Leaderboard

Popular Content

Showing content with the highest reputation on 01/23/2019 in Posts

-

Just a heads up on 2 important areas for the Qualified Business Income (QBI) deduction in new code section 199A. The IRS published final regs last week. The first is rental real estate. There was substantial debate over rental real estate, and whether it ros eto a "trade or business" eligible for the QBI deduction. Trade or business is still a facts-and-circumstances determination, but the IRS created a safe harbor that basically requires 250 hours of work a year on each set of rental real estate activities for it to qualify. The work may be performed by the owner or agent(s), but a log must be maintained for years starting in 2019. More info is at www.irs.gov/pub/irs-drop/n-19-07.pdf The second is a clarification for the self-employed that has caught some of us by surprise. Many professionals and most software packages used a starting point of net Schedule C income for QBI. The IRS clarified that the QBI deduction is done after the deductions for SE health insurance, SE DC pensions, and 1/2 the SE tax: "Thus, for purposes of section 199A, deductions such as the deductible portion of the tax on self-employment income under section 164(f), the self-employed health insurance deduction under section 162(l), and the deduction for contributions to qualified retirement plans under section 404 are considered attributable to a trade or business to the extent that the individual's gross income from the trade or business is taken into account in calculating the allowable deduction, on a proportionate basis." The net is that the after-tax value of contributing to an SEP or solo 401(k) declines by at least a few percentage points; I'm still calculating scenarios. For example, with $100k of SE income, and a $10,000 SEP contribution, the 20% QBI deduction is calculated on $100,000 - $10,000 SEP - $7650 SE tax = $82,350 x 20% = a $16,470 deduction. Not $20,000.4 points

-

That's why I am still using Windows 7 (64bit pro) and wait several days to install updates. Too many times there have been updates where suddenly computers won't boot, or all the printers drivers seize up, or other untenable result.4 points

-

Lately, part of the normal Windows update process is a chance that your OS will no longer be in a bootable state upon completion (or half-completion) of the installation, with potential for data loss. Keeping your system updated is important, but it's hard to blame the average person for being leery of updates given Microsoft's recent track record.4 points

-

I will quote you all season.4 points

-

It is an either or situation. The deduction is the smaller of 20% of QBI or 20% of taxable income as adjusted (in the simplest! form - assuming under the phaseout range.) That's why I am not telling anyone they will get 20% of their business income as a deduction. Like everything else in tax law, IT DEPENDS!3 points

-

Hey DTA, You need to hire a tax professional to help you. Just by the nature of your question, you are in way over your head. And the fact that you are asking on a web board looking for free advice is even more concerning. What you get for free on the internet is worth exactly what you pay for it. In a few minutes, the moderator is going to read back to you the terms of this site, which you agreed to when signed up and tell you that this site does not give advice to non-professionals. We only work with professionals in the tax industry. Then she is going to lock this post. Get a tax advisor, someone who is reputable, and pay them to answer your questions. Tom Modesto, CA3 points

-

Gail subtracted the standard deduction because she assumed no other income. The QBI deduction is the lesser of 20% of the QBI or 20% of taxable income. Under Gail's assumption, taxable income is less than the QBI.3 points

-

The other way to look at this, though, is if they only have SE income, then the taxable income would be after the SEHI deduction, and the SEP (or whatever) deduction, and the 1/2 SE tax deduction AND the standard deduction. So in your example, if they had NO OTHER INCOME, the actual QBI they would wind up with assuming they are single would be $14,070 (100,000-10,000-7,650-12,000=70,350 x 20%). There are so many variables in this mess, and I am still learning how they all come together. By 2025 I should have it down pat.3 points

-

I figured out how the get the QBI for a specified service business to show up on the QBI Deduction - Service tab. On the Activities tab, you have to check both the qualified business box and the service business box. You still have to provide the income for a Schedule C business in the Income/Loss box on the Activities tab. If an S corporation's income needs adjustment from the K-1 reported QBI amount, you would adjust the amount that shows up in the Income/Loss box. I think all ATX needs to do is provide a way to aggregate activities if that is desired.3 points

