Leaderboard

Popular Content

Showing content with the highest reputation on 03/13/2021 in Posts

-

But wouldn't it be fun if everybody amended their returns right this minute?5 points

-

Possi & and Tom, you have a very sick sense of humor4 points

-

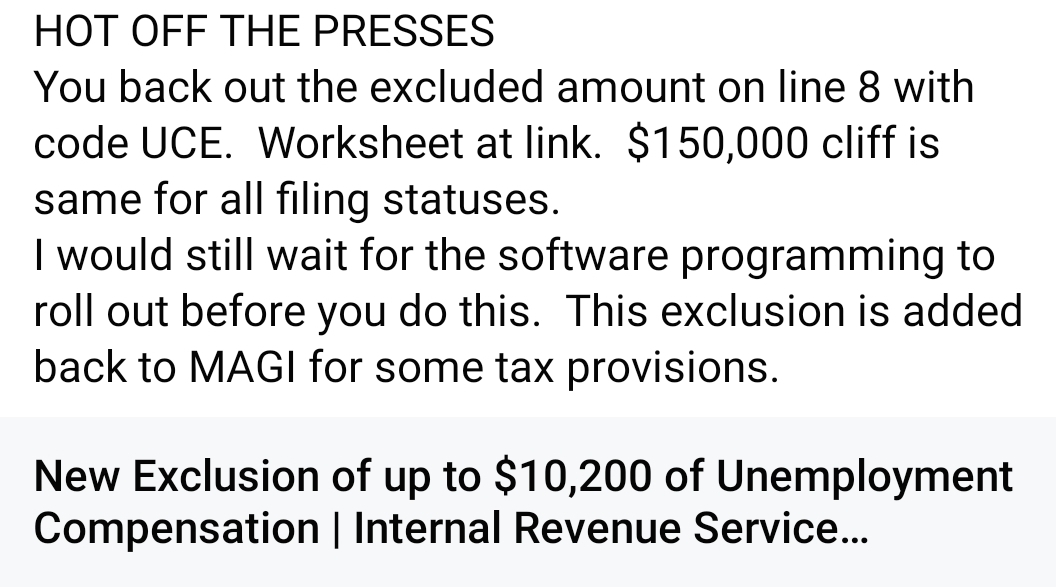

I haven't looked them up myself, but another forum said these calculations require the add-back: Taxable amount of social security Exclusion for US savings bond interest used for higher education Exclusion for employer-provided adoption assistance Limit on deductible IRA contributions by plan participants Limit on student loan interest deduction Limit on deduction for tuition and fees Limit on rental real estate exception to passive activity loss rules It might take a while for the software vendors to get all this right.3 points

