Unread Content 30 Days

Showing all content posted in for the last 30 days.

- Past hour

-

Married Couple Revocable Trust Owns LLC in Non-Community Property State

G2R replied to G2R's topic in General Chat

Trust was setup years ago. LLC was just setup last year and owns the rental. I got the EIN letter from the client, they state 1065 as the expected form filing. -

I never received an early renewal offer, and they can't show that it was sent to me. Did everyone else receive an offer? If so, what was the pricing for Max all in?

- Today

-

But not unexpected or surprising.

- 1 reply

-

- 2

-

-

Copied from the TIGTA Report "FY 2023, cases worked by TAS generally met its acceptance criteria and taxpayers’ issues were fully addressed. However, we found TAS case advocates did not timely contact taxpayers or their representatives in 103 (63%) of the 163 closed cases we sampled. The initial and subsequent contact delays for these cases totaled an average of 146 calendar days late." "The National Taxpayer Advocate stated that TAS case advocacy is facing three challenges: rising case volume, new staff, and outdated systems." Well, this is really discouraging

- 1 reply

-

- 1

-

-

Married Couple Revocable Trust Owns LLC in Non-Community Property State

jklcpa replied to G2R's topic in General Chat

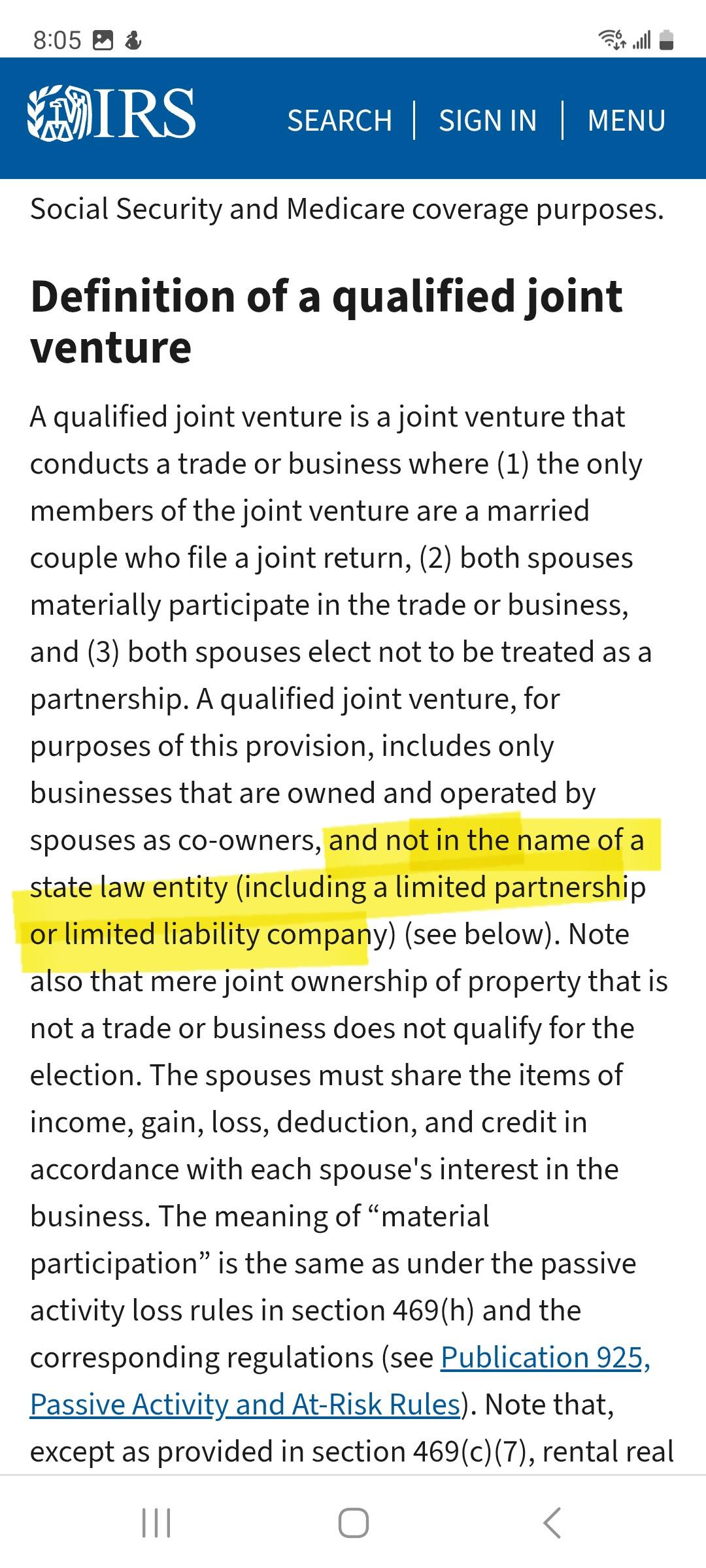

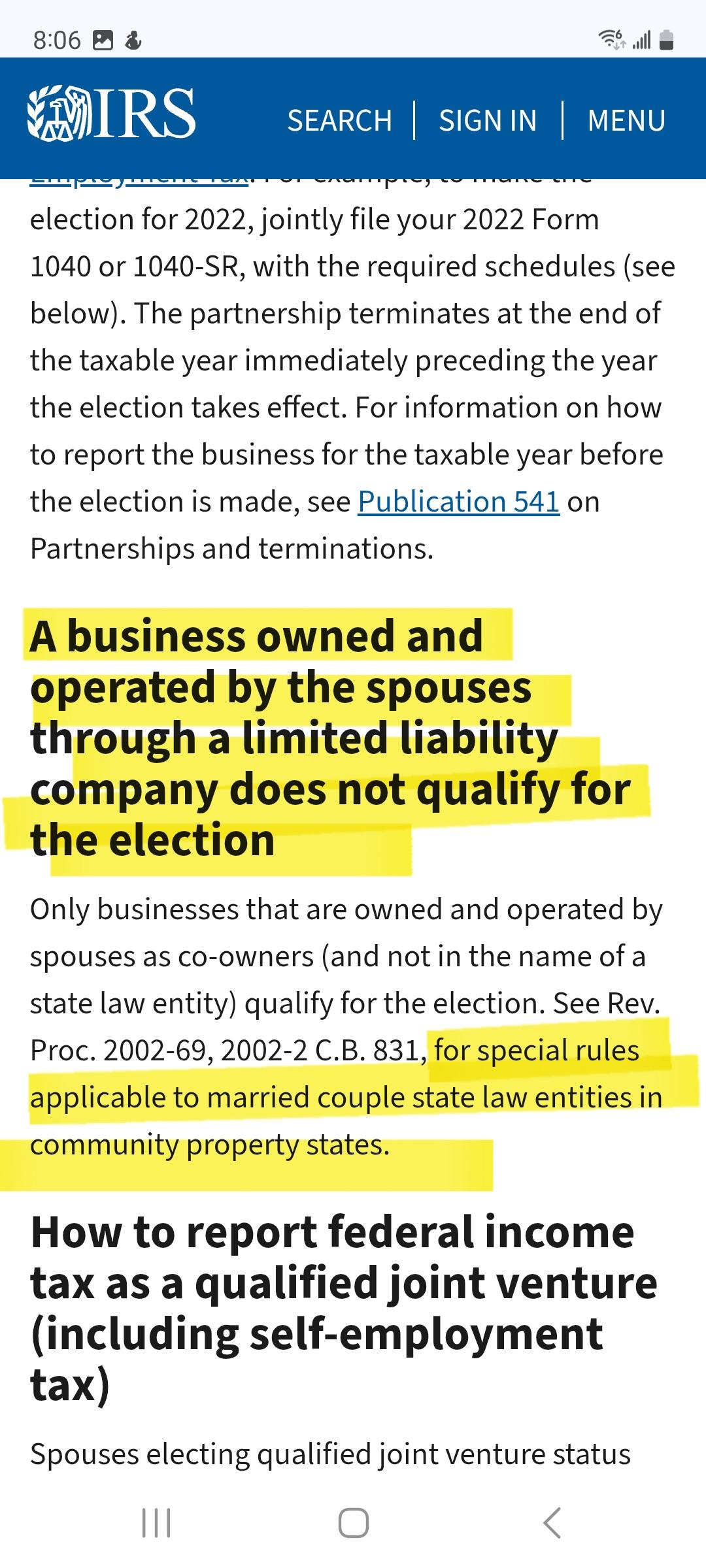

https://www.thetaxadviser.com/newsletters/2020/mar/married-taxpayers-jointly-owned-business/ @DANRVANThis is a second article from The Tax Advisor that disagrees with your interpretation by saying that MMLLCs are state entities that do not qualify to make the 761(f) election, and that goes on to make the separate point of an exception to those in community property states. I would still tell the OP to file a 1065. In Argosy, the court didn't need to consider that it was an LLC or not because there were previous filings as a partnership. ----------------- As to your H-W rentals in your state and the audit you mentioned, not all auditors are that good. Are these in LLCs? Even if not, did you make a 761(f) election for them? Do you check for material participation of EACH party each year without attribution of the participation of each to the other? Also from the same Tax Advisor article: -

