Leaderboard

Popular Content

Showing content with the highest reputation on 09/27/2023 in all areas

-

Folks who aren't well-positioned for retirement don't tend to listen to advice...they've already made up their mind to sign up ASAP.3 points

-

Kathy, of course there's nothing wrong with educating yourself, but I draw the line at sharing my certainly incomplete knowledge with someone who will use it for a life-changing decision. People should get solid advice from SSA (the folks there are really good in my experience) or work with a financial advisor--NOT their tax preparer. Over my career I have had several people question me about the tax implications of getting married. Really? I would think that people decide to marry because of love, commitment, to make a relationship permanent. Money might enter into a decision to do a prenup, but to get married? Talk to a marriage counselor, not your tax preparer.3 points

-

Surgent's detailed course descriptions include a breakdown of the potential credits for CPAs and EAs who will recognize those (NASBA, IRS...) Fwiw, I've taken the SS course by Bob Lickwar and found it helpful and informative but certainly not enough for me to want to create various complex scenarios for my clients.1 point

-

Neither do I. I got a good chuckle from that comment. Surgent has several. I think webinars led by Bob Lickwar are quite good. You can buy an unlimited package that is good for 12 months for $560.1 point

-

For me, studying my own situation has led me down many paths which might help others. Answering your own issues is a great first step, which will give you a place to start making notes to look at other paths. As above, my first advice is always to study death or disability tomorrow, and the results of prior planning or lack of will be a shock. That shock is great inspiration. I then looked at my death being at age 100, which is the actual average for my family. I slightly considered death at an age where waiting until max SS is gained, but for me, I discounted it as it only affected ME, not those I will leave behind (which is my personal priority).1 point

-

I don't think anyone else is an idiot. I do feel that I'm an idiot for not being thoroughly educated in tax-adjacent topics, such as SS, Medicare, retirement saving, investing, crypto, planning for like-kind exchanges, STR, vacation rentals, anything I haven't had to study in the past, etc. I know I don't have the knowledge or the time to give my clients the consultation they need -- but that there are people who can. I do talk a LOT about SS to my clients, but remind them I don't know any more than I'm telling them, that I gained my little bit of information by taking courses from experts in those fields, and suggest they consult experts in each field, that we can all work together to help them plan. I thought I was agreeing with kathyc2 that we need to help our clients plan (in my case, with my limited knowledge, help by recommending consultants that I've learned from) for retirement -- using SS as just one of their resources. Who do you all recommend that I take classes from to up my SS game? Any courses you recommend scheduled for November-December 2023?1 point

-

SS planning should be done starting from an early age. Meaning, get in 10 quarters. Check for accurate reporting. If an s corp, for example, maximize SS wages instead of playing RC games. JMO though. My opponent noon is based not on maximizing for own self, but to setup for the unexpected. Surviving spouse, surviving kids. Disabled self, spouse, kids. Etc. Comes from my grandmother collecting for over 50 years. Me being a surviving child. Daughter likely collecting 40+ years of ssdi based on my wages. Also still personally having one zero year dragging my calculations down due to a poor choice in my youth. i don’t see it as a need to beat private investment game, but a way to care for those we are responsible for. The average person is not going to beat SS if something unexpected happens. I don’t else a scenario where SS is left fallow. I know not all agree, and I know many who wish they had!1 point

-

Like I said, if you choose to not talk about SS with clients, that's fine. However, telling someone that chooses differently to "stay in your lane" is quite rude in my opinion.1 point

-

Exactly.... This is where I always get hung up.1 point

-

The goal should not be maximizing SS benefits, but rather maximizing wealth. Simple scenario: Benefits at age 67 are 25K. I'm assuming a 2.5% annual COLA. Waiting until age 70 and the combo of 8% a year bump and COLA and first year benefits are 33,914. If the person lives past age 80, they will receive more in benefits by not claiming until 70. If they die before 80 they will have received less benefits. By age 90, the projected benefit total is 809K for starting at 67 and 922K by starting at age 70. Looking only at the benefits, it looks like it's better to delay, correct? Instead, how about starting at 67 and investing the benefits for the first 3 years? I used 80% of benefits at account for any tax on amount to invest and used an annual return rate of 7%. Compounding the returns and the amount in this account is 272K at age 90. The non invested SS benefit amount is 732K, for a total of 1,004K. In this case, you end up with 82K more, plus the 272K can be passed on to heirs. Now, which one sound better?1 point

-

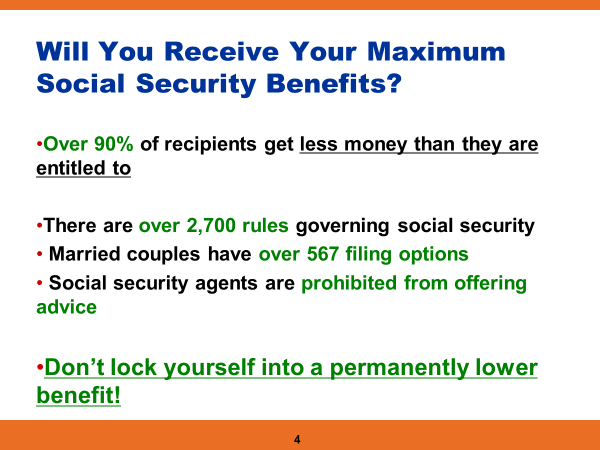

Send your clients to an SS benefits expert. Here's just 1 of Ash's slides from his presentation to the NY/CT-ATP June 2018:

1 point

1 point -

I always deferred most SocSec questions by recommending that the client go straight to SSA for answers. After I began drawing SocSec 7 years ago and navigated my own situation, I changed my policy. I now defer ALL SocSec questions by recommending that the client go straight to SSA.1 point

-

I think the SSA.gov has a lot of good information if you know what you're looking for. The Tax Book has a SS/Medicare book, or it's included in their Tax Library. I know I've done webinars in the past, likely either Surgent or Checkpoint. In a nutshell, benefits are based on highest 35 inflation adjusted earning years. There is software that you can buy to calculate this, or if you are an Excel person, you can calculate it yourself. One word of caution. When you get the statement from projected benefits from SSA, they assume you are working at the same level as past year until you collect benefits. This can be misleading for people especially for people who want to retire now but want to wait to take benefits until later.1 point

-

cbslee refers to a very specific exception where over $500 requires an appraisal if an item of clothing/furniture is NOT in "good used condition" or better. See tax code section 170(f)(16)(C). Without an appraisal value over $500, you cannot deduct such clothing/furniture at all. It's hard to imagine one item in poor condition being worth more than $500, but anything's possible, and you can deduct such items with an appraisal.1 point