Leaderboard

Popular Content

Showing content with the highest reputation on 08/17/2018 in Posts

-

We are under no legal obligation to continue providing tax return services in future years. If you don't want to prepare a tax return next year, don't send them a organizer, don't send them a appointment and do not accept an appointment if they call. Yes, it is polite to send them a letter saying to "get lost". But really, email, USPS, Priority, Certified or even smoke signals.... It is a courtesy you are extending to them. They do not contact US to tell US that they won't be back, right? (Well, except to get free copies of prior years returns so they can give them to the new person...) The letter I would send, would state that next years fee is going to last years fee plus an increase of 1.xx more. They can make a decision after that. Rich5 points

-

I usually just fire them by billing them much more than usual. Consider it a parting gift.4 points

-

On another forum, the standard advice was to double their bill every year until they left or you were happy. One guy wrote back, saying he'd inherited a "problem client" (acctg and tax) who drove him NUTS always calling with questions. Annual fee was $1250. So he double it to $2500. Still drove him nuts. Doubled again to $5,000 and they were still annoying. Doubled it yet *again* to $10,000 - and now they're some of his favorite clients, with whom he is always happy to chat! The fee just wasn't commensurate with what they needed and wanted. How many times do we put up with stuff we should be charging for, and resent it, when clients might be happy to pay more? (Or walk away, with us waving energetically behind them to hurry them along.) Make sure the ones you are firing are really PITA's that you don't want at any price. Else try hiking the price to the level they annoy you, and see. One guy said some years ago that if you double your price and lose half the clients, you're making the same money for half the work.3 points

-

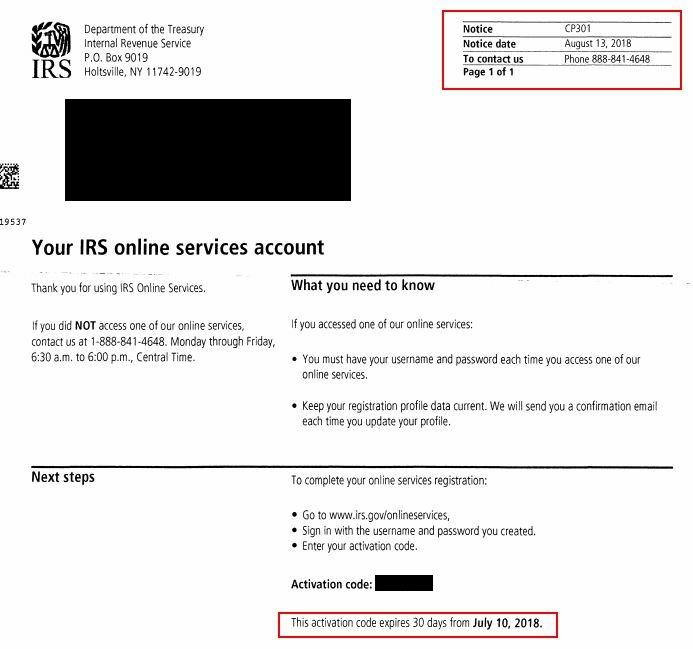

I requested my code on July 10. Notice the date of the IRS letter and the expiration date at the bottom.

3 points

3 points -

A reply from them may not be necessary as proof of receipt of email. Some email functions through ISPs or apps have the option to receive an acknowledgement that the recipient received and read the email. I still prefer an actual letter sent by snail mail better for termination letters and other official correspondence though.3 points

-

Start with email. Their reply gives you proof for your records that they received the message. If they don't reply, escalate to Certified Mail with Return Receipt.3 points

-

I have fired clients using plain ole USPS. They all got the message, although a couple begged me to keep them on until they got through some complex situations (end of a trust, etc. and one who just couldn't bear to go anywhere else). I did, but at least I got rid of most of the "high risk" and PIAs.3 points

-

You know, that is an excellent point Catherine. I have been thinking that I want to sell my business and get out so I can work less hard. Maybe if I don't have much luck selling, I should just keep raising my fees until I am working less hard because people leave but I will still be making money on the ones that stay. Something to think about before the first of the year......2 points

-

QuickAlerts for Tax Professionals August 17, 2018 e-file Resources QuickAlerts Library QuickAlerts Article QuickAlerts Brochure e-file for Tax Pros MeF Software Developers IRS.gov Refund Information Other Useful Links Tax Professionals Home Forms and Instructions Stakeholders Partners' Headliners Training and Communication Tools IMRS e-Services Disaster Relief Internal Revenue Bulletins Subject: CP-301B notices for Secure Access Registration Some CP-301B notices for Secure Access Registration, issued between August 8 – 15, 2018, were issued with an expired Activation Code. The IRS will update the Activation Code expiration date to September 30, 2018, on Tuesday, August 21, 2018. If you received one of these notices please complete your online Secure Access registration between August 21, 2018 – September 30, 2018. We apologize for any inconvenience this has caused. Back to Top Thank you for subscribing to QuickAlerts for Tax Professionals, an IRS e-mail service. If you know someone who might want to subscribe to this mailing list, please forward this message to them so they can subscribe. This message was distributed automatically. Please Do Not Reply To This Message. Update your subscriptions, modify your password or email address, or stop subscriptions at any time on your Subscriber Preferences Page. You will need to use your email address to log in. If you have questions or problems with the subscription service, please contact subscriberhelp.govdelivery.com. This service is provided to you at no charge by the Internal Revenue Service (IRS). This email was sent to [email protected] by: Internal Revenue Service (IRS) · Internal Revenue Service · 1111 Constitution Ave. N.W. · Washington DC 205352 points

-

Years ago, while in the Coast Guard, in November, the ship I was Communications Officer of received a 6 month supply of a brand new form for a monthly report to headquarters. In April the following year I ordered a replacement supply of the forms. The reply from headquarters was "In November we sent you a six months supply of this new form. Why are you ordering more in April?" (In essence: 6 months ago we sent you a 6 month supply. Why do you want more?) I realize that someone never read what they sent as a reply. Joel2 points

-

Your government at play! *What* a pack of idiots. Sigh.2 points

-

I guess the programmers never allowed for the possibility that the codes could expire before the letter was mailed, and to just generate a new code to be mailed. The lady told me they had a glitch that delayed the letters and that they're normally mailed in about 5 days.1 point

-

That's OUR tax dollars!1 point

-

Even though the trust was not closed out, the property was transferred out of the trust so the income and expenses go to the beni's per the assignment of income doctrine.1 point

-

Mostly agree with you Judy but the expenses paid after transfer would not be treated as distribution if paid from rent that was received after transfer. In this situation, the trust collected rent and paid expenses on behalf of beni's. So anything paid out of rent earned by beneficiary's would not really be a distribution from the trust assets. Also I question whether 1099 from trust is appropriate. I would advise trustee to furnish beni's with a statement showing their share of rent and expenses including mortgage interest that flowed through the trust bank account. Also provide beni's with information on their share of basis on date of transfer per treas. reg 1.1014-4 (Uniformity of basis).1 point

-

https://kb.drakesoftware.com/Site/Browse/11648/Form-1120H1 point

-

Judy, thank you very much for your detailed analysis and am very appreciative of the time put into it. I am certainly leaning in going in that direction as most of it coincides with what I was thinking.1 point

-

And make sure to take them OFF the list for new season client organizers!1 point

-

The personal representative might be able to get a transcript online, if not, paper file the 4506T-EZ and attach court appointment letter.1 point