jklcpa

-

Posts

7,153 -

Joined

-

Days Won

403

Everything posted by jklcpa

-

When I read posts like some here in this topic and others, and I think back to the workload I endured in my earlier career, I worry about some of you and about us as a profession overall. I haven't made nearly the amount I could have for whatever talents I have, but I have made a concerted effort for a healthier work-life balance and am happier because of those choices. This work can be extremely rewarding, but I believe that it shouldn't be at the expense of our health and well-being. I wish you all well, hope that you recover quickly, and are able to enjoy some quality time away from the office. I also hope to see you here in the off-season as we continue to work at a less hectic pace.

- 14 replies

-

- 13

-

-

If someone did that to me, I wouldn't have wasted an hour and may have considered not continuing on with the client, all depending on the tone of the lecture and insistence. Probably not over rounding though. Twice in my career I had returns ready to file, took them back from the client and disassembled them, handed original source documents back, and showed the (former) client the door. However, it was people who had outright lied, insisted I file a certain way, and when I refused to file fraudulent returns, accused me of not knowing what I was doing! Fine, they could go find someone else!

-

You already have the answer for the federal superseded through ATX, but this topic came up earlier this season, and at that time when I checked, there were only three states (CA, UT, NY) that accept superseded individual returns. That means that if your client's state return(s) also requires correction and isn't one of those three states I listed, then you will have to create a separate file for the state amendment. It may be easier to process by amending both the federal and state at the same time.

-

Faulty AI and no human to error check and correct?

-

But if the actual method is used in the first year, then the client must continue to use that and can't ever switch to cents-per-mile method.

-

I'm waiting for it to go to a second page!

-

I may use that on a difficult meeting tomorrow!

-

What Abby said, plus if prior preparer changed software providers without conversion, the LTCL c/o entry may have been missed.

-

PA has its own sch K-1s for either resident or nonresident partners or shareholders. Do you have a PA NRK-1 ("NR" meaning nonresident)? The PA return should back out the federal information and pick up the activity reported on the state NRK-1. Hope this helps.

-

Without researching, I'd say that this isn't any sort of apportionable item or a corporate-level item that can be attributable to nexus in the client's nonresident state, but rather is a shareholder level gain based on individual's basis. There are a few states that tried to impose a tax on similar gains from partnerships (distribs in excess of outside basis) for partners (CA, ID, NJ, OR), but not KS as far as I know. I would treat this as taxable to the resident state. What is the nonresident state?

-

Sometimes clients hear what they want to hear. If other withholding or estimates were already sufficient for 2024 to meet the safe harbor, are you sure that the previous preparer didn't really say that if they didn't pay tax on the gain during 2024 that they wouldn't have the underpayment penalty? That could be the case here, a year later, especially when a client doesn't fully understand and aren't talking with the original messenger that can revisit the conversation and information or advice she discussed.

-

The Wikipedia link from my first post has links and references to the 2 immediate predecessors, one of which was RockTenn. RockTenn's wiki page has the company's history of a merger in 1973, so that is probably what your client's mother owned when she passed in 2001. RockTenn came from a merger of 2 other TN companies, one with history going back 125+ years in Nashville. Maybe some of the history on that page will help you figure out which company your client had to start with. Does the client's county register of wills have archives of estate filings that could be retrieved? IF the gain is substantial, it may be the most expedient method to get that information for a small fee rather than trying to recreate something you are unsure of or can't truly document.

