Leaderboard

Popular Content

Showing content with the highest reputation on 09/28/2023 in all areas

-

https://www.irs.gov/charities-non-profits/charitable-organizations/charitable-contributions-quid-pro-quo-contributions https://www.nolo.com/legal-update/irs-changes-thank-you-gift-rules-35445.html6 points

-

You would have to determine what the motivational speaker usually charges the general public to attend one of his presentations. If the speaker does not normally charge for his presentations, then no value would have to be included. I believe the DJ and photo booth have a insubstantial value, and do not have to be included. The attendee's didn't receive any tangible benefit, good, or service and would probably would have attended even if the DJ and and photo booth were not included. I would make sure I documented the information that was used to make the "good faith estimate" of the FMV of the goods or services received.4 points

-

Yesterday, I checked the client that had zero entries on their Income transcript and everything showed up, all twelve pages.3 points

-

Can they file a late 8832 to claim the Corp status and then make a late S election? Normally an automatic approval from the IRS from what I understand. And since the IRS does not have a 1065 on file, since this is the first year filing, they should be good to go if the 8832 is included with the 1120S. Just a thought. Tom Longview, TX1 point

-

Depends on how the questions were answered. They could have just gotten an EIN for banking purposes, but yes, if they answered the questions correctly, it would default to a 1065. Now I'm wondering if an extension was filed. Even then, the 1065 would be late, but it's an automatic penalty removal, even without first time forgiveness.1 point

-

If they obtained an EIN, won't the IRS be expecting a Form 1065?1 point

-

This is why I almost never support fundraising events. I'd rather just donate cash.1 point

-

Sometimes failure reinforces the process of learning lessons. This happened several times with my clients before you could efile amendments.1 point

-

I take a LOT of courses that do NOT earn me CEs to retain my EA. I take classes on CT, NY, MA, PA, CA, and other states, and also technology, and classes from instructors/topics I like that might give CPE but not CE. My NY/CT-ATP group includes an hour of NY tax updates and an hour of CT tax updates each year and two hours of non-federal tax law classes (we've done SS, Medicare, retirement planning, multi-state issues, financial aid/paying for college, and office security years before the IRS approved it for CEs).1 point

-

Kathy, of course there's nothing wrong with educating yourself, but I draw the line at sharing my certainly incomplete knowledge with someone who will use it for a life-changing decision. People should get solid advice from SSA (the folks there are really good in my experience) or work with a financial advisor--NOT their tax preparer. Over my career I have had several people question me about the tax implications of getting married. Really? I would think that people decide to marry because of love, commitment, to make a relationship permanent. Money might enter into a decision to do a prenup, but to get married? Talk to a marriage counselor, not your tax preparer.1 point

-

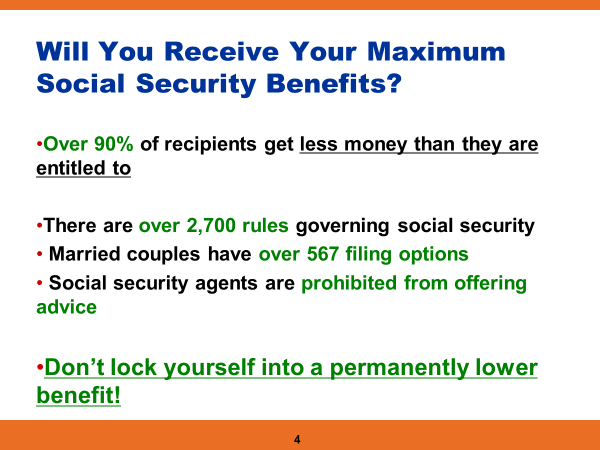

He may be great, but I personally don't put much stock in people using scare tactics to drum up business. "Over 90% of recipients get less money than they are entitled to." LOL! Took me less than a minute to google that 10% wait until age 70. Are 90% of people wrong by starting benefits before 70? Nope. Like I said, it's about maximizing wealth, not SS benefits. Do I think the gov't can handle my money better than me? Again, nope. None of us knows when we will die nor do we know what Congress will do when the Trust Fund is depleted. It's estimated that around 70% of benefits could be paid by current tax inflows. I wouldn't be all that surprised if high income/high retirement account people have their benefits reduced in the future. Just like defer, defer, defer mantra for retirement accounts isn't always the correct answer, neither is deferring SS as long as possible the correct answer for a lot of people. I am curious about a couple of things. Does he have a list of the 567 filing options? And how much does he charge to advise on SS benefits?1 point

-

The goal should not be maximizing SS benefits, but rather maximizing wealth. Simple scenario: Benefits at age 67 are 25K. I'm assuming a 2.5% annual COLA. Waiting until age 70 and the combo of 8% a year bump and COLA and first year benefits are 33,914. If the person lives past age 80, they will receive more in benefits by not claiming until 70. If they die before 80 they will have received less benefits. By age 90, the projected benefit total is 809K for starting at 67 and 922K by starting at age 70. Looking only at the benefits, it looks like it's better to delay, correct? Instead, how about starting at 67 and investing the benefits for the first 3 years? I used 80% of benefits at account for any tax on amount to invest and used an annual return rate of 7%. Compounding the returns and the amount in this account is 272K at age 90. The non invested SS benefit amount is 732K, for a total of 1,004K. In this case, you end up with 82K more, plus the 272K can be passed on to heirs. Now, which one sound better?1 point

-

Send your clients to an SS benefits expert. Here's just 1 of Ash's slides from his presentation to the NY/CT-ATP June 2018:

1 point

1 point -

I always deferred most SocSec questions by recommending that the client go straight to SSA for answers. After I began drawing SocSec 7 years ago and navigated my own situation, I changed my policy. I now defer ALL SocSec questions by recommending that the client go straight to SSA.1 point

-

I consider SS out of my bailiwick. Sure, I'll advise clients on how benefits will affect their tax situation, but that's where I draw the line. When to collect, on whose record, etc. are complex and I don't want to be responsible for giving advice that may end up not being in the client's best interest. Same goes when clients ask us legal or investment questions. Go ask an expert in those fields. Of course they ask us because they don't think they'll have to pay us extra. We had a client who called with a legal predicament and when we recommended he go to his lawyer, he admitted that the lawyer charges too much. Stay in your lane.1 point