jklcpa

-

Posts

7,165 -

Joined

-

Days Won

406

Everything posted by jklcpa

-

Yes, it has been like that almost since the beginning of this season for me. When the program would open, I had no alerts or notifications in that bottom left corner of the manager screen, and I wasn't able to get program updates. I didn't realize this at first because I was only waiting for state approval of a certain form. Also, MS Edge browser window would open on top of the program every time, and I couldn't make the support person or her supervisor understand this. I have never used Edge, and the supervisor's suggestion was for me to try changing to Edge as my default browser, or try Chrome. I could NOT make either of them understand at all that something with my computer's environment was blocking communication from the program to Drake's server, that it was not a browser issue. Finally after about 6 calls the supervisor sent a message to a higher level support person. Very frustrating! We worked on it and thought it was solved with me changing settings in my AV, but the problem reappeared again in late Feb. I ended up changing to a different AV software completely but had only disabled the original one. That worked until I rebooted the computer and a portion related to the original AV's VPN was still enabled, and THAT was the issue.

-

I haven't had anything from Drake yet. Tax Book's offer came in the mail today.

-

He's a cute little fluffball.

-

Yes, please see the instructions to preparing 1099-C and "Who Must File" and the large bold heading under that labeled "Exceptions". It seems that the form's issuance depends on the type of bankruptcy and whether the debt was for business or investment, or if it was for personal use.

-

Thanks. That's good to know, and so it would be up to Christian to find out the specifics for this student.

-

Christian, you may be correct. With the AOC, the student must be a degree candidate, and he can't be a candidate for a degree without graduating from HS. Most colleges and universities will not even enroll the student in the degree program without first completing the secondary education. The LLC, on the other hand, can be taken by an eligible student taking course(s) that are part of a degree program, but it does not require that the student be a degree candidate.

-

Student has to be a degree candidate, and since he hasn't graduated high school yet that would knock him out. No? Even if qualifying, AOC can only be claimed for 4 years. Maybe the parents don't want to claim in a year where the credit would be small.

-

The incomparable thrill of meeting the deadline. Almost 2 a.m. and 4 coffee cups, that would have been about right in many past years for me.

-

I'm done and done in. Last night I dug a hole on the edge of my foot to remove an already inflamed deepish splinter and went off this morning to the 5K charity event with a bunion pad and bandage. I completed only half of that, and then the sporting clays went about the same, like I was a raw beginner again. I had an awful season this year. My Mom passed at the end of Feb, and the I got the flu-a in early to mid March and missed many days. I actually sent 3 returns and a trust away because of it. There were a few days that I don't even remember in March when I started back working and was still very sick. Glad this season is over. If you made it this far, thanks for listening to me whining.

- 32 replies

-

- 14

-

-

-

-

Yes, absolutely we want you to stay with us.

-

Have you included the nonresident/part-year ratio schedule in the return? That ratio from the schedule would be applied to the overall MT tax on all income so that the tax is reduced to the same ratio that the MT income represents of the total income.

-

Certain people do come to mind and then they turn to dust. Breaking things after an aggravating day can be very satisfying.

- 32 replies

-

- 10

-

-

-

There is a fillable version available from irs.gov here: https://www.irs.gov/pub/irs-pdf/f8978.pdf and the instructions: https://www.irs.gov/instructions/i8978 Good luck!

-

I have no experience with this and don't use ATX but googled and found that ATX does not list this form as part of the ATX packages. https://support.atxinc.com/taxna/software-system-requirements/atx-forms

-

I'm done. This morning I filed the extension for my ultimate procratinator, and other than the extended returns, I am waiting on one to pickup (SO unexpectedly hospitalized day she was scheduled to see me) and one couple that have had the returns for almost a week and must return the 8879 to me. Tomorow I am participating in a charity event in the early morning and then will be shooting at the clay pigeons. That's been ongoing as weather permitted and really helped keep my sanity this year. Plus, it's fun.

-

TexTaxToo's quote is directly from the 1310's instructions. I don't know why this is so hard either. If Yardley's client (the son) has a Short Certificate, which if in his state would be the only official legal appointment LIKE IS HERE IN DE, then the form 1310 is NOT REQUIRED.

-

Yes, this is correct. It depends on how long the investment has been held.

-

That's what I do too, but it is so frustrating. This is a large return in terms of the number of bank, brokerage, and retirement accounts and pensions this couple has.

-

"Court appointed" is why I said to attach a pdf of the Short Certificate that the son has already obtained. Here, the Register of Wills is THE agency with the authority and issues the Short Certificate because our county Register of Wills is a branch of the Court of Chancery and definitely has the legal authority to issue that document showing the official legal appointment of the named executor to act on behalf of the estate. Maybe it works differently where you live, but an executor here with a Short Certificate in hand has all he or she needs and could definitely file without the 1310.

-

It's more likely that this is some sort of stipend that isn't taxable as federal wages but had the SS & Medicare withheld. As others said, either ignore the w-2 completely or enter $1 as federal taxable wages. Personally I'd ignore it if there isn't anything in any other boxes that needs reporting. Nothing on the that W-2 that affects any state return?

-

In general, for any filer whose SSN is used on the return and has an IP PIN, that IP PIN must be entered on the return or the return will be rejected. Even a paper-filed return will require the entry, or without it the IRS will need to verify the identity through other methods and will slow down its processing. Is it possible that the spouse opted to retrieve the IP PIN electronically and a paper notice wasn't mailed? This sounds like a case where a call to the IRS # for special situations is needed to answer the question.