-

SSTB restrictions kick in at the threshold levels. If they are below the threshold levels the restrictions do not apply. Below taken from IS FAQ regarding section 199A & SSTB's. 8. In 2018, I will report taxable income under $315,000 and file married filing jointly. Do I have to determine if I am in an SSTB in order to take the deduction? Is there any limitation on my deduction? A8. No, if your 2018 taxable income is below $315,000, if married filing jointly, or $157,500 for all other filing statuses, it doesn’t matter what type of business you are in. You will be able to deduct the lesser of: a) Twenty percent (20%) of your QBI, plus 20 percent of your qualified REIT dividends and qualified PTP income, or b) Twenty percent (20%) of your taxable income minus your net capital gains.3 points

-

Yes, I'm sure that's true. And both sides either far right and far left irritate me. I've got both in my family and friends and I'm ready to look for a big rock to get under.2 points

-

I just called Richmond. The verdict on Sch A (when not itemizing on the federal) is still out. She said you can e-file, BUT they are not processing any tax returns until legislation has been rendered on the outstanding issues.2 points

-

I dunno; they have reported correctly in the past on government intrusions so I would not discount it out of hand. Take everything with a small boulder of salt, and research from original sources oneself. There is plenty of propaganda out there, masquerading as 'news', on all sides.2 points

-

Unfortunately, Tax Reform seems to knock this deduction out because it is a miscellaneous deduction subject to 2% of AGI per IRS Publication 529, and all such deductions are disallowed on Schedule A. The IRS is planning to issue regulations on this matter, and they asked for comments from the public in Notice 2018-61. Part of that Notice is excerpted here: The section 642(h)(2) excess deduction may include expenses described in section 67(e). As previously discussed, prior to enactment of section 67(g), miscellaneous itemized deductions were allowed subject to the restrictions contained in 8 section 67(a). For the years in which section 67(g) is effective, miscellaneous itemized deductions are not permitted, and that appears to include the section 642(h)(2) excess deduction. The Treasury Department and the IRS are studying whether section 67(e) deductions, as well as other deductions that would not be subject to the limitations imposed by sections 67(a) and (g) in the hands of the trust or estate, should continue to be treated as miscellaneous itemized deductions when they are included as a section 642(h)(2) excess deduction. Taxpayers should note that section 67(e) provides that appropriate adjustments shall be made in the application of part I of subchapter J of chapter 1 of the Code to take into account the provisions of section 67. The Treasury Department and the IRS intend to issue regulations in this area and request comments regarding the effect of section 67(g) on the ability of the beneficiary to deduct amounts comprising the section 642(h)(2) excess deduction upon the termination of a trust or estate in light of sections 642(h) and 1.642(h)-2(a). In particular, the Treasury Department and the IRS request comments concerning whether the separate amounts comprising the section 642(h)(2) excess deduction, such as any amounts that are section 67(e) deductions, should be separately analyzed when applying section 67. (Emphasis underlined.)2 points

-

Oh and there was previous argument that a K-1 doesn't include any info on whether the income qualifies - WRONG! What do I do if the K1 doesn’t have any information in the new QBI codes? If the taxpayer gets a K-1 that does not have any info in the new K1 codes, but you believe it should be a qualifying trade or business, the taxpayer should request a corrected K-1 from the partnership, scorp, or fiduciary. If the QBI info is not recorded in the codes, the IRS will assume it is not a qualifying business, so the taxpayer will not be allowed to take the deduction from the pass-through entity.2 points

-

No, just amend whoever you want to be first on the return and add the other taxpayer. IRS knows how to handle this.2 points

-

Only if you exceed the income thresholds. Small time folks like me can still take the QBI, possibly. A lengthy read but seems to be the best analysis given to date.2 points