-

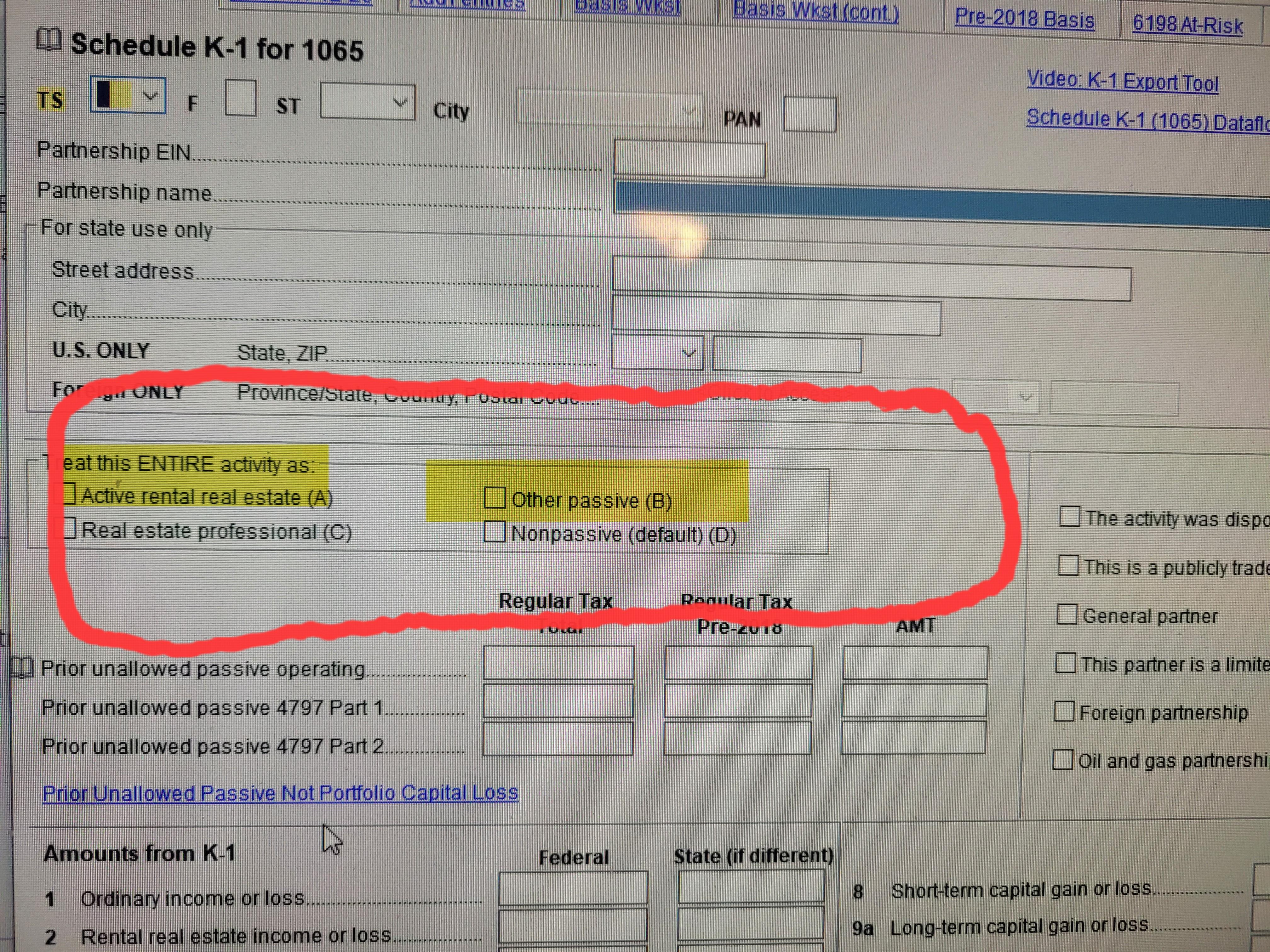

The box I am referring to has nothing to do with PTPs. You either have nothing checked in this section shown or have the default checked which is "D". Again, Drake is allowing the loss as nonpassive because no box is checked or is defaulting to "D" and is putting it in the nonpassive column on pg 2 of Sch E. IF you want the the loss to be subject to the PAL rules, you must check either box "A" or "B" that I have highlighted. Checking either of these will produce the form 8582, and 8582 worksheet, and possibly a PAL worksheet. If your client has active participation, check box "A" and the loss should carry to line 1b of the 8582 and will be disallowed for the current year, carried fwd to future, and current Sch E should have a -0- on it. Checking box "B" for passive activity will also produce the 8582 with the loss flowing to line 2b. Again, loss should be disallowed and carried fwd with the current Sch E having a -0-.

-

Looks like it was under another name and became Westrock through a merger. You may have to work backwards from the # of shares now to what was originally held before looking up the historical prices. Found this on Wikipedia that may help, if this is the company you need data for: https://en.wikipedia.org/wiki/WestRock

-

What is listed as the "type" of partner? Does it say "individual" or does it say "individual passive" or "passive"? Drake will put the loss in the nonpassive column and carry, allow it, and carry that loss to 1040 Sch 1 if you check "Nonpassive (default) box D" on the K-1 input screen. If you believe this is wrong and that the loss should be subject to the PAL rules, then you need to check box B for "other passive" on the K-1 input screen. I still don't think Drake has a programming error. It is doing what you are telling it.

-

Well, your taxpayer A would have 8582 because of the passive nature, but the MAGI already exceeds $150K so no loss should be allowed during the year unless there is a disposition or related gain that it generated. Taxpayer B, you said nonpassive loss with high AGI. Is this a real estate professional that could be materially participating? Is the amount also shown on Sch E, pg 2, line 43? Did Drake produce an MAGI worksheet or an 8582 worksheet. That 8582 worksheet looks almost identical to the form itself and should give you an idea what is happening on the return.

-

I do breakout the charges on my billing, and the partnership gets a separate bill anyway.

-

I'm pretty much in line with your pricing. I have those easy ones that are under $200 too. Then there are ones to deliver where the total will be on your higher end. All the bookkeeping for an entire strip shopping center, lots of payments for expenses charged on credit cards, quarterly tenant passthrough billings, quarterly gross receipts tax filings, had a casualty with insur reimb when a tractor trailer ran into the end of the buildings with structural damage. It's an LLC taxed as partnership, and then preparing the individual owner returns with other investment properties too. Very high income. Great clients that were with the firm I worked for in the 80's and came to find me when that owner retired and have been with me since '96. Will be delivering to their home for no charge, gives me a break to get out of the office for a short time too.

