Leaderboard

Popular Content

Showing content with the highest reputation on 03/16/2019 in Posts

-

Yes, it needs to be a PDF. Use the efile menu to attach PDFs to a return. Or just skip it. No one at the IRS is ever going to look at your PDF. Plus the PDF may be so large you'll have problem efiling it.3 points

-

All my LLC's pay $841 per year. $800 LLC fee and $41 for failure to make estimated payment. I don't know why I waste the paper and toner to print out the voucher every year. Tom Modesto, CA3 points

-

Yes, notes are assigned to a field. We use the date field at the top of page 1 on all returns for our general notes, since it's convenient and a field we almost never use. Review type notes should be in the field or form they are related to. Some users add the Permanent File form and type notes on one of the blank pages, or a blank statement page of the Elections form, but notes show up when you review a return and to me are the preferable way to go.2 points

-

I think Abby is referring to right-clicking on an input cell and choosing the menu item Insert/Edit note.2 points

-

It needs work:

2 points

2 points -

Thank you so much!!! I just tried it and am so happy! I could not find this in the KB but really should understand the REAL KB is right here on this board.2 points

-

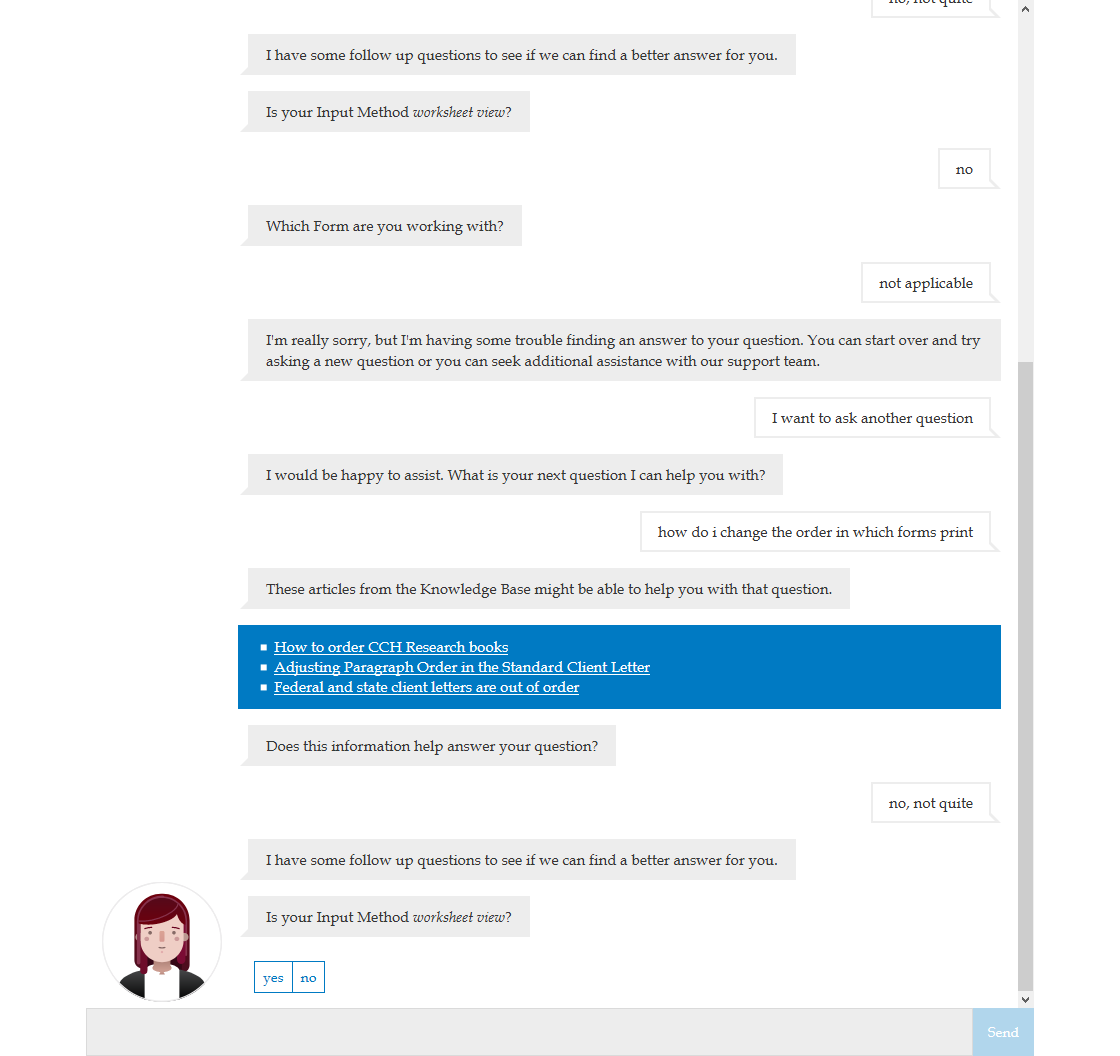

Highlight the form you want to move and press Ctrl+ up or down arrow. You can permanently do this in print packet edit as well, but that only helps new returns... unless you uncheck remember, print, close, re-open and print again (check remember at this point).2 points