-

https://www.journalofaccountancy.com/news/2019/jan/sec-199a-qbi-deduction-201920483.html?utm_source=mnl:alerts&utm_medium=email&utm_campaign=22Jan2019&utm_content=button Qualified business income deduction regs. and other guidance issued By Sally P. Schreiber, J.D.; Paul Bonner; and Alistair M. Nevius, J.D. On Friday, the IRS released guidance on a large number of Sec. 199A issues, including the eagerly awaited final Sec. 199A regulations (in an as-yet-unnumbered Treasury decision). The IRS also issued new proposed regulations on how to treat previously suspended losses and how to determine the deduction for taxpayers that hold interests in regulated investment companies (RICs), charitable remainder trusts (CRTs), and split-interest trusts. The guidance also includes a notice that provides a safe-harbor rule for rental real estate businesses and a revenue procedure on calculating W-2 wages. Sec. 199A allows taxpayers to deduction up to 20% of qualified business income (QBI) from a domestic business operated as a sole proprietorship or through a partnership, S corporation, trust, or estate. The Sec. 199A deduction can be taken by individuals and by some estates and trusts. The deduction is not available for wage income or for business income earned through a C corporation. The deduction is generally available to taxpayers whose 2018 taxable incomes fall below $315,000 for joint returns and $157,500 for other taxpayers. The deduction is generally equal to the lesser of 20% of the taxpayer’s QBI plus 20% of the taxpayer’s qualified real estate investment trust (REIT) dividends and qualified publicly traded partnership (PTP) income, or 20% of taxable income minus net capital gains. Deductions for taxpayers above the $157,500/$315,000 thresholds may be limited; the application of those limits is described in the regulations. These amounts are inflation-adjusted. (For more on the deduction, see “Understanding the New Sec. 199A Business Income Deduction,” The Tax Adviser, April 2018). Final regulations The IRS noted that the final regulations had been modified somewhat from the proposed regulations issued last August (REG-107892-18) as a result of comments it received and testimony at a public hearing it held. The final regulations apply to tax years ending after their publication in the Federal Register (they have so far only been posted on the IRS website); however, taxpayers may rely on the proposed regulations for tax years ending in 2018. The final regulations focus on determining the amount of Sec. 199A deduction. They also cover determining when to treat two or more trusts as a single trust for purposes of Subchapter J (governing estates, trusts, beneficiaries, and decedents). The IRS says it received approximately 335 comments on the proposed regulations. The final regulations contain modifications based on some of those comments, and the IRS says it is continuing to study some comments it received that were beyond the scope of the proposed regulations. Net capital gain: First, the IRS noted that it had not defined “net capital gain” in the proposed regulations and that a number of commenters had requested a definition. The final regulations, however, reject one comment suggesting that net capital gain exclude qualified dividends. Instead, the regulations define net capital gain for purposes of Sec. 199A as net capital gain under Sec. 1222(11) (the excess of net long-term capital gain for the tax year over the net short-term capital loss for that year) plus qualified dividend income as defined in Sec. 1(h)(11)(B). Relevant passthrough entities: The proposed regulations define a relevant passthrough entity (RPE) as a partnership (other than a PTP) or an S corporation that is owned, directly or indirectly, by at least one individual, estate, or trust. A trust or estate is treated as an RPE to the extent it passes through QBI, W-2 wages, unadjusted basis immediately before acquisition (UBIA) of qualified property, qualified REIT dividends, or qualified PTP income. The final regulations expand this definition by providing that other passthrough entities, including common trust funds described in Temp. Regs. Sec. 1.6032-T and religious or apostolic organizations described in Sec. 501(d), are also treated as relevant passthrough entities if the entity files a Form 1065, U.S. Return of Partnership Income, and is owned, directly or indirectly, by at least one individual, estate, or trust. It declined to treat RICs as RPEs, however, because they are C corporations. Trade or business: After considering all relevant comments, the final regulations retain and slightly reword the proposed regulations’ definition of a trade or business. Specifically, for purposes of Sec. 199A, Regs. Sec. 1.199A-1(b)(14) defines a trade or business as a trade or business under Sec. 162 other than the trade or business of performing services as an employee. The IRS again rejected suggestions that the IRS use the Sec. 469 passive activity rules, explaining that whether a trade