thetaxadviser.com/issues/2017/jan/carryovers-death-spouse/

-

Do you have a "1" on line 1 for the size of the tax family? If married, that should say "2".

-

Margaret, those are line references on the 1040, not boxes on the 1099R.

-

The 1099R appears to be correct with respect to box 2 showing -0- as taxable. As I said above, line 4a should have $5623 on it, line 4b -0-, and do not fill out or include form 8606 as that would be wrong to do so. Code T is telling you that no penalty applies. I'm curious, is ATX trying to create a form 8606 for this, or is that you trying to use it because it is showing basis there?

-

You shouldn't need to fill out the 8606 at all. Software should enter gross distribution on 4a, and 4b should be -0-. I agree with Kathy that you are missing a checkbox somewhere. 1040 instructions for lines 4a and 4b, under Exception #2 says Exception 2. If any of the following apply, enter the total distribution on line 4a and see Form 8606 and its instructions to figure the amount to enter on line 4b. 1. Doesn't apply to your situation 2. You received a distribution from a Roth IRA. But if either (a) or (b) below applies, enter -0- on line 4b; you don’t have to see Form 8606 or its instructions. a. Distribution code T is shown in box 7 of Form 1099-R and you made a contribution (including a conversion) to a Roth IRA for 2018 or an earlier year. In fact, the 8606 instructions for Part III, line 19 says don't include on line 19 any of the following, and item #4 says: 4. Distributions made on or after age 59½ if you made a contribution (including a conversion or a rollover from a qualified retirement plan) for any year from 1998 through 2019.

-

efiling Amended return with insufficient address information

jklcpa replied to Mike T's topic in General Chat

OP's software must require the address, or at least the zip code be valid, to pass the error checking for e-filing. Does the client have a paystub? Or just put in the city, st, zip where the client worked. That won't affect the return's figures and will allow e-file to process. -

efiling Amended return with insufficient address information

jklcpa replied to Mike T's topic in General Chat

The client should call employer for the information, but if that isn't possible you could add all the W-2 income together as one entry into your software and e-file that way. Detail of each individual W-2 isn't transmitted to IRS with the e-file. In the explanation for the amendment, just put that one W-2 with taxable wages of "$XX" and fed witholding of $XX was omitted from the original return. As long as the totals are correct, it should be OK from IRS perspective. You just have to make the software behave. Which software are you using? -

It's always possible that these small companies mailed the W-2s to IRS instead of SSA. It's hard to believe that 3 companies for one client would do that though. I agree with Kathy that something seems off.

-

If the carryover doesn't match anything you expected, I would go back to the 2023 program and look at what return it is now generating for this client that may be affecting the rollover of data. Compare that return being generated to the return actually filed. Perhaps there is an entry in the 2023 system that doesn't belong?