Leaderboard

Popular Content

Showing content with the highest reputation on 09/26/2023 in all areas

-

I consider SS out of my bailiwick. Sure, I'll advise clients on how benefits will affect their tax situation, but that's where I draw the line. When to collect, on whose record, etc. are complex and I don't want to be responsible for giving advice that may end up not being in the client's best interest. Same goes when clients ask us legal or investment questions. Go ask an expert in those fields. Of course they ask us because they don't think they'll have to pay us extra. We had a client who called with a legal predicament and when we recommended he go to his lawyer, he admitted that the lawyer charges too much. Stay in your lane.5 points

-

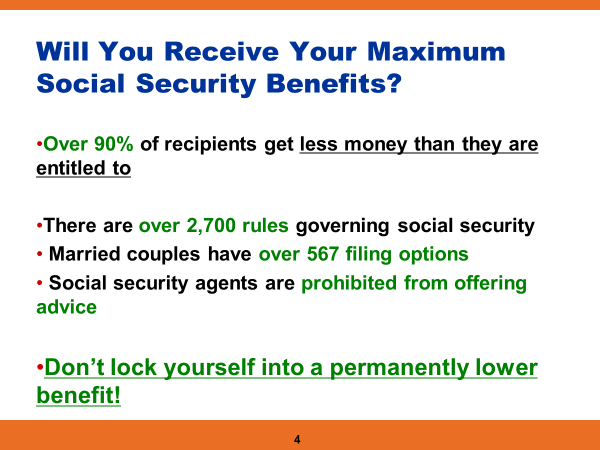

He may be great, but I personally don't put much stock in people using scare tactics to drum up business. "Over 90% of recipients get less money than they are entitled to." LOL! Took me less than a minute to google that 10% wait until age 70. Are 90% of people wrong by starting benefits before 70? Nope. Like I said, it's about maximizing wealth, not SS benefits. Do I think the gov't can handle my money better than me? Again, nope. None of us knows when we will die nor do we know what Congress will do when the Trust Fund is depleted. It's estimated that around 70% of benefits could be paid by current tax inflows. I wouldn't be all that surprised if high income/high retirement account people have their benefits reduced in the future. Just like defer, defer, defer mantra for retirement accounts isn't always the correct answer, neither is deferring SS as long as possible the correct answer for a lot of people. I am curious about a couple of things. Does he have a list of the 567 filing options? And how much does he charge to advise on SS benefits?2 points

-

That and the thousands of employees shifted to answering the phones .2 points

-

Wow! Nothing wrong with us increasing knowledge on issues such as how SS works. Many times I've been able to inform clients on items they aren't aware of. Of course I always say "this is my understanding" and encourage them to contact SS for verification. If preparers don't want to get involved in such issues as SS, that's fine. On the flip, if preparers want to educate themselves and share the knowledge with clients, that is also fine. To each their own. My "lane" is trying to help clients that aren't well versed on various financial matter to the best of my ability.2 points

-

Be careful, there is a lot of misinformation out there. Most clients have preconceived notions which aren't always accurate. Also, certain situations can be significantly more complicated than you might expect. Because of these minefields I don't give specific advice, I speak about issues to be considered. Clients wanting specific advice probably should be referred to Certified Financial Planners.2 points

-

Christian, if I remember correctly being a half time student is not enough to claim dependency - the student must have been a full time student for at least some part of 5 months of the year. Not getting the degree would be irrelevant - you don't have to be a successful student, just a student.2 points

-

I have found an excellent IT support person who works remotely and is customizing a WISP plan for me, along with ongoing IT support. If anyone here is interested in talking to him, send me a message and I'll pass along his contact information.1 point

-

Remember when the IRS said they were moving employees to opening the mail in a timely manner? Now we know where they came from! Of course, some other function will suffer.1 point

-

Send your clients to an SS benefits expert. Here's just 1 of Ash's slides from his presentation to the NY/CT-ATP June 2018:

1 point

1 point -

There is not always a good answer. Situations may be different. For example, someday, our daughter will need to transition from SSI to SSDI, based on my earnings. This change is not always automatic, and must be initiated. If one does understand this can be done, and why, one may make less than optimal decisions before then, such as claiming before FRA.1 point

-

Seems to me to be anomalous--the IRS records are "reasonably complete" by August. But I recheck all of my clients (who've given me authority) in October to make sure something hasn't popped up. You cannot be absolutely certain until Jan 01 of the following year. BTW, if you see Code 922 on a transcript, it means they are going to get a CP2000 within 5 months.1 point

-

All this stems from my annual client reviews which I do in an attempt to make certain all is according to Hoyle.1 point

-

Ash Ahluwalia https://www.oneteamfinancial.com/1 point

-

From Accounting Today (https://www.accountingtoday.com/opinion/tax-strategy-irs-expands-focus-on-digital-asset-reporting?utm_source=newsletter&utm_medium=email&utm_campaign=V3_ACT_Daily_2023%2B'-'%2B09252023&bt_ee=7jXmSOk9k89v2KKJINwG%2BptBxryLwmkr26gmdBbyuzYmd2vNQetW91Wy8I1QODYQ&bt_ts=1695643801434) "It appears that there will be a new broker reporting form, Form 1099-DA, to address the reporting of digital assets. For every digital asset sale, the broker is required to report the following: 1. Name, address and TIN of the customer; 2. Name or type and number of units of digital assets sold; 3. Time and date of sale; 4. Gross proceeds of sale; 5. Transaction identification number; 6. Address from which digital assets were transferred; 7. The type of consideration received, such as cash, other digital assets, other property or services; and, 8. Any additional information required by forms or instructions. Regs with respect to the computation of gain or loss and the basis of digital assets are proposed to apply to tax years after the finalization of the proposed regulations. The proposed rules with respect to broker reporting of gross proceeds apply if the sale is on or after Jan. 1, 2025. The proposed rules on broker reporting of adjusted basis apply if the sale or exchange is effected on or after Jan. 1, 2026. The information required to be reported may relate back to Jan. 1, 2023." Thankfully, most of my clients are older and want nothing to do with digital assets. Last year I only had one that did anything with cryptocurrency.1 point

-

She can be a dependent qualifying as a full time student until she turns 24, provided the rest of the dependency requirements are met. The mom can get AOC for 4 years if daughter is he dependent. LLC is available for any years in which AOC is not claimed. Tom Longview, CA1 point