or business exists is a different determination than that applied to the passive loss rules. Under the rules, the rental or licensing of tangible or intangible property to a related trade or business is treated as a trade or business if the rental or licensing activity and the other trade or business are commonly controlled under Regs. Sec. 1.199A-4(b)(1)(i). This rule also allows taxpayers to aggregate their trades or businesses with the leasing or licensing of the associated rental or intangible property if all of the requirements of Regs. Sec. 1.199A-4 are met. One commenter suggested the rule apply to situations in which the rental or licensing is to a commonly controlled C corporation. Another commenter suggested that the rule in the proposed regulations could allow passive leasing and licensing-type activities to benefit from Sec. 199A even if the counterparty is not an individual or an RPE. The commenter recommended that the exception be limited to scenarios in which the related party is an individual or an RPE and that the term related party be defined with reference to existing attribution rules under Sec. 267, 707, or 414. The final regulations clarify these rules by adopting these recommendations and limiting this special rule to situations in which the related party is an individual or an RPE. Commenters also asked the IRS to provide safe harbors or factors for determining how to delineate separate trades or businesses conducted within one entity and when an entity’s combined activities should constitute a single trade or business, but the IRS declined to provide this guidance. The IRS warns that taxpayers should report items consistently. For example, the IRS says that taxpayers who treat a rental activity as a trade or business for purposes of Sec. 199A should also comply with the Form 1099 information-reporting requirements under Sec. 6041. The final regulations also provide computational rules. The final regulations clarify the proposed regulations by providing that for taxpayers with taxable income within the phase-in range, QBI from a specified service trade or business (SSTB) must be reduced by the applicable percentage before the application of the netting and carryover rules described in Regs. Sec. 1.199A1(d)(2)(iii)(A). The final regulations also clarify that the SSTB limitations also apply to qualified income received by an individual from a PTP. Disregarded entities: The proposed regulations did not address the treatment of disregarded entities. The final regulations provide that an entity with a single owner that is treated as disregarded as an entity separate from its owner under Regs. Sec. 301.7701-3 is disregarded for Sec. 199A purposes. Accordingly, trades or businesses conducted by a disregarded entity are treated as conducted directly by the owner of the entity. Share of UBIA property: The final regulations modify the proposed regulations with regard to the allocation to partners of the UBIA of qualified property. In the proposed regulations, in the case of a partnership with qualified property that does not produce tax depreciation during the year, each partner’s share of the UBIA of qualified property would be based on how gain would be allocated to the partners pursuant to Secs. 704(b) and 704(c) if the qualified property were sold in a hypothetical transaction for cash equal to the fair market value of the qualified property. The IRS adopted a commenter’s suggestion that for partnerships, only Sec. 704(b), not Sec. 704(c), should apply to determine each partner’s share of the UBIA of qualified property. Thus, the final regulations state that each partner’s share of the UBIA of qualified property is determined in accordance with how depreciation would be allocated for Sec. 704(b) book purposes under Regs. Sec. 1.704-1(b)(2)(iv)(g) on the last day of the tax year. Under the final regulations, for an S corporation’s qualified property, each shareholder’s share of UBIA of qualified property is a share of the unadjusted basis proportionate to the ratio of shares in the S corporation held by the shareholder on the last day of the tax year over the total issued and outstanding shares of the S corporation. Basis for contributed property: Another change in response to comments was for a basis rule for property contributed to a partnership in a Sec. 721 transaction or to an S corporation in a Sec. 351 transaction that the property should retain its basis. Therefore, Regs. Sec. 1.199A-2(c)(3)(iv) provides that, solely for Sec. 199A purposes, if qualified property is acquired in a transaction described in Sec. 168(i)(7)(B), the transferee’s UBIA in the qualified property is the same as the transferor’s UBIA in the property, decreased by the amount of money received by the transferee in the transaction or increased by the amount of money paid by the transferee to acquire the property in the transaction. Similarly, the final rules clarify how to determine the UBIA of replacement property under Sec. 1031 or 1033 in response