jklcpa

-

Posts

7,163 -

Joined

-

Days Won

406

Everything posted by jklcpa

-

You already received the best answer is to have client use IRS' Direct Pay. About the above statement, don't ever assume that a bank or credit union offers overdraft protection or that the account is of the type that even has that set up.

-

@Pacun and everyone, I fixed the link so that it now goes to the official IRS page for direct pay.

-

Attorney should get 1099. IN GENERAL, the part for services provided to your client should be on NEC box 1. The settlement portion should be on the MISC, box 10. The amount to include will depend on how the check was made out. My basic understanding is that if the check was paid to only one attorney, then obviously that attorney gets the 1099 for full amount. If one check is paid to co-payees, I think they each get a 1099 for the full amount. If attorney gets money and part is for co-counsel, then attorney gets 1099 with full amount, and they issue a 1099 for amount they paid co-counsel, but again, that depends on who check is made payable to. There is also the issue on what type of settlement the payment is for. Example, as the article below explains, payments for personal injuries don't require 1099s to the injured party but will be issued to the attorney, depending on how the check is made out. I'd suggest start your reading with the article below from the ABA that is written in more layman's language and is informative before going to the 1099 instructions for preparation, and then the code . The 1099 instructions do reference the applicable code sections. Also, perhaps a separate post would be better for what portions of these payments are deductible by your client. Slippery Pencil is correct that attorneys are an exception to the corporate rule. They get 1099s regardless. Anyway, here is the ABA article to start with: https://www.americanbar.org/groups/business_law/resources/business-law-today/2020-february/irs-form-1099-rules-for-settlements-and-legal-fees/

-

Ask more questions. Every day rented at below market rate is considered personal use, and this may not be a rental at all as far as deductions are concerned. If that is the case, the income becomes ordinary income, deductions evaporate except for those that would be allowed on Sch A.

-

Is this client using a management/rental agent? If so, those companies usually have a report that shows the actual days rented and the days it was owner occupied. If you can get that, you may be able to see if receipts for fixing up and repair costs match up to any of those dates after it was put in service. If there are no receipts for repair supplies but the report shows owner usage, then what exactly were they doing there? Even something as simple as painting requires materials, but if it is a nice enough property to be rented as a vacation spot that the owners choose to stay themselves, then what would be needed at that point other than routine cleaning or fixing something minor that was broken by a tenant? Are you sure that all of the $75K is furnishings that would allow the bonus depreciation? Is it available for rental this year, or is it already out of service? I also wonder about the $2,000 of income for 61 days of rental. That seems really low to me, but maybe it is your location compared to mine. What kind of property are we talking about here? Are these short-term rentals in a nice vacation area or a more rustic site like a cabin in the woods?

-

Now that the convo seems to have exhausted and concluded, I found this funny clip about those farm trucks. It is a Facebook clip, so I'm sorry that those of you not on that platform won't be able to see it. https://www.facebook.com/share/r/16AqLmzUXp/?mibextid=D5vuiz

-

I'm confused by this. How is it possible for the ATX program to allow the 4868 and the 1040 to be filed at the same time? Extensions I file are because I am missing data and the input has estimated amounts in it about 99% of the time. Will these returns require amending now?

-

Any body else having issues getting Ack's back from California?

jklcpa replied to Tax Prep by Deb's topic in E-File

If you haven't yet done so, I would go to Drake's support site, and under "Reports," print out the "E-file Detail Lookup Report ." That report is more detailed than what is available through the software. For Federal and each state return, it shows the time stamp, its e-file status, the e-file submission i.d., and the DCN. The submission i.d. is unique to each return, so CA's identifier will be different than the federal or any other states for the client. Because by Monday you will be beyond the 5 day correction period for rejected e-files, that report would prove that e-filing was done timely, because if you end up resubmitting the e-file for some reason, it is my understanding that a new e-file submission i.d. is generated and that may make it appear as if these returns were filed late. If you don't have acks by Monday, I also think you should escalate this to a higher level with Drake than with those that provide basic telephone support. There were other years where posts here indicated a delay of 2-3 days immediately after the deadline, but this seems too long to me. -

Any body else having issues getting Ack's back from California?

jklcpa replied to Tax Prep by Deb's topic in E-File

Are these returns on extension? The reason I ask is that my state doesn't accept e-filing of its extension, so when I send the 4868, I always click the box to suppress the state from being sent just in case. Then, I always have to remember to uncheck that box when I file the returns themselves. Any possibility something like that happened? Another thing, have you checked the e-file database for these 5 returns, either through the software or Drake's online site to make sure they were sent and for the timestamps? -

Sounds good, but I would suggest this substitution: After reflecting, I realize that I need to reduce my workload to a more manageable level.