Married Couple Revocable Trust Owns LLC in Non-Community Property State

DANRVAN replied to G2R's topic in General Chat

And for whatever it is worth, I live in a non-com-prop-state and have never ever seen a 1065 prepared for a married jointly owned real estate rental; always on a single Schedule E. The last audit I had involved a married couple with several jointly owned rentals, the issue never came up. -

Married Couple Revocable Trust Owns LLC in Non-Community Property State

DANRVAN replied to G2R's topic in General Chat

The code is the authority. Per 761(f): "(2)Qualified joint venture For purposes of paragraph (1), the term “qualified joint venture” means any joint venture involving the conduct of a trade or business if— (A the only members of such joint venture are a husband and wife, (B) both spouses materially participate (within the meaning of section 469(h) without regard to paragraph (5) thereof) in such trade or business, and (C) both spouses elect the application of this subsection." *************************************************************** Rev Proc 2002-69 is the IRS position: (tax courts are not bound by Rev Proc) ".02. Qualified Entity. A business entity is a qualified entity if: (1) The business entity is wholly owned by a husband and wife as community property under the laws of a state, a foreign country, or a possession of the United States; (2) No person other than one or both spouses would be considered an owner for federal tax purposes; and (3) The business entity is not treated as a corporation under § 301.7701-2. **************************************************************** -The code does not make any reference to community property or an LLC. -The RP refers to community property, but not to LLC's in contrast to the IRS webpage. -In Argosy Technologies, LLC, T.C. Memo. 2018-35, the husband and wife owners asserted that their business was a single-member LLC in order to avoid a levy to collect the Sec. 6698 penalty