to comments. They also explain how Sec. 743(b) basis adjustments for partnerships should be treated for UBIA but also request further comments on Sec. 743(b) adjustments. Aggregating trades or businesses: The IRS declined to adopt most of the comments it received on aggregating trades or businesses, but it did permit an RPE to aggregate trades or businesses it operates directly or through lower-tier RPEs. The resulting aggregation must be reported by the RPE and by all owners of the RPE. An individual or upper-tier RPE may not separate the aggregated trade or business of a lower-tier RPE but instead must maintain the lower-tier RPE’s aggregation. An individual or upper-tier RPE may aggregate additional trades or businesses with the lower-tier RPE’s aggregation if the rules of Regs. Sec. 1.199A-4 are otherwise satisfied. The IRS also chose to permit taxpayers who have not reported businesses as aggregated on a tax return to choose later to aggregate businesses on a future tax return. However, taxpayers cannot aggregate businesses on an amended return because that would permit taxpayers the benefit of hindsight. Because many taxpayers were not aware of the aggregation rule, though, for 2018, they may report an aggregation on an amended return. Performing services as an employee: The final regulations, like the proposed regulations, include a presumption that an individual who was previously treated as an employee and is subsequently treated as an independent contractor while performing substantially the same services for the same employer or a related person will be presumed to still be in the trade or business of performing services as an employee for purposes of Sec. 199A. However, in response to comments, the final regulations were modified to include a three-year lookback rule for this presumption. The individual can rebut the presumption by showing records that corroborate the individual’s status as a nonemployee. Specified service trades or businesses: A large part of the preamble to the final regulations was devoted to comments received on SSTBs. Apart from a few clarifications in the definitions, the final regulations did not adopt these comments. Proposed regulations At the same time as it released the final regulations, the IRS also released new proposed regulations (REG-134652-18) treating certain issues not addressed in the proposed regulations issued in August 2018, specifically: (1) the treatment under Sec. 199A of previously suspended losses, (2) “Sec. 199A dividends” paid by a RIC, and (3) the treatment of amounts received from split-interest trusts and CRTs. Previously suspended losses: The proposed regulations amend Prop. Regs. Sec. 1.199A-3(b)(1)(iv) to provide that previously disallowed, suspended, limited, or carried over losses (including under Secs. 465, 469, 704(b), and 1366(b) and only for disallowance, etc., years ending after Jan. 1, 2018) are taken into account for QBI purposes on a first-in, first-out basis and are treated as from a separate trade or business. To the extent that losses relate to a PTP, they must be treated as losses from a separate PTP. In addition, the attributes of these losses with respect to Sec. 199A are determined according to the year incurred. Sec. 199A dividends by RICs: In redesignated Prop. Regs. Sec. 1.199A-3(d), the IRS proposed that RICs under Sec. 852(b) may pay Sec. 199A dividends, defined as any dividend that a RIC pays to its shareholders and reports as such in written statements to its shareholders. The rules under which a RIC would compute and report Sec. 199A dividends are based on the rules for capital gain dividends in Sec. 852(b)(3) and exempt interest dividends in Sec. 852(b)(5). The amount of a RIC’s Sec. 199A dividends for a tax year would be limited to the excess of the RIC’s qualified REIT dividends for the tax year over allocable expenses. Split-interest trusts and CRTs: These proposed regulations redesignate Prop. Regs. Sec. 1.199A-6(d)(3)(iii) to state that a trust with substantially separate and independent shares and multiple beneficiaries is treated as a single trust for determining the application of the threshold amount under Sec. 199A(e)(2). In addition, new Prop. Regs. Sec. 1.199A-6(d)(v) provides that in the case of a CRT, any taxable recipient of a unitrust or annuity amount from a trust must determine and apply the recipient’s own Sec. 199A threshold amount, taking into account any annuity or unitrust amounts received from the trust. These recipients may take into account any included QBI, qualified REIT dividends, or qualified PTP income so distributed for purposes of determining their own QBI deduction. PTPs: The IRS reserved for further study and comment the treatment of qualified PTP income in qualified Sec. 199A dividends distributed by RICs, noting several technical and administrative problems of their proper characterization with respect to recipients. These proposed regulations are effective when adopted as final, but the IRS stated that taxpayers may rely