-

When I read posts like some here in this topic and others, and I think back to the workload I endured in my earlier career, I worry about some of you and about us as a profession overall. I haven't made nearly the amount I could have for whatever talents I have, but I have made a concerted effort for a healthier work-life balance and am happier because of those choices. This work can be extremely rewarding, but I believe that it shouldn't be at the expense of our health and well-being. I wish you all well, hope that you recover quickly, and are able to enjoy some quality time away from the office. I also hope to see you here in the off-season as we continue to work at a less hectic pace.

- 14 replies

-

- 13

-

-

If someone did that to me, I wouldn't have wasted an hour and may have considered not continuing on with the client, all depending on the tone of the lecture and insistence. Probably not over rounding though. Twice in my career I had returns ready to file, took them back from the client and disassembled them, handed original source documents back, and showed the (former) client the door. However, it was people who had outright lied, insisted I file a certain way, and when I refused to file fraudulent returns, accused me of not knowing what I was doing! Fine, they could go find someone else!

-

You already have the answer for the federal superseded through ATX, but this topic came up earlier this season, and at that time when I checked, there were only three states (CA, UT, NY) that accept superseded individual returns. That means that if your client's state return(s) also requires correction and isn't one of those three states I listed, then you will have to create a separate file for the state amendment. It may be easier to process by amending both the federal and state at the same time.

-

Faulty AI and no human to error check and correct?

-

But if the actual method is used in the first year, then the client must continue to use that and can't ever switch to cents-per-mile method.

-

I'm waiting for it to go to a second page!

-

I may use that on a difficult meeting tomorrow!

-

What Abby said, plus if prior preparer changed software providers without conversion, the LTCL c/o entry may have been missed.

-

PA has its own sch K-1s for either resident or nonresident partners or shareholders. Do you have a PA NRK-1 ("NR" meaning nonresident)? The PA return should back out the federal information and pick up the activity reported on the state NRK-1. Hope this helps.

-

Without researching, I'd say that this isn't any sort of apportionable item or a corporate-level item that can be attributable to nexus in the client's nonresident state, but rather is a shareholder level gain based on individual's basis. There are a few states that tried to impose a tax on similar gains from partnerships (distribs in excess of outside basis) for partners (CA, ID, NJ, OR), but not KS as far as I know. I would treat this as taxable to the resident state. What is the nonresident state?

-

Sometimes clients hear what they want to hear. If other withholding or estimates were already sufficient for 2024 to meet the safe harbor, are you sure that the previous preparer didn't really say that if they didn't pay tax on the gain during 2024 that they wouldn't have the underpayment penalty? That could be the case here, a year later, especially when a client doesn't fully understand and aren't talking with the original messenger that can revisit the conversation and information or advice she discussed.

-

The Wikipedia link from my first post has links and references to the 2 immediate predecessors, one of which was RockTenn. RockTenn's wiki page has the company's history of a merger in 1973, so that is probably what your client's mother owned when she passed in 2001. RockTenn came from a merger of 2 other TN companies, one with history going back 125+ years in Nashville. Maybe some of the history on that page will help you figure out which company your client had to start with. Does the client's county register of wills have archives of estate filings that could be retrieved? IF the gain is substantial, it may be the most expedient method to get that information for a small fee rather than trying to recreate something you are unsure of or can't truly document.