-

I didn't even know about this feature. Been doing it the old fashion pen-and-paper way! Thanks for the tip!1 point

-

Do you mean in the 'a' box? I thought it was wrong, also, until I read the 1040 instructions for this year, and it has changed. ***If you have IRA distributions and/or pension and annuity payments, unlike in prior years when you entered these amounts on different lines, this year they will be combined and reported on the same line. IRA Distributions You should receive a Form 1099-R showing the total amount of any distribution from your IRA before income tax or other deductions were withheld. This amount should be shown in box 1 of Form 1099-R. Unless otherwise noted in the line 4a and 4b instructions, an IRA includes a traditional IRA, Roth IRA (including a myRA), simplified employee pension (SEP) IRA, and a savings incentive match plan for employees (SIMTIP TIP Need more information or forms? Visit IRS.gov. -28- Page 29 of 117 Fileid: … ions/I1040/2018/A/XML/Cycle08/source 14:16 - 24-Jan-2019 The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing. 2018 Form 1040—Lines 4a and 4b PLE) IRA. Except as provided next, leave line 4a blank and enter the total distribution (from Form 1099-R, box 1) on line 4b. Exception 1. Enter the total distribution*** My taxable amounts have flowed through okay.1 point

-

ProSystem fx has the virtual rep chat, also. First year. Only works if you're searching for a word or phase that's already in their KB. I usually start in their KB, anyway, so I've already done what she's doing. I used her a couple times; she suggested I go to live Chat after a couple of exchanges like you had above. So, now when I've already searched the KB, I go straight to the live Chat or the "write your own ticket." I'll try her again later in the year; she'll probably get better over time. Their IntelliConnect and newer AnswerConnect have gotten better over time.1 point

-

From my sleep-deprived memory, I think the "help" for abused spouses has to do with filing MFS withOUT having to pay everything back. Look for that exception within the form, maybe. That's all I got.1 point

-

Yes. There are permanent notes where we keep extensive info on the client, from the trivial (nicknames) to the crucial (don't forget state subtraction for ...). And there are review notes that must be cleared before you can finalize a return. We print the permanent notes to the back of our 'job sheet' for each return and check them off as we do them.1 point

-

A] 1120S Sched K line 16d, Jump to its detail worksheet to distinguish between cash or property distributions AND populate Sched M-2. Or B] 19 steps up from the bottom of the Pages & Worksheets tab of Form 1120S input screen.1 point

-

Well, either method mostly works. This year I've become inured to ATX's failure to reliably retain everything about the orders I arranged -- taking over an hour to do so at the beginning of the Season -- in the print packets. Fer instance, I slid *all* E-file Info tabs to the bottom of their categories, Federal and State, but in individual jobs those still pop up at the top or middle of the print order. Overall, I'm grateful that my PC is powerful enough that re-arranging PDF pages in Thumbnail view (Power PDF but Acrobat in my assistant's) takes only a few seconds at worst. (But I may splurge on a gamer-weight video card next go 'round, hoping to reach *instantaneous* in each and every graphic manipulation.)1 point

-

Marriage has consequences! Just ask me.1 point

-

Have you been doing th e8606 every year to show the basis and the total balance in the IRA's? Part of this is going to be taxable because you have to withdraw taxable (earnings, deductible contributions) pro rata with the non-deductible amounts withdrawn. In other words, you can't withdraw only the non-deductible contributions from a traditional IRA and then withdraw the earnings later. But the 8606 is the form that should calculate the amount that is a return of basis and therefore non-taxable. Did you complete Part I before you completed Part II?1 point

-

In the middle of the bill is what I believe to be new tax extender : Sec. 122. Exclusion from gross income of discharge of qualified principal residence indebtedness (sec. 108(a)(1)(E)). The provision provides through 2019 a maximum exclusion from gross income of $2,000,000 for a discharge of qualified principal residence indebtedness. Generally, indebtedness must be the result of acquisition, construction, or substantial improvement of primary residence. The provision also modifies the exclusion to apply to qualified principal residence indebtedness that is discharged pursuant to a binding written agreement entered into before January 1, 2020. Very interesting, how many taxpayers really need a $2,000,000 exclusion ? I'll bet there is a special favor behind the inclusion of this item!!!!1 point