for failure to timely file 2010 and 2011 partnership returns. The taxpayers lost. - The determining factors in that case were the previous filing of 1065 by the plaintiffs and the failure to make an election under 761(f) as a QJV. - The facts that the plaintiffs resided in a non-community property state; and were an LLC were not mentioned in the opinion of the court. - Therefore it appears to me the court looked to the code for authority and was not bound by the RP stipulations. In answering your question Judy, yes I believe the IRS page is an incorrect interpretation of the tax code. If so, then they have failed to make the 761(f) election and must continue to file 1065. -

If the investment account was joint and originally funded jointly, half of the carryover losses belong to the surviving spouse and can be used on his or her future returns. The deceased spouse's half is lost forever after the final return. Many of us still have clients who lost a fortune in the 2008 market crash, pulled out of the market altogether, and will have to live to be 200 to use up the losses at $3k per year. That $3k limit has been around since 1978 and never adjusted for inflation.

- Yesterday

-

That's correct. What this means is that the final 1040 can show up to a $3,000 loss (just like usual) and any remaining loss carryover is lost. The planning opportunity mentioned is where a surviving spouse can sell capital assets having a gain in that year of death so that the otherwise unused losses would offset those gains. Example: your client is allowed $3K of losses allowed in the current year and $25K losses unused that are going to be lost. The taxpayer (prior to death) or surviving spouse any time during that year, if filing MFJ, could have sold other capital assets having GAINS up to that $25K with no additional tax effect. If single, that client could have done that in prior years or in the final year prior to death to use up the losses so that they aren't lost. For a single taxpayer where someone has a POA and is aware of the situation, that person could so initiate such a sale of capital asset prior to the taxpayer's death.