-

New Exclusion of up to $10,200 of Unemployment Compensation More In Forms and Instructions If your modified adjusted gross income (AGI) is less than $150,000, the American Rescue Plan enacted on March 11, 2021, excludes from income up to $10,200 of unemployment compensation paid in 2020, which means you don’t have to pay tax on unemployment compensation of up to $10,200. If you are married, each spouse receiving unemployment compensation doesn’t have to pay tax on unemployment compensation of up to $10,200. Amounts over $10,200 for each individual are still taxable. If your modified AGI is $150,000 or more, you can’t exclude any unemployment compensation. The exclusion should be reported separately from your unemployment compensation. See the updated instructions and the Unemployment Compensation Exclusion Worksheet to figure your exclusion and the amount to enter on Schedule 1, lines 7 and 8. The instructions for Schedule 1 (Form 1040), line 7, Unemployment Compensation, are updated to read as follows. Line 7 Unemployment Compensation You should receive a Form 1099-G showing in box 1 the total unemployment compensation paid to you in 2020. Report this amount on line 7. Caution. If the amount reported in box 1 of your Form(s) 1099-G is incorrect, report on line 7 only the actual amount of unemployment compensation paid to you in 2020. Note. If your modified adjusted income (AGI) is less than $150,000, the American Rescue Plan enacted on March 11, 2021 excludes from income up to $10,200 of unemployment compensation paid to you in 2020. For married taxpayers, you and your spouse can each exclude up to $10,200 of unemployment compensation. For example, if you were paid $20,000 of unemployment compensation and your spouse was paid $5,000, report $25,000 on line 7 and report $15,200 on line 8 as a negative amount (in parentheses). The $15,200 excluded from income is $10,200 for you and all of the $5,000 paid to your spouse. If your modified AGI is $150,000 or more, you can’t exclude any unemployment compensation. Use the Unemployment Compensation Exclusion Worksheet to figure your modified AGI and the amount you can exclude. If you made contributions to a governmental unemployment compensation program or to a governmental paid family leave program and you aren't itemizing deductions, reduce the amount you report on line 7 by those contributions. If you are itemizing deductions, see the instructions on Form 1099-G. Caution. Your state may issue separate Forms 1099-G for unemployment compensation received from the state and the additional $600 a week federal unemployment compensation related to coronavirus relief. Include all unemployment compensation received on line 7. If you received an overpayment of unemployment compensation in 2020 and you repaid any of it in 2020, subtract the amount you repaid from the total amount you received. Enter the result on line 7. Also enter “Repaid” and the amount you repaid on the dotted line next to line 7. If, in 2020, you repaid more than $3,000 of unemployment compensation that you included in gross income in an earlier year, see Repayments in Pub. 525 for details on how to report the payment. Tip. If you received unemployment compensation in 2020, your state may issue an electronic Form 1099-G instead of it being mailed to you. Check your state's unemployment compensation website for more information. Unemployment Compensation Exclusion Worksheet – Schedule 1, Line 8 Enter the total of lines 1 through 7 of Form 1040 and Schedule 1, lines 1 through 7. Include the full amount of unemployment compensation you received in 2020 on Schedule 1, line 7. Use the line 8 instructions to determine the amount to include on Schedule 1, line 8 and enter here. Do not reduce this amount by the amount of unemployment compensation you may be able to exclude. Add lines 1 and 2. Enter the total of line 10b of Form 1040 and Schedule 1, lines 10 through 21. Subtract line 4 from line 3. This is your modified adjusted gross income. Is the amount on line 5 $150,000 or more? [ ]Yes. Stop You can’t exclude any of your employment compensation [ ]No. Go to line 7 Enter the amount of unemployment compensation paid to you in 2020. Don’t enter more than $10,200 If married filing jointly, enter the amount of unemployment compensation paid to your spouse in 2020. Don’t enter more than $10,200 Add lines 7 and 8 and enter the amount here. This is the amount of unemployment compensation excluded from your income. Subtract line 9 from line 2 and enter the amount on Schedule 1, line 8. If the result is less than zero, enter it in parentheses. On the dotted line next to Schedule 1, line 8, enter “UCE” and show the amount of unemployment compensation exclusion in parentheses on the dotted line. Complete the rest of Schedule 1 and Form 1040, 1040-SR, or 1040-NR. Page Last Reviewed or Updated: 12-Mar-20213 points

-

"The IRS strongly urges taxpayers not to file amended returns related to the new legislative provisions or take other unnecessary steps at this time. The IRS will provide taxpayers with additional guidance on those provisions that could affect their 2020 tax return, including the retroactive provision that makes the first $10,200 of 2020 unemployment benefits nontaxable. For those who haven't filed yet, the IRS will provide a worksheet for paper filers and work with software industry to update current tax software so that taxpayers can determine how to report their unemployment income on their 2020 tax return. For those who received unemployment benefits last year and have already filed their 2020 tax return, the IRS emphasizes they should not file an amended return at this time, until the IRS issues additional guidance." …2 points

-

If this is in an IRA account, and has a loss, do you even need to enter it?2 points