on them in the interim. Calculating W-2 wages Rev. Proc. 2019-11 provides guidance on how to calculate W-2 wages for purposes of Sec. 199A. Sec. 199A(b)(2) uses W-2 wages to limit the amount of a taxpayer’s Sec. 199A deduction in certain situations. Sec. 199A(b)(4) defines W-2 wages to mean amounts described in Secs. 6051(a)(3) (generally remuneration paid for services paid by an employee to an employer) and 6051(a)(8) (elective deferrals and deferred compensation) paid by a person claiming the deduction with respect to employment of employees by that person during the year. W-2 wages does not include any amount that is not properly allocable to QBI under Sec. 199A(c)(1) or any amount not properly included in a return filed with the Social Security Administration (SSA) on or before the 60th day after the due date for the return. The revenue procedure provides three methods for calculating W-2 wages: the unmodified box method, the modified box 1 method, and the tracking changes method. The IRS cautions that using one of these methods does not necessarily calculate the W-2 wages that are properly allocable to QBI and eligible for use in computing the Sec. 199A limitations. After using the revenue procedure to calculate W-2 wages, the taxpayer must then determine the extent to which they are properly allocable to QBI. The IRS also cautions that the revenue procedure cannot be used for determining if amounts are wages for employment tax purposes. The unmodified box method described in the revenue procedure involves taking, without modification, the lesser of (1) the total entries in box 1 (wages, tips, and other compensation) of all Forms W-2, Wage and Tax Statement, filed by the taxpayer with the SSA or (2) the total entries in box 5 (Medicare wages and tips) of all Forms W-2 filed by the taxpayer with the SSA. The modified box 1 method involves making modifications to the total entries in box 1 of all Forms W-2 filed by the taxpayer with the SSA by subtracting amounts that are not wages for federal income tax withholding purposes (such as supplemental unemployment compensation benefits) and adding the total amounts of various elective deferrals that are reported in box 12. Under the tracking wages method, the taxpayer tracks total wages subject to federal income tax withholding and elective deferrals reported in box 12. Rental real estate activities Many of the comments the IRS received regarding the proposed regulations dealt with the question of when rental activity qualifies as a trade or business. Therefore, in Notice 2019-07, the IRS has issued a proposed revenue procedure that would provide a safe harbor for taxpayers. Under the proposed safe harbor, a “rental real estate enterprise” would be treated as a trade or business for purposes of Sec. 199A if at least 250 hours of services are performed each tax year with respect to the enterprise. The IRS says this includes services performed by owners, employees, and independent contractors and time spent on maintenance, repairs, rent collection, payment of expenses, provision of services to tenants, and efforts to rent the property. However, hours spent in the owner’s capacity as an investor, such as arranging financing, procuring property, reviewing financial statements or reports on operations, and traveling to and from the real estate will not be considered hours of service with respect to the enterprise. A rental real estate enterprise is defined, for purposes of the safe harbor, as an interest in real property held for the production of rents. A rental real estate enterprise may consist of multiple properties. The interest must be held directly or through a disregarded entity. Taxpayers either must treat each property held for the production of rents as a separate enterprise or must treat all similar properties held for the production of rents as a single enterprise. Commercial and residential real estate cannot be combined in the same enterprise. The proposed safe harbor would require that separate books and records and separate bank accounts be maintained for the rental real estate enterprise. Property leased under a triple net lease or used by the taxpayer (including an owner or beneficiary of a relevant passthrough entity) as a residence for any part of the year under Sec. 280A would not be eligible under the proposed safe harbor. AICPA webcast On Jan. 23, from 1 to 3 p.m. ET, the AICPA will present a comprehensive overview of the final IRS guidance. The webcast will review the issues that the final regulations modify and explain, including expansion of the aggregation rules, clarification around rental real estate activities, examples, and more. Don’t miss this opportunity to understand the final regulations before helping your clients with this new area of the tax law. Click here to learn more. — Sally Schreiber, J.D, ([email protected]) and Paul Bonner ([email protected]) are JofA senior editors. Alistair Nevius, J.D., ([email protected]) is the JofA’s editor-in-chief, tax.2 points