-

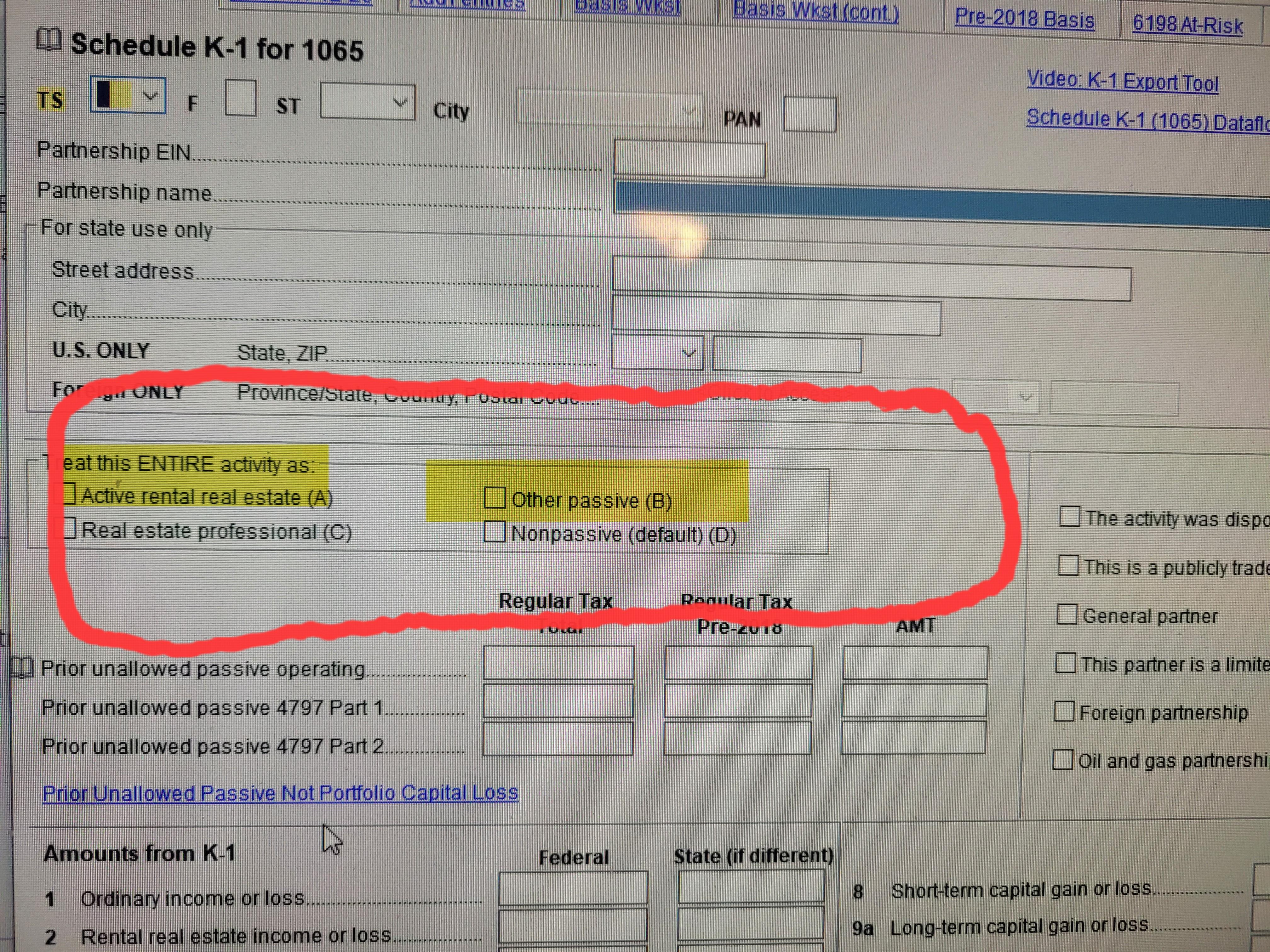

The box I am referring to has nothing to do with PTPs. You either have nothing checked in this section shown or have the default checked which is "D". Again, Drake is allowing the loss as nonpassive because no box is checked or is defaulting to "D" and is putting it in the nonpassive column on pg 2 of Sch E. IF you want the the loss to be subject to the PAL rules, you must check either box "A" or "B" that I have highlighted. Checking either of these will produce the form 8582, and 8582 worksheet, and possibly a PAL worksheet. If your client has active participation, check box "A" and the loss should carry to line 1b of the 8582 and will be disallowed for the current year, carried fwd to future, and current Sch E should have a -0- on it. Checking box "B" for passive activity will also produce the 8582 with the loss flowing to line 2b. Again, loss should be disallowed and carried fwd with the current Sch E having a -0-.

-

Looks like it was under another name and became Westrock through a merger. You may have to work backwards from the # of shares now to what was originally held before looking up the historical prices. Found this on Wikipedia that may help, if this is the company you need data for: https://en.wikipedia.org/wiki/WestRock

-

What is listed as the "type" of partner? Does it say "individual" or does it say "individual passive" or "passive"? Drake will put the loss in the nonpassive column and carry, allow it, and carry that loss to 1040 Sch 1 if you check "Nonpassive (default) box D" on the K-1 input screen. If you believe this is wrong and that the loss should be subject to the PAL rules, then you need to check box B for "other passive" on the K-1 input screen. I still don't think Drake has a programming error. It is doing what you are telling it.