-

No. It is different for a corporation and not at all the same as how a partner handles UPE. Corporation would need to set up an accountable plan and reimburse the shareholder. An example of where this is used is personal auto used for business purpose, shareholder keeps mileage log and submits a report to the corp for reimbursement. Corp reimburses at the allowed federal rate. There are other accountable plans that have more specific tax law rules such as medical reimbursement plans or when to reimburse shareholder paid disability insurance premiums. If there is carelessness or intentional comingling of expenses paid from the corp accounts, you may want to have a discussion with your client about not using the corp's checkbook as his/her own.

-

My client is sharp too, just the ultimate procrastinator. His type of treatments won't cause any brain fog, but just one more thing in his day that's taking up time. I know about the cancer issues with my husband having had 3 types, 4 if we count minor skin cancer too. Throat, prostate, and TCC aggressive bladder cancer.

-

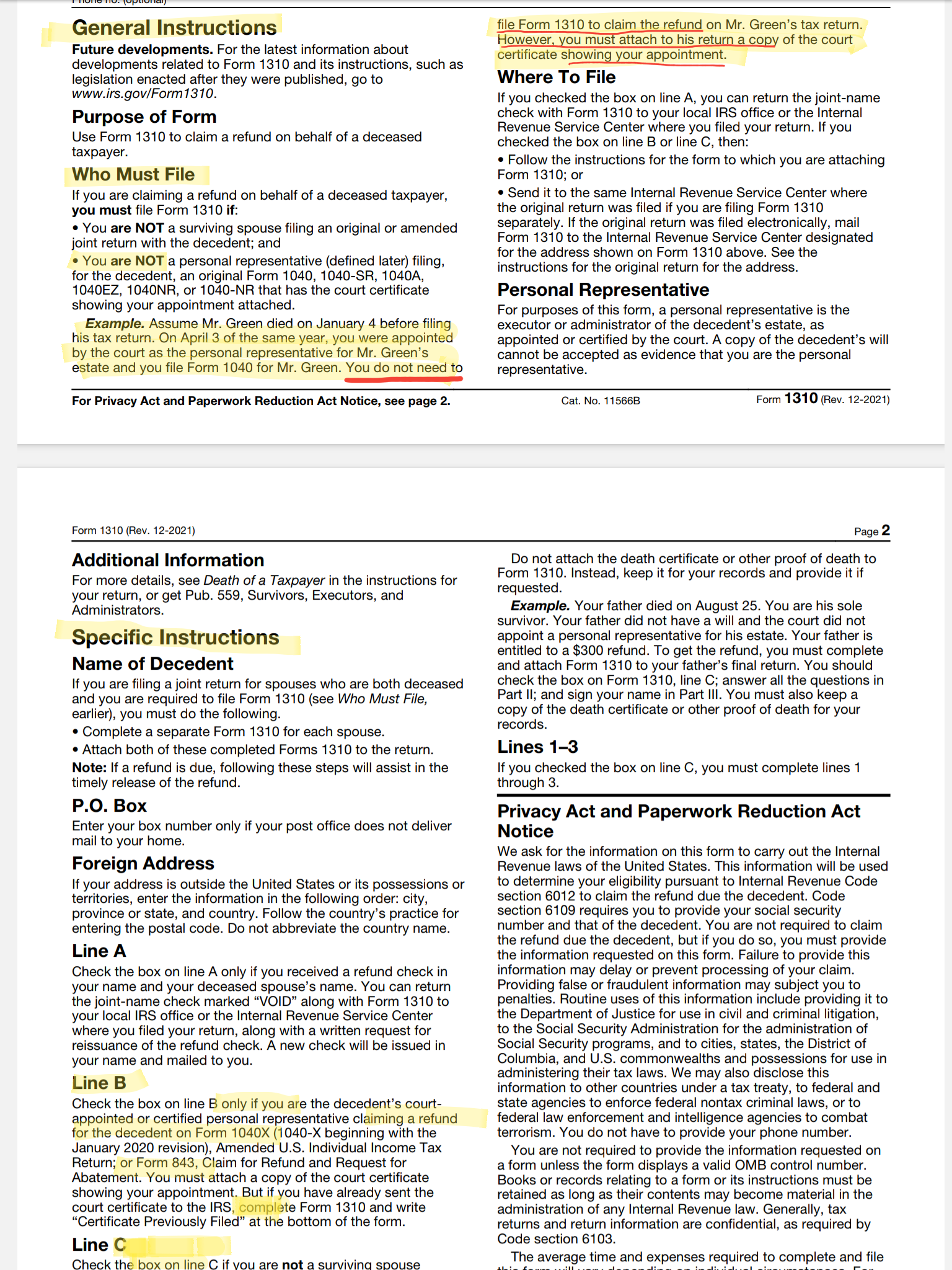

You don't need form 1310. You can definitely request an extension by e-file. You should also be able to scan and attach the short certificate to the return itself and e-file that too. See below. For purposes of form 1310, executor is considered the "personal representative," so this return doesn't need the 1310. See below. Be sure to enter the name of the executor in the "c/o" name box in your input and change the address to that of the executor. This is what will be on the 1040. If you look at the instructions for "Who Must File" you don't need the form 1310 because son IS the personal representative of the estate, and for purpose of this form, the executor is considered the "personal representative". You should be able to scan the short certificate and attach that as a pdf for the return and e-file it. Please see the example as shown in the instructions to the 1310 below:

-

For me, this site is a place to learn, get answers, vent or commiserate, or just take a break during the day. It continues to be an invaluable resource that's been a part of my daily routine for 17 years. Eric has taken care of us from the site's inception, mostly unseen, and his work is ongoing. Soon he will migrate the forum to a new host and is waiting for us to get through the 15th before doing so. I've made a donation today and hope others here will consider that as well.

- 2 replies

-

- 10

-

-