-

https://www.irs.gov/faqs/irs-procedures/forms-publications/new-exclusion-of-up-to-10200-of-unemployment-compensation?fbclid=IwAR2PO_Zfyso02H3SQA6JTAgwkLTUU-Zmv26YdgxtbYg9UcOZNQoLnXkfWWM2 points

-

Not sure of the validity of this. I saw it on the ATX Facebook page and figured I'd post here as an FYI:

1 point

1 point -

For matching proposes, you should get the W-2Gs from your client. Not everything on the casino report has a W-2G. So it is on the best interest of the tax payer to list them. By the way, start a new topic vs hijacking someone else's post with different topics.1 point

-

CT is one of them. CT-NATP is writing legislators for urgent guidance, sooner rather than later. Here's a letter I cut & paste (with typos) that you can use however it works for your state. I'm off to get vaccination #2 and really hoping for no side effects, because I have an S-corp to complete plus two more on extension but need to calculate the CT payments they need to make. I felt it prudent to let you know what my firm has written to our State Reps about the unemployment. Why not write to yours and as for guidance. Feel free to cut and paste. Thank you Robert Hartmann, CT NATP Secretary for the letter: "Dear Rep., Last night the IRS released more details on how to report the new exclusion of up to $10,200 (per spouse) of Unemployment Compensation. We have been recommending to our clients who have received unemployment that they wait to file. We are not ethically thrilled about the prospect of having to file amended returns for a fee to cover our costs, if not time, later in order that taxpayers might receive a portion of their refund now. We have been in touch with DRS about this matter but they have had nothing to report thus far. Can you tell us if there is any consideration in the House for CT to exclude unemployment compensation from income tax? I’m happy to talk with you about this, especially if we are able to offer input. We are in the office constantly these days if you would like to call." Click below to find your State Representative and their contact details: https://www2.cbia.com/ga/CT_State_Representatives/-AZHOUSE1 point

-

Yes....it would....and it would break them. I for one would like to see it happen. Tom Modesto, CA1 point

-

Actually, the part of your Rule 3 I changed to red has to be added to Rule 1 and Rule 2 also. Or to put it another way, taxpayers of any age qualify for the refundable credit if they have no living parents, or file a joint return.1 point

-

Form 8915-E1 point

-

In fact, you get three bites at the apple (if you haven't yet filed for 2020). "As rapidly as possible," the IRS will send payments to those who qualify based on the 2019 return (if 2020 not yet filed). Later this year, the IRS will send payments based on the 2020 return (if 2020 filed by then) - you will get the difference if you were paid in the first round and are now eligible for more. Next year, you can claim RRC based on your 2021 income if eligible for more then. So, wait to file if you qualify for more based on 2019 return.1 point

-

Enter the 1099-R the way it is written, then scroll down and select Corona... on another post I entered the correct line...that will invoke form 8915-E. The form will be showing the amount from form 1099-R and all you have to do is to enter the date to the left of the amount. That will do 1/3 for 3 years. If the client wants to put back some money to the 401k before filing, you enter that amount on the correct line. See other posting by searching for 8915-E1 point

-

https://www.law.cornell.edu/uscode/text/26/6428 (2) Joint returns In the case of a refund or credit made or allowed under subsection (f) with respect to a joint return, half of such refund or credit shall be treated as having been made or allowed to each individual filing such return. Which is also what the 1040 instructions for line 30 say: Married filing jointly. • If your EIP 1 or EIP 2 was based on a joint return, you and your spouse are each treated as having received half the payment that was issued. Legal disclaimer: The date at the bottom of Cornell's page is 3/27/20 and the instructions were probably written 3 months ago, so none of the above may be currently accurate. If you wait another two days, the answer may differ.1 point

-

Grouping does not work for 1099-R forms. I don't know if the IRS system will be looking to match each W-2G for dollar amounts or not. Charge per entry. "This is the extra cost of winning."1 point