-

Herein lies my confusion. However, when you die, any capital loss carryover is lost. It cannot be utilized by your estate or surviving spouse except in the final tax return filed for the year that you die. Therefore, it’s important to use as much of the remaining deduction as possible in the final year (or in the years prior to death). There are planning techniques available to help accomplish this goal.

-

I should have clarified. This is her final personal return and not an estate return.

-

So the now deceased client can only deduct the $3,000 normally allowed per year. They must have changed this in 2017 perhaps.

-

Married Couple Revocable Trust Owns LLC in Non-Community Property State

Lee B replied to G2R's topic in General Chat

Also see this article in The Tax Advisor: https://www.thetaxadviser.com/issues/2019/apr/llc-spouses-partnership-joint-venture/ -

Married Couple Revocable Trust Owns LLC in Non-Community Property State

jklcpa replied to G2R's topic in General Chat

@DANRVAN Dan, IRS information page on QJVs says it can't be held in a state-recognized entity such as an LLC. Are these IRS pages incorrect? This rental the OP asked about is in an LLC owned by the rev trust. According to the original post, this is in a NONcommunity property state. Do you still think it goes on Sch E and not on 1065?

-

Married Couple Revocable Trust Owns LLC in Non-Community Property State

Lee B replied to G2R's topic in General Chat

We don't know when the LLC was set up or when the Trust was set up. Has the LLC previously been filed as a 1065 or as a Schedule E? - Last week

-

Married Couple Revocable Trust Owns LLC in Non-Community Property State

DANRVAN replied to G2R's topic in General Chat

An LLC has no bearing on tax reporting since it is the underlying entity that counts. In this case the entity is a Joint Revocable Trust, which is also disregarded for tax purposes due to its grantor status. Therefore the grantor is treated as the owner(s) for tax purposes. Since the husband and wife are the actual owners for tax purposes, they meet the requirement of sec 761(f)(2)(a) for a QJV as I see it. I don't see where community property state vs non comes to play under sec 761. Based on that, I would report on Schedule E. -

No, the losses in year of death are handled like any other year. Any capital losses that are unused (those that would carryfwd if the person lived) are lost. They die with the decedent.

-

I should have said are all of the losses deducted on the Form 1040 which would require possibly overriding the line item as using Schedule A the client may not have gotten the full amount taken off. It is a moot point as her itemized deductions far exceed the standard deduction but the ATX software shows only the $3000 yearly amount on the Form 1040 so I will simply deduct that from the total loss and show the remaining amount on her Schedule A. I think this is correct but I have not done one of these in many moons.

-

A client passed on in 2024 having some $25,000 plus in remaining capital losses. Are these deducted on Schedule A or on the Form 1040?

-

"Designates a person on the taxpayer's tax form to discuss that specific tax return and tax year with the IRS." My understanding is that this only allows you to discuss what's on the form submitted. It doesn't authorize the IRS to share any information with you or for you to represent the taxpayer. I don't believe that responding to a notice received by your client is covered by being a third party designee.

-

Two weeks ago I called the IRS in regards to a notice my client received which I have third party designee, guess what I had to conference call my client to discuss the notice. First in all the years of doing business, the payroll report was filed in April 2025 so it was not expired.

-

Married Couple Revocable Trust Owns LLC in Non-Community Property State

Abby Normal replied to G2R's topic in General Chat

I thought an LLC was an unincorporated entity because it's a partnership. -

No matter how many people they hire, it won't improve significantly until they invest in new infrastructure. I had to be transferred three times, over two hours, to reach the person who could access the platform needed to fix the issue. Once I got to the right person, it took 10 minutes to resolve the issue.

-

Married Couple Revocable Trust Owns LLC in Non-Community Property State

jklcpa replied to G2R's topic in General Chat

I worded that very poorly. I revocable trust can have biz prop that is QJV, but it can't be in an LLC, rather it must be operated in an unincorporated entity. So in your case, QJV would be off the table on 2 scores: because the rental is in an LLC and because the client is in a non-community property state. Sorry for the confusion.