-

Not going to kick you off, Tom, but I can see I may be deleting posts or locking a topic soon.

Not going to kick you off, Tom, but I can see I may be deleting posts or locking a topic soon. -

A couple of years ago I agreed to prep a very simple return for an employee of a business client. Prior CPA preparer charged btwn $450-$500 for a return with one W-2, two SSAs, one 1099int, one 1099R, standard deduction...AND IT HAD ERRORS. HRB would have been even higher around here! Former preparer wouldn't return their calls, and they took it there in person and former preparer refused to acknowledge the error or fix it. These people are really, really nice too. They were really nervous coming to pick up the returns and the amended ones from me, naturally being worried again about the CPA price. I was nowhere near that fee!

-

Well I am too and most of my clients aren't anywhere near in this range. I am serioisly curious though what some others of you would charge for a return package that included nine returns that included splitting the income and deductions manually for those states to be correct, had 2 complicated projections containing 3 scenarios and done at different times during the year, had to create the mortgage amortization schedules and tie in the balances for one that settled midway through the year, another starting during the year, so 3 mortgages altogether and about 2 million in debt. I spent at least half a day on all that not including the phone calls or the meeting with them at the end to deliver and explain it all, the handholding and questions afterward, and finalizing the efiling. How much would you charge for more than a 1/2 day of work in total?

-

Tom, does ATX allow attachment of a pdf? I can scan and attach any statement I want. I just have to fill in three things: a basic explanation or form it relates to, a reference (such as the form, pub, code, reg, memorandum) and the name of the file with a .pdf extension.

-

There are lovely people I serve too though. I delivered a return yesterday to a client/friend of almost 40 years. She's 95 now in assisted living. Return isn't *that* complicated but has half a dozen 1099Rs, one consol broker 1099 package with only 40 page or so, the bigger main consol broker 1099 package that was only 60 pages, and a PTP. We had a really nice visit and did some reminiscing. People like her remind me why I still do this work.

-

I would be in the $400-500 range too, depending on how much work I had to do on the rental and basis of stock. If the basis is printed on the broker 1099, that is less work than if the client brings in basis from an inheritance or older purchases where they've changed investment firms, etc. I had one that I started to list in the complaint topic and changed my mind. The guy did not return to me this year because I charged him $800 last year. He'd been a client for more than 10 years and I cut him big breaks on the calls and projections, but not on the returns themselves, and I still undercharged him. He also owed about $60K on the federal alone because he has huge bonuses and never calls, and does stupid things like using retirement distribs to purch the beach property, and underwithholds or has no withholding on that income. Tax prep and other work included were for: high income earner W-2, so also had Medicare add-on tax, but not even $1 of interest or dividends so no NIIT, Sch A with SALT and mortgage limitations, sold 2nd residence which also had extended calls to fill out the form to avoid the state tax withholding at settlement, purchased another beach house, this one as rental but with lots of personal use, and didn't agree with explanation of expense limitations and argued that, 3 retirement distributions with partial rollovers and minimum withholding of 20% in the 39% bracket. These partially used for new beach house/rental, a complicated projection with 3 scenarios for a possible early retirement. Sent me a 200+ page booklet of explanations of these deals that he then demanded answers for within a day (the week I had the flu too!), multi-state as DE resident and working in PA, out of state credit and a daughter's return that was PY DE, PY NJ, and worked in Phila while living in each of those states, and then worked in NY city once fully moved to NJ. So with all of that, it was parent's Fed, DE, nonres PA, 2 complicated projections, and daughter's Fed, part-year DE, part-year NJ, nonres PA, and nonres NY and NYC returns. Nine returns in total. His other adult daughter left too. Charged her ~ $500. Similar BS with multi-state: She works in PA, husband in DE, they sold home in DE and moved to PA during year, has 2 children for the CTC and dep care credits with the documentation and due diligence, unemployment, std deduction for federal but each itemizing for DE on a separate basis, plus they live in a PA jurisdiction that has local earned income tax. So that one was joint Fed, 2 separate PA, 2 separate DE, 2 separate locals and figuring the out of state credits on those was a PITA. Not a word from either of them to know why they were unhappy. Those are the type I typically never take back because they were unhappy enough to leave and not give any courtesy to me after more than 10 years as clients and lots of free advice. I hope they are happy with their new preparer and higher fees, and if they contact me in future I will joyfully and firmly say "NO THANKS."

-

Yes, a horrible season. Getting the information from people seems to get more difficult each year, and no one likes the price increases when all I've done is raise the price to just stay even with my increased costs. Increased aggravation to make less than before? No thanks.