-

@Mitzi rogers please see the notation in red that is part of this forum's registration rules that you agreed too:2 points

-

You will want to contact Turbo Tax. We are professional tax preparers using professional preparation software and cannot help you with whether TT reported a refund for your 2016 returns.2 points

-

The proposed regs have knocked out all of my rental clients except one whose qualification is questionable since he is always juggling multiple business issues and the probability of him maintaining a contemporaneous activity log is pretty low. For those of you with clients who might qualify, here is a step by step in depth analysis : https://www.forbes.com/sites/anthonynitti/2019/01/19/irs-publishes-final-guidance-on-the-20-pass-through-deduction-putting-it-all-together/?ss=taxes#55344e92d9f01 point

-

If you spend some time setting up the print sets it makes printing quicker.1 point

-

I hate to ask such a dumb question to this learned group, but I don't want to spend an hour and a half on ATX' jiffy-quick support line, so can someone please point me to the "Comparison Form" referred to inside the ATX program. When you open a client's return and go to the bottom of the page where "Main Iinformation Worksheet" is located and punch it, a form comes up with a square blue box that says "Please review the comparison form to ensure that you have reported all income and deduction amounts for this taxpayer." Where is that form? Since a bomb was dropped on our old 1040 and idiotically exploded into six different "postcards" of incomes, credit, taxes, etc., I was hoping that there would be a non-filing summary sheet somewhere that would let you see if all the different items have been entered without having to go through all the postcards (sort of an unofficial 1040 to look at and save time). Is that what this blue box refers to? And if so, where is it? Any advice would be appreciated.1 point

-

I've been using this form for several years and include it with the electronic return (or printed for those few) so folks can more readily see how changes in their income and deductions from last year resulted in the current year's higher or lower taxes. I wish there was a comparable form for the state but those fluctuations aren't as obvious any way. It tends to forestall some questions from clients.1 point

-

I cannot imagine anyone considering IRS regs as a mess. By the way Gail I called the local Commissioner's office to see if they might provide any info on the opening of state efile. Their usual answer was DUH !1 point

-

Online list shows release on Jan. 25. You could also just compare with last year's return the hard way. It will be interesting to see the new comparison form and how it shows the placements of income and deductions between somewhat different return formats.1 point

-

I kind of think like you said, mine was part of a test batch. Usually I don't transmit early but new to Drake this year I wanted to check out the process. I am amazed at the speed of Drake! Thank you for the tips!. Now if I could figure out the mayor's thing, and how to quickly select what I want to print.1 point

-

Terry, The TCJA BLUE BOOK and the proposed reg specifically stated that sec 162 will be used in defining a trade or business. That was clarified by the final reg which specifically states on page 14 that section 469 will not be used. I would ask your CPE instructor where he came up with his 469 statement.1 point

-

Judy I believe a partnership is a disregarded entity described in 301.7701-3. § 301.7701-3 Classification of certain business entities. (a)In general. A business entity that is not classified as a corporation under § 301.7701-2(b)(1), (3), (4), (5), (6), (7), or (8) (an eligible entity) can elect its classification for federal taxpurposes as provided in this section. An eligible entity with at least two members can elect to be classified as either an association (and thus a corporation under § 301.7701-2(b)(2)) or apartnership, and an eligible entity with a single owner can elect to be classified as an association or to be disregarded as an entity separate from its owner.1 point

-

I believe that the IRS does process a limited number of returns ahead of the official opening. Perhaps your client's returns were in one of those batches. If you are very concerned, Drake support should be able to tell you for sure.1 point

-

I don't believe that the comparison form has been released yet. At least not by yesterday when I rolled over a return.1 point

-

It is showing as IRS accepted, and the state CA accepted. Seems odd if they are not opening up till next Monday.1 point

-

You can sort the Client Manager list by clicking on any column heading, so for example, clicking on the Fed Ack status column will put them in order by grouping the various statuses. In client manager, I have additional columns to track the ack status and date of each state. The state of residence will show as state 1, other states as state 2, and so forth. With all of that set up, once a client's Fed and state acks are all back as "accepted" with a capital 'A' (little 'a' is used for extensions), then I will change the client status to "complete", and I have the client manager set to "hide completed returns" so that the only returns that show are those that are in process. Right clicking anywhere in the client manager will bring up the options for what to display and allow customizing the columns.1 point

-

Is it possible this return was accepted by the Drake servers and not the IRS or CA? From the client manager, right click on the client's name and select "Open Efile Data Base For Selected Client. This will give you the transmission detail. Maybe you just got one thru. To answer your second question, in the client manager, the status will be displayed. It will show accepted, rejected, pending; etc. Also, look at the left side of the screen under alerts and notifications, if you have a notice you have acks to process, click that and it will give you the status as well. Trust me when I say, once you get used to Drake, you won't regret it. Yes, a small learning curve. In the early years of ATX/Sabre Pro, I always fought with how to know the status of a return. Last year I used ATX was 2007 so a lot may have changed.1 point

-

I saw a different article about this subject several weeks ago.1 point

-

That's for sure. Can't believe anything those guys say. Although by the title you never know these days.1 point

-

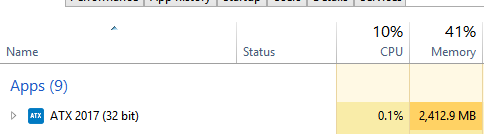

...just take a look at this RAM usage!

1 point

1 point -

They won't hire me. My mindset is not like theirs. I have attempted to get hired, to help design the software, and teach "Customer Service" employees how to be "Customer Service" employees.1 point

-

Upper level employees should have reserves, but low level employees don’t make a ton of money, and if in DC, it’s an expensive place to live. It also depends on the length of time on the job, size of family, etc. if you think the people keying paper returns make enough to save 6 months living expenses, you aren’t thinking correctly. I had the same kind of experience after college as Katherine did, although she didn’t mention any stints of homelessness as I had. And looking for the free food the Hare Krishnas served in the park. While I was working, too. But I have a bit more compassion for others in hard circumstances.1 point

-

Bart: As you well know, a sense of humor and not taking ourselves too seriously can get us through a lot of tough situations. Although I have to say a client took it real personal one time when I told him I'm not a caring person, but I am feeling person. (We were talking about a tax problem he had which was of his own making.) After staring in awkward silence, he replied he didn't understand. So I explained, "I really don't care, but sometimes I feel bad about not caring." You know, that guy left and never did come back.1 point

-

Data collected from banks, credit cards and other sources without authorization. 100 times more data collected in 2017 than in 2007. Privacy - GONE. Audits to be made through data analytics. One can imagine all kinds of scenarios on the horizon. https://www.wnd.com/2019/01/big-data-meets-big-govt-new-irs